Financial-technology firms: Tech start-ups promise to transform finance, if regulators will let them

August 2, 2013 Leave a comment

Financial-technology firms: Tech start-ups promise to transform finance, if regulators will let them

Aug 3rd 2013 |From the print edition

TWO millennia after the Temple was cleansed of money-changers, the Archbishop of Canterbury, Justin Welby, plans to open his churches to moneylenders. This is no capitulation in the struggle between God and Mammon. It is an effort to “compete out of existence” payday lenders that offer expensive loans by supporting not-for-profit credit unions.

The archbishop is right that more competition is needed, but old-fashioned credit unions are unlikely to be able to beat the slick systems and snappy service of online providers, like Wonga. A more effective way of pushing down rates would be lighter regulation to allow more lenders to flourish.Digital communications have given birth to a new generation of finance companies (see article). Money-transfer agents such as Xoom have drastically cut the time and costs for migrant workers to send money home. Peer-to-peer lenders are matching savers and borrowers, slashing fees and delivering a better deal to both. New foreign-exchange firms are giving travellers access to the prices quoted on wholesale currency markets. Card companies such as Square and iZettle let anyone from yoga teachers to plumbers accept payments by credit card. Firms such as M-Pesa have given millions of people in developing countries access to mobile money.

Heavy regulation of financial companies means many firms stick to small niches to skirt the boundaries of banking regulations. Peer-to-peer lenders do not offer savers the security of deposit insurance or the convenience of guaranteed instant access to their cash. This limits their appeal. Other firms that take deposits such as Holvi, a Finnish start-up that offers group accounts, are not allowed to lend. Those that do lend, such as Wonga, cannot take deposits.

Creating a financial-tech company is arduous. Whereas it takes less than a day to register a company in Britain, it takes months or years and can cost millions to get authorised as a bank. The number of new banks started over the past decade can almost be counted on one hand. Even those that have started, such as Metro Bank or Aldermore, are penalised by regulation: rules on capital favour large and complex firms. In America the Dodd-Frank Act is an imposing barrier to all but the biggest firms. And regulation is closing in on some existing firms. M-Pesa has struggled to grow much beyond Kenya, partly because authorities stand in its way. The market for remittances has been a hothouse for start-ups in Britain, partly because it was lightly regulated. Yet almost half the country’s money-transfer firms may be shut as banks close their accounts to comply with money-laundering rules.

Banks need to be more heavily regulated than other firms because of their central role in the economy. However, governments could regulate more smartly, raising capital requirements for big and systemically important banks while easing the burden on smaller ones. Regulators should be even more relaxed about many of the new entrants to the market, most of which simply provide quicker and simpler ways of shifting money around. Most of these start-ups avoid the alchemy of banking—the transformation of short-term deposits into long-term loans—so pose little systemic risk.

The idea of lighter-touch regulation will seem to many an anathema after the financial crisis. It would certainly lead to more failures by small banks and start-ups. This would also impose some costs on society and deposit-guarantee schemes. Yet these costs would be outweighed by the enormous benefits to consumers and businesses of a far more competitive financial system.

Financial-technology firms

Revenge of the nerds

An explosion of start-ups is changing finance for the better

Aug 3rd 2013 |From the print edition

THINK of banking today and the image is of grey-suited men in towering skyscrapers. Its future, however, is being shaped in converted warehouses and funky offices in San Francisco, New York and London, where bright young things in jeans and T-shirts huddle around laptops, sipping lattes or munching on free food.

A wave of financial-technology (or “fin-tech”) firms, many of them just a few years old, are changing the ways in which people borrow and save, pay for things, buy foreign exchange and send money. In doing so they are finding and mining rich seams of profit, challenging the business models of existing institutions and inflating a bubble of excitement among investors that technology and the internet are about to change banking for good.

Much of this may sound like hype, particularly to those whose memories take in the unmet promises of internet banks at the height of the dotcom bubble, or that go back earlier still to the statements of Bill Gates, the co-founder of Microsoft, that banks were dinosaurs. Yet the growth rates of some of these start-ups seem to warrant the excitement.

