Murky Data Muddy Debate on Chinese Consumers’ Strength

August 5, 2013 Leave a comment

August 4, 2013, 2:56 p.m. ET

Murky Data Muddy Debate on Chinese Consumers’ Strength

Issue Is Key to Determining Need for Policy Reform

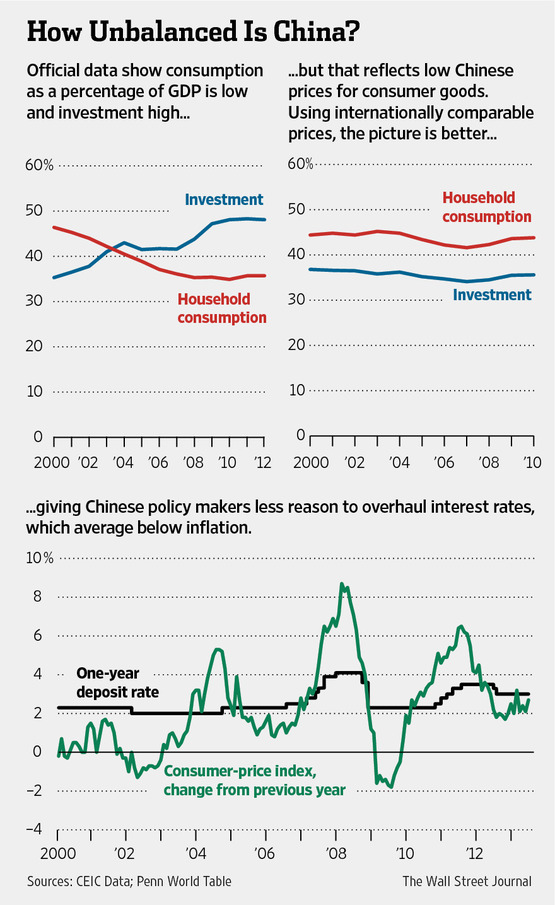

As China’s growth slows toward a 20-year low, economists are calling for consumers to shoulder more of the burden of supporting the world’s No. 2 economy. But the country’s leaders are increasingly saying Chinese consumers aren’t shirking their responsibility—they’re just undercounted. “The official data severely understates household consumption,” argued People’s Bank of China Deputy Governor Yi Gang, speaking at a meeting of top government and private economists from China and the U.S. in April. Mr. Yi also played down the role of China’s low interest rates—long seen as depressing consumption—in contributing to the imbalances, according to those present at the meeting.Low household consumption—in 2012 it accounted for 35.7% of China’s gross domestic product, compared with close to 70% in the U.S.—is widely seen as a key barrier to sustainable growth. With consumption’s share of GDP falling, according to the official data, China is driven to rely on investment, often in redundant infrastructure or ill-conceived factory projects, as a way to support the economy.

Mr. Yi’s view is that the real situation isn’t nearly so bleak. He cites numbers from the University of Pennsylvania showing that, measured in internationally comparable prices, China’s consumption is higher and more stable than the official data suggest; that is because compared with other countries, China’s consumer goods are cheap. The University of Pennsylvania numbers show the share of household consumption in China’s GDP was 43.8% in 2010, the latest year encompassed by their study.

If Mr. Yi is right, a resilient China should continue to be a global growth driver, with stronger consumer demand a boon for a variety of enterprises—from Apple selling iPhones to China’s middle class, to copper miners in Chile supplying raw materials for China’s expanding electrical grid.

If he’s wrong, a complacent government holding back from needed reforms risks a sharper slowdown, with global repercussions.

The central bank didn’t respond to requests for comment.

Mr. Yi isn’t the only Chinese economist making the case that China’s consumption is understated. In a recent paper, Li Daokui, a former member of the central bank’s Monetary Policy Committee, argued that household consumption as a share of China’s GDP was 38.5% in 2011, compared with 35.7% in the official data.

Crucially, Mr. Li sees a turning point in 2007, with household consumption steadily increasing its share since then. With the shift coinciding with tighter labor markets that raised wages and household income, Mr. Li argues that the economy is righting itself without the need for major jolts in policy.

“Our research shows that we should have a basic confidence in the current structural adjustment of China’s economy,” Mr. Li and his co-author wrote in the paper, adding that “government policy shouldn’t be overly hasty. Don’t spoil things by excessive zeal.”

The root of the disagreement between China’s statistics bureau and its critics: an official approach to adding up income and consumption that many independent economists regard as flawed. The government’s National Bureau of Statistics calculates consumption through a survey covering thousands of households across the country. But critics say a distorted sample and difficulty measuring certain types of spending skew the results downward.

One of the key flaws identified by Mr. Yi and other economists is difficulty measuring spending by China’s rich—who are likely underrepresented in the survey and unwilling to report all the details of their lavish lifestyles.

The survey also fails to capture some household consumption paid for by firms. For China’s massive state sector—which continues to employ millions of workers—firms often pick up employees’ tabs on myriad goods and services. “I have never bought rice or flour myself,” said Zhang Zhipeng, a worker with Yangquan Coal Industry Group, a government-owned firm in Shanxi province. “It’s one of the benefits of [working for] state-owned enterprises, you know.”

The National Bureau of Statistics didn’t respond to requests for comment.

China’s central bank is seen as taking the lead on reforms to get the economy back on an even keel. Near the top of the list of changes economists say is required: raising low interest rates. For the past decade, interest rates for bank savers have averaged below the rate of inflation, acting as a tax on household income.

Critics say low interest rates have crimped income for households by reducing returns on savings, denting consumption growth. The International Monetary Fund estimates that low interest rates transfer about 4% of GDP a year out of the pockets of household savers and into the coffers of state-owned firms that borrow at preferential rates. But if the share of consumption in GDP is understated, as Mr. Yi argues, the case for reform is weakened.

“I don’t agree with Yi Gang,” said Zhang Ming, a senior researcher at the Chinese Academy of Social Sciences, a government think tank, who was in the audience at the April event.

“Interest-rate regulation is the major financial repression tool in China, and the benchmark deposit rate is a key factor in the slow income growth and consumption of household sector,” he added.

That is a view widely held by economists in and outside China. Just not, it appears, by the central bank.