In Deal Hunt, Big-Game Buffett Settles for Small Prey; Berkshire Hathaway Boss Trains His ‘Elephant Gun’ on Junior-Sized Targets With Larger Ones Scarce

August 9, 2013 Leave a comment

Updated August 8, 2013, 4:38 p.m. ET

In Deal Hunt, Big-Game Buffett Settles for Small Prey

Berkshire Hathaway Boss Trains His ‘Elephant Gun’ on Junior-Sized Targets With Larger Ones Scarce

ANUPREETA DAS

Warren Buffett hasn’t fired his “elephant gun” much recently, but he has put his managers on the hunt for smaller prey. Berkshire Hathaway Inc.’s BRKB +0.72% subsidiary operations collectively spent about $2.3 billion on 26 acquisitions last year, which the company says is a record amount. They have continued that streak this year, acquiring more than a dozen companies in the first half of 2013. Berkshire hasn’t disclosed the amount spent by its subsidiaries on acquisitions this year. With bigger, multibillion-dollar deals few and far between of late, Mr. Buffett increasingly favors such “bolt-on” acquisitions because they increase Berkshire’s earnings and enable it to use its cash pile, which stood at $36 billion at the end of June. Net cash flow from operations rose nearly 36% for the first six months of 2013 from a year earlier, putting greater pressure on Berkshire to use its cash rather than hoard it. In a telephone interview, the Omaha, Neb.-based billionaire investor said he expected these types of deals to be frequent and numerous. “I like the managers finding opportunities,” Mr. Buffett said.Mr. Buffett, who turns 83 later this month, is famous for allowing the managers of Berkshire’s units to run their businesses without interference, but he is more hands-on when it comes to the CEOs’ deal-making. Some Berkshire chiefs send him monthly updates on potential targets.

These deals differ from “elephants,” which Mr. Buffett identifies as megadeals struck for Berkshire by him and his partner, Berkshire Vice Chairman Charlie Munger, often marking the gigantic conglomerate’s entry into a new business. In 2011, he wrote that his “elephant gun” is loaded and his “trigger finger is itchy.”

Despite the current paucity of companies that meet Mr. Buffett’s criteria of size, industry, earnings and price, he hasn’t called off the hunt. “A big deal still is what causes my heart to beat faster,” said Mr. Buffett in the recent interview. Berkshire teamed up with an investment firm in June to buy ketchup-maker H.J. Heinz Co. for $23.6 billion, putting up roughly half the amount.

After all, multibillion-dollar deals are what helped transform Berkshire from a textile manufacturer in the 1960s to a holding company with $288 billion in market value, with interests spanning from running shoes to a railroad.

Berkshire subsidiaries don’t always disclose how much they spend on individual deals, but the bigger transactions tend to be at least $1 billion, Berkshire executives said. In a notable exception, Berkshire unit MidAmerican Energy Holdings Co. said in May it would buy Nevada utility NV Energy Inc. for $5.6 billion.

Because of Berkshire’s diverse holdings and its financial heft, Mr. Buffett and his managers frequently get approached by companies wanting to sell. The ability to pick and choose deals is a relative luxury in the mergers-and-acquisitions business, which has struggled to regain its health after the financial crisis.

“We’re on the radar screen of people in dozens of industries,” he said. “They know I’m interested in sizable acquisitions that break new ground, but also that our businesses are interested in expanding on their own.”

Wall Street bankers and private-equity executives say they call Berkshire more often than other potential buyers because the company’s 81 operating businesses touch nearly every industrial sector.

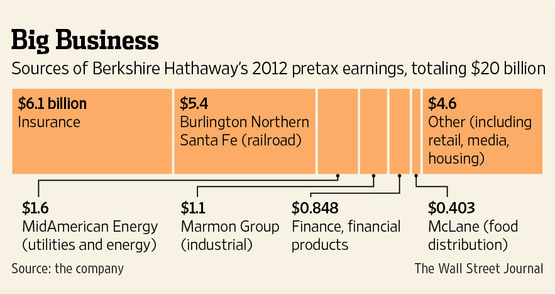

The smaller transactions are important because they augment Berkshire’s revenue and profit. In 2013’s first half, for example, revenue at Berkshire subsidiary McLane Co. rose to $22.2 billion, up 30% from a year earlier, while earnings climbed 41%, to $246 million, before taxes. The increases partly reflect McLane’s 2012 acquisition of Meadowbrook Meat Co., a food-services company.

The billionaire investor has previously said he hopes to increase Berkshire’s earnings through such deals. Berkshire CEOs say Mr. Buffett hasn’t instructed them to do deals but is encouraging and supportive of those efforts.

“He just is a terrific sounding board,” said Victor Mancinelli, the chief of farming-equipment maker CTB Inc., one of the busier deal makers in the Berkshire family, having done roughly one deal a year since Berkshire bought it in 2002.

Executives say Mr. Buffett’s hands-off approach hasn’t changed noticeably since the 2011 departure of David Sokol, a top manager and former chief of MidAmerican, where he was an active deal maker. Mr. Sokol quit after revelations he had bought shares of a company that Berkshire later acquired at his suggestion, although he said his decision to leave had nothing to do with the purchase.

Berkshire subsidiaries also use the conglomerate’s enormous cash reserves to invest in improvements to plant and equipment; this year, such expenditures are on track to exceed $10 billion, a record for the company, Mr. Buffett said.

And not every Berkshire business is an acquirer. Burlington Northern Santa Fe LLC, the railroad operator Berkshire bought for $26.5 billion in 2010, is unlikely to buy another railroad, Berkshire executives said. But it has earmarked $4.3 billion for capital expenses this year, up from $3.6 billion spent last year, according to the company.

Deals in the insurance sector, a pillar of Berkshire’s business, will also be infrequent, mainly because there are only a few targets attractive to Berkshire, and the company can build its own insurance products at lower cost, Mr. Buffett said. Berkshire subsidiaries Columbia Insurance Co. and National Indemnity Co. have snapped up small businesses in the past year.

In recent years, three of Berkshire’s five biggest noninsurance businesses have been busy acquirers—industrial-equipment maker Marmon Group LLC, MidAmerican, and specialty-chemicals maker Lubrizol Corp. CTB and engineering-products company MiTek Inc., which struck two deals in the past two weeks, are among the smaller units that make acquisitions regularly.

Tom Manenti, MiTek’s CEO, said he strives to apply the same criteria as Mr. Buffett when searching for deals, including good management. “Warren has proven that to be a successful strategy,” he said.

Some Berkshire CEOs are even looking for game for their boss.

James Hambrick, the CEO of Lubrizol, said that, while his priority is to look for targets for the chemicals maker, “I never miss an opportunity to look more broadly” for targets suited to Mr. Buffett’s big gun.