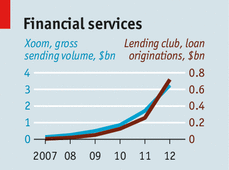

Take Xoom, a San Francisco-based firm that is little more than a decade old. It specialises in sending small amounts of money across borders. By collecting the money online, and using technology to minimise fraud, it is able to undercut the fees charged by traditional money-senders such as Western Union that have huge networks of agents to collect and distribute cash. Its stock has more than doubled since its IPO earlier this year, valuing the company at more than $1 billion, a heady figure for a firm that reported revenues for 2012 of just $80m and a net loss for the year of $5m. In an echo of the valuation methods used before the bursting of the dotcom bubble in 2001, its shares are priced not in relation to its profits or even its revenue but to its extraordinary growth.

In Britain similar buzz surrounds Wonga, an even younger firm that specialises in making short-term loans at eye-popping interest rates. The firm is controversial: it occupies the same market as payday lenders. The Archbishop of Canterbury, no less, has said he wants to use church credit unions to compete it out of existence. But Wonga is growing fast thanks to slick technology and clever algorithms that analyse masses of data, including how much time customers spend on its website. This allows it to reach credit decisions in seconds. The time taken between a customer applying for a loan and receiving the money in their bank can be mere minutes.

Some in the industry think Wonga will be valued at more than £1 billion ($1.5 billion) when it comes onto public markets. Its profit margins make that seem plausible. In 2011, the most recent year for which its financial information is publicly available, the firm produced a pre-tax profit of £62m on revenues of £185m.

The excitement around these companies and others has venture-capital (VC) firms tripping over one another to find the next Wonga or Xoom. “I get two to three calls a week from VCs,” says Michael Kent, the CEO of Azimo, an online money-sending firm based in London.

Several factors have converged over the past few years to produce the upsurge in fin-tech firms. First was the financial crisis, which damaged trust in banks. It also precipitated several years of record-low interest rates, which pushed savers to look for better returns where they can. That has benefited peer-to-peer lenders such as Lending Club, an American firm that provides a platform on which investors can lend to borrowers and that recently passed the $2 billion mark for loans originated.

Shape of fin to come

The rise of cloud computing, a term for software and services delivered over the internet, has also slashed barriers to entry for technology firms. This is true across many areas of business but it is an especially potent force in financial services, which is a digitised industry in which most money exists as bits and bytes in computers rather than as notes and coins.

Globalisation also helps. Sonali de Rycker, a partner at Accel, a VC firm, and a director of Wonga, points out that the company initially got started by outsourcing much of its programming to developers in Kiev, the Ukrainian capital.

The spread of smartphones has also boosted tech start-ups by enabling the emergence of new ways of making or receiving payment. Firms such as Square in America or iZettle in Europe produce cheap credit-card readers that plug into smartphones and allow merchants to accept card payments. Their costs are low partly because customers already have sophisticated computers in their pockets.

The emergence of “big data”, a term used rather loosely to describe computer software that can analyse masses of information for patterns or correlations that people would not otherwise spot, is another factor. Number-crunching has helped firms such as Wonga and Zestcash, an American start-up, transform the way credit decisions are made.

Yet for all their promise, fin-tech firms still face formidable barriers. Chief among these is winning the trust of their customers. It is not a huge leap of faith to order a book online; it is a larger one to entrust your savings or the management of your financial life to a new company that seems to exist only on your computer screen or smartphone. Samir Desai, the chief executive and co-founder of Funding Circle, a British peer-to-peer lender that specialises in financing small businesses, says his biggest challenge is raising awareness among borrowers. “Less than 1% of businesses have heard of peer-to-peer lenders, or even know that there are alternatives to banks,” he says. As expensive as banks’ branch networks are, they provide advertising that money cannot easily buy.

Another challenge comes from the limits of their business models. Peer-to-peer lenders such as Zopa (with which your correspondent has deposited £50 in the name of research) are not able to offer their savers the security of insured deposits or a guarantee that they can withdraw their money when they want it. This makes them much less risky to regulators since they cannot suffer from bank runs, but less useful to customers who want long-term mortgages as well as instant access to their cash. Fin-tech firms will take lots of business from the banks in coming years. Replacing them is another matter.