Women and China’s property market: Married to the mortgage; Are high house prices hurting women more than men?

July 17, 2013 Leave a comment

Women and the property market: Married to the mortgage; Are high house prices hurting women more than men?

Jul 13th 2013 | BEIJING |From the print edition

CHINA’s communists attacked many bourgeois institutions after taking power in 1949. But marriage was not one of them. On the contrary, they enacted a marriage law in 1950, four years before they introduced a constitution. The pressure to marry remains heavy in today’s China, where almost 80% of adults have tied the knot at some point, compared with only 68% in America. But today, in contrast to the 1950s, marriage is bound up with another bourgeois institution: property. In China mortgages often precede marriages. According to popular belief, if a man and his family cannot buy property he will struggle to find a bride. In choosing a husband, three-quarters of women consider his ability to provide a home, according to a recent survey of young people in China’s coastal cities by Horizon China, a Beijing-based market-research firm. Even if a woman herself dismisses this criterion, her family and friends, not to mention the country’s estate agents, will not let her forget it.

“Naked marriages”, as property-less ones are known, are endorsed by increasing numbers of young people. But as they get older, their attitudes may regress faster than society’s progress. One 28-year-old Beijing woman married her husband after falling in love with him at college. But “if you introduced a man to me now, and he couldn’t afford a home, I wouldn’t marry him,” she says. “I need to be more realistic. I’m not a 20-year-old girl.”

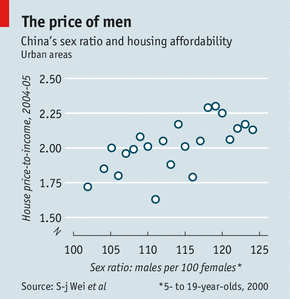

Some economists argue that competition for brides in China’s marriage “market” helps explain the punishingly high prices in its property market. Houses are least affordable in those parts of China where men most outnumber women, argue Shang-jin Wei of Columbia University, Xiaobo Zhang of the International Food Policy Research Institute and Yin Liu of Tsinghua University (see chart).

Men (and their families) splash out on property to improve their position in the marriage queue. But that merely forces other men to spend more in response. Unmarried men are locked in a Darwinian race, the economists argue. Overpriced homes are like the extravagant plumage of a peacock, an eye-catching encumbrance that only the most resourceful males can put on display.

The burden of home-buying thus falls heavily on unmarried men. But it is no longer confined to them. Women and their families now contribute to their partner’s home purchases in 70% of cases, according to Horizon China’s research. They help out both because they must—couples have to pool their resources to afford coastal China’s pricey homes—and because they can. Young women are earning more and receiving more help from their parents, for whom they are often now the only child.

The machismo of mortgages

Although most women now contribute to the purchase of the home, only 30% of married women add their name to the title certificate, according to Horizon China’s research. Leta Hong Fincher, a sociologist at Tsinghua University, worries that “many Chinese women are shut out of what may be the biggest accumulation of residential wealth in history.”

More women are trying to add their name to this wealth. Of those married after 2006, 37% have succeeded. Their efforts gained new urgency in 2011 when the Supreme Court clarified the divorce rules. Each party, it said, would keep the property registered in their name, after compensating their ex for any contributions to the mortgage.

But joint registration of property faces bureaucratic and social obstacles. One woman interviewed by Ms Hong Fincher contributed heavily to the down-payment on a home and insisted on registering it in both names. But her boyfriend’s mother begged her to drop her demand, pointing out that the bride-to-be outearned him and was more likely to leave him than vice versa. Joint-ownership would be a further blow to his pride.

In principle, the law entitles a divorced wife to compensation for her mortgage contributions, even if the family home was not registered in her name. But women do not always document their home payments. And even if they pay nothing towards a mortgage, they may still pay a lot towards other household expenses, Ms Hong Fincher points out. In many cases, the man can afford the mortgage only because the woman takes care of the fittings, furnishings and many other expenses.

“Home ownership defines masculinity,” Ms Hong Fincher says. Often a couple’s finances are arranged so that the husband can take all the pride of owning the home, even if, in reality, his wife is jointly supporting the household. A dutiful wife may feel obliged to bolster his pretence. In China, macho posturing is another bubble that has yet to burst.