State Firms Cloud Chinese Growth Hopes

August 10, 2013 Leave a comment

August 9, 2013, 3:22 p.m. ET

State Firms Cloud Chinese Growth Hopes

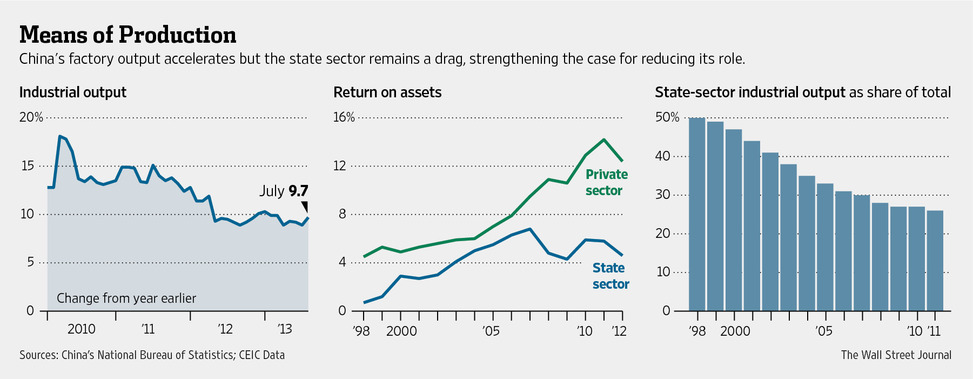

BEIJING—China added to its growing string of evidence of an economic rebound Friday with strong industrial-production figures, but the good news masked problems in its sprawling state sector that is increasingly seen as a major drag on growth. Factory output rose 9.7% in July from a year earlier, up from the June figure of 8.9%. Those results, taken together with strong trade numbers a day earlier, increasingly suggest the worst of the China’s slowdown is over. But the same data show that state-owned firms grew barely half as much as private firms—up 5.6% from 2012 for the year so far, compared with 10.9% for private firms. And all of the figures appear boosted by massive lending, which was up strongly in the first half before falling back in July. The recent decline in lending followed a cash crunch, engineered by China’s leaders to draw a line under spiraling credit.That puts a microscope on the sprawling state sector—which accounts for about a quarter of industrial output—as a potential brake on a sustained return to growth. With little fear of going under, no matter how badly they do, thousands of state firms and their millions of employees have little incentive to perform.

“I work one day a week and the rest of the time I’m chatting, drinking tea, and reading the paper,” said Guo Lirong, a 45-year-old who works full time checking electricity meters at a state-owned power company in China’s northern Shanxi province.

China’s policy makers have so far kept fundamental reform of the state sector off the agenda. But as they consider reforms for areas that weigh on growth, unproductive state firms could become a prime target.

Low worker productivity is one reason state firms generated an average 4.6% return on assets last year, compared with 12.4% for private sector firms. One in four state firms operated at a loss in 2012, compared with 8% of private-sector firms.

“No one will take responsibility for losses and the government will even lend a hand when state firms are on the edge of bankruptcy,” said Zhou Fangsheng, a researcher with a think tank tied to China’s state-owned Assets Supervision and Administration Commission, the arm of the government that supervises China’s biggest state firms.

That allows firms like China Cosco Holdings Co. 601919.SH 0.00% Ltd.—a massive state-owned shipping firm—to engage in wasteful investment that contributes to overcapacity on a global scale.

As world trade collapsed in the face of the financial crisis, Cosco ramped up shipping capacity by more than 50% from the end of 2008 to this year’s first quarter, hammering cargo prices and pushing the company into the red with losses of $1.5 billion in 2012.

Cosco says that shipbuilding orders were all placed prior to 2007.

With that wasteful investment contributing to slowing growth and rising debt, the Communist Party’s top leaders are expected to meet in the fall to hash out a series of reforms that could instill greater market discipline in the state sector.

During top-level talks with the U.S. in July, China pledged to make state firms pay market prices for land, energy and water. Beijing has also committed to make state firms cough up higher dividend payments and channel the money into social-welfare spending.

Currently, just 4% of profits for centrally owned state firms find their way into the government’s budget, according to the International Monetary Fund, while most are plowed back into expanding capacity—helping explain investment splurges like that at Cosco.

Such measures stop short of full privatization of state firms—a move that would likely encounter fierce resistance—but analysts said they could still have an impact.

Chinese state firms would have made no profit from 2001 to 2008 if they had been forced to pay market rates for capital, land and other inputs, the Beijing-based Unirule Institute estimated. Forcing them to pay market prices for inputs should incentivize higher performance.

Control of strategic sectors like energy, banking and power also has its advantages, giving the government levers it can use to control the economy. The example of Russia demonstrates that privatization of state firms can bring costs as the government struggles to tame powerful new interests.

“In China the danger of privatizing everything is that there are serious problems with corruption and the regulatory tools to constrain powerful companies are limited,” said Scott Kennedy, an expert on China’s industrial policy at Indiana University. “At least when they’re owned by their state there’s more direct control.”

As for Ms. Guo, the underutilized electricity meter worker, she’s hoping that changes can be delayed for a few more years. “State-owned enterprise reform? I know it’s good, but I hope it could start after my retirement.”