Reserving a Spot in the Shifting Oil World; For oil companies, resource data are too big to ignore. They carry vital clues about what today’s oil majors will look like tomorrow

August 12, 2013 Leave a comment

August 11, 2013, 8:00 p.m. ET

Reserving a Spot in the Shifting Oil World

For oil companies, resource data are too big to ignore. They carry vital clues about what today’s oil majors will look like tomorrow.

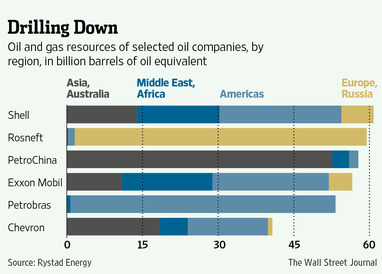

Anyone who watched “Dallas” knows it can be hard to trust oil barons. Yet investors do that every day, particularly on the question of how much oil a baron actually has. While many investors are familiar with proven reserves—which listed U.S. oil companies show in annual reports—executives are also keen to talk up the less-certain barrels beyond these. Despite their more nebulous nature, resource data are too big to ignore. They carry vital clues about what today’s oil majors will look like tomorrow. While there is no agreed definition of resources, energy consultancy Rystad Energy calculates its own estimates. Looking at a sample of 11 of the world’s biggest listed oil companies, there are clear tiers. Royal Dutch Shell,RDSB.LN +1.00% Russia’s Rosneft,PetroChina, 601857.SH +1.50% Exxon Mobil XOM -0.47% and Petróleo BrasileiroPETR4.BR +2.58% are at the top, each holding roughly between 50 billion and 60 billion barrels of oil equivalent, or BOE, under Rystad’s definition.Next sit Chevron, CVX -0.46% France’s Total and BP, BP.LN +0.33% with roughly 30 billion to 40 billion BOE each. Then come Eni of Italy, Norway’s StatoilSTL.OS +0.24% and ConocoPhillips, COP -0.39% all around 25 billion BOE.

Size matters, but the make-up of resources is key.

Rosneft and PetroChina must keep expanding abroad. They are homebody elephants with around 90% or more of their resource base in one country or region. It is also relatively mature, with roughly three-quarters already in production, against roughly 30% to 40% for the Western majors.

The two state-backed giants need diversification, both geographically and in terms of project type, suggesting they will be favorites of M&A bankers for some time.

Western majors are relatively spread out geographically. Their issue is focus.

The integrated oil business model is under pressure. As the recent struggle at Hess shows, investors aren’t convinced that scale and integration deliver value—underscored by the majors’ lousy second quarter. Deutsche Bank DBK.XE +0.52%analyst Paul Sankey says the “big-oil business model” makes most sense as a refuge when investors expect a sustained oil-price drop. These days, Exxon and Shell are essentially paying investors to stick around with big dividends and buybacks.

Sanford C. Bernstein holds out one intriguing prospect to keep the integrated major business model relevant. Rising U.S. oil output twinned with a shift in demand growth from the Western to the Eastern Hemisphere have changed how oil flows around the world. This creates trading-profit opportunities for firms with global oil production, refining and logistical infrastructure—and big balance sheets.

Only Exxon and Shell are truly global integrated majors. Despite lackluster valuations, they are unlikely to consider breaking up. Similarly, while BP, Chevron and Total lack scale and geographic spread in refining, they have large, diversified resource bases.

Smaller majors face a strategic quandary. Statoil, Eni and Conoco each has a resource base of less than 30 billion BOE and is heavily weighted to one or two regions. They must either bulk up or break up into more focused, higher-growth firms. Since they are national champions, it is unlikely Eni and Statoil would choose the latter option.

Conoco, however, which has hived off its refining business into Phillips 66,PSX -0.14% could consider a further split. Fully 69% of its resource base was in North America at the end of 2012, according to Rystad. Mr. Sankey at Deutsche Bank sees potential for a focused North American growth stock and a separate company dedicated to international deepwater and liquefied-natural-gas projects. These could be valued more highly as investors have indicated would be the case at Hess andOccidental Petroleum, OXY -0.23% too.

Resources are the basis of any oil company. But resourcefulness in how they get packaged and sold to investors is just as important.