Squeezing the hourglass: Growth is back. But for many Britons, it does not feel like it

August 11, 2013 Leave a comment

Squeezing the hourglass: Growth is back. But for many Britons, it does not feel like it

Aug 10th 2013 | SOLIHULL |From the print edition

MARK CARNEY is a man on a macroeconomic tightrope. On August 7th the new governor of the Bank of England promised that interest rates will stay low until the unemployment rate, now 7.8%, has fallen to 7.0% or lower. He gave himself two get out clauses: his pledge is off if inflation gets out of hand or if Britain’s banks start to wobble. Mr Carney’s announcement reflected the balancing act demanded of him: he must spur economic confidence without allowing inflation to erode wages and savings. The severity of the slump in British living standards shows just how tricky that task will be.By some measures, the economy is moving from “rescue to recovery”—in the words of George Osborne, the Conservative chancellor of the exchequer. GDP grew by 0.6% in the second quarter of 2013 and house prices by almost 4% year-on-year. Yet the wallets of many, particularly those on lower and middle incomes, bear little evidence of it. Inflation is relatively modest, but wages lag far behind. A recent government-funded study found that 52% of Britons are struggling to keep up with the bills.

Even comfortable areas are pinched. In Solihull, a leafy suburb of Birmingham, unemployment is below average, but the cost-of-living crisis is acute. In 2010 only one client of its three Citizens Advice Bureaus (CAB) needed an emergency food parcel. Today they give out one every two days, some to people in work who run out of cash before payday. A record 16,000 people (nearly 8% of Solihull) passed through the charity’s advice cubicles in 2012. Most frequently, they sought help with debt.

One such customer, David, used to make a decent living as a skilled tradesman, but is now unemployed. He is behind on once-affordable gas, water and rent bills. His CAB adviser reckons he will never again earn what he used to, so is helping him cut costs he once considered essential, like internet access and mobile phones, from his family’s budget.

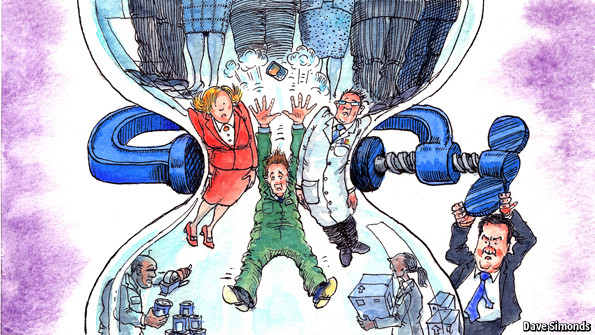

A Spartan future awaits the 40% of working-age Britons who, like David, are falling behind. They are in the bottom half of the income scale but, unlike the poorest 10%, predominantly live off wages, not benefits. Their predicament dates to the early 2000s, when GDP and earnings peeled apart. Living costs have since left median wages far behind (see chart 1).

The plate tectonics of the labour market offer the best explanation for this. With a declining industrial base, the British economy needs fewer mid-level skilled workers. Most new posts are low- or high-paying ones (see chart 2). Many in the middle lack the skills to move up and are pushed towards the low-wage end of the economy. Machinists and tradesmen become cashiers and call-centre workers.

Successive governments have bolstered the disposable incomes of the 40% with tax credits. According to the Resolution Foundation, a think-tank, in 1977 the state supplemented their wages by one percentage point of national income. By 2008-09 the top-up was 3.7 percentage points. This helped disguise the decline in the group’s share of national original income from 30% to 22%.

Today the government crows about the failings of past administrations while presiding over an intensification of the same problems. At current rates, real earnings will have shrunk by £6,660 ($10,250) over the 2010-15 parliament. The hourglass shape of the labour market has become more pronounced: research by the Trades Union Congress shows that four in five net jobs created up to December 2012 were in low-wage sectors. As before, the squeezed middle is turning to credit cards to compensate; in the first quarter of 2013 the savings ratio fell to 4.2%, its lowest since 2009.

Solihull’s economy is a microcosm of the national one. Job vacancies are up 2% on pre-recession levels, but mortgage and secured-loan arrears are 30% higher. The collapse of a local vanmaker, LDV, pushed many into low-quality service jobs. A noticeboard in a local CAB is crammed with advertisements for part-time or temporary work in supermarkets and cleaning agencies. “It’s hard for someone used to a job as a production manager on £25,000 to find themselves stacking shelves on minimum wage,” says Kerry Turner, the local head of Citizens Advice.

Desperate times, plastic measures

Such struggling voters are electorally crucial, especially in the southern and Midlands seats that swing national results (in Solihull the Liberal Democrat MP has a majority of just 175). Politicians are right to call the nationwide polls scheduled for 2015 the “living-standards election”.

Coining a phrase is one thing, living up to it is another. The Labour Party’s recent offensive on living costs was long on point-scoring and short on detailed solutions. The government boasts of its remedies (increasing the income-tax threshold and cutting beer tax, for example), but most are more than offset by the fall in real incomes. Recent education and welfare reforms are broadly commendable, but do little to change the fundamentals. Britons lack vocational skills and are underemployed. As the firms they work for invest at an alarmingly low rate, their productivity stagnates.

Ruminating on the state of the nation, Mrs Turner describes the increasing number of people who come to the CAB with plastic bags stuffed with unopened post from creditors. They ignore the letters, and take out more loans to make ends meet. Unable to kick the debt habit and unwilling to face reality, they are a reminder of what is wrong with Britain’s recovery.