Student-Loan Load Kills Startup Dreams

August 14, 2013 Leave a comment

August 13, 2013, 8:08 p.m. ET

Student-Loan Load Kills Startup Dreams

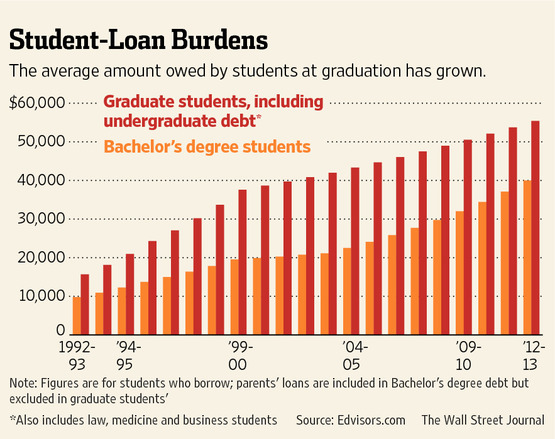

The rising mountain of student debt, recently closing in on $1.2 trillion, is forcing some entrepreneurs to abandon startup dreams and others, including Christine Carney of Orono, Maine, to radically reshape their business plans. Ms. Carney, 29 years old, and her husband, John, 31, started Thick & Thin Designs, making and selling food picks in the shapes of zombies, bikes and deer antlers after a brainstorming session while she was cooking dinner. The couple, both students at the University of Maine, where he is earning a master’s degree in fine arts and she is earning her second undergraduate degree, in zoology, sell the picks for about $12 a dozen as decorative cupcake toppers. But they chose not to purchase a laser cutter, because doing so would require them to take out a business loan—and together they have $140,000 in leftover student debt. Instead, they use a university-owned laser cutter, which limits the size of the acrylic sheets they can work with. Having the student-loan debt “is preventing me from being able to take a lot of chances or risks that are usually necessary when starting a business,” Ms. Carney says. The average student who borrows has piled up about $40,000 in debt by graduation, including parents’ loans, nearly double the levels of a decade ago, according to Edvisors.com, which runs college-planning and financial-aid websites. Recipients of graduate and professional degrees who borrow average more than $55,000 in debt at graduation, including undergraduate loans, but not parent loans. That is up from $40,800 some 10 years ago.

Some academic experts say leftover loans are the biggest impediment to upstart entrepreneurship by those who recently received college or graduate degrees. “I mentor students all the time,” says Vivek Wadhwa, a fellow at Stanford University Law School. “The single largest inhibitor to entrepreneurship is the student loans.”

Recent graduates and college dropouts account for a disproportionate share of the founders of technology startups that have transformed the economy over the past decade, says Shikhar Ghosh, a senior lecturer at Harvard Business School. Many freshly-minted M.B.A.s “are willing to sleep on a couch for a year or two, but they can’t do it with the burden of student loans,” he adds.

Jackson Solway created an online service last year to connect employers with teams of freelancers. He hoped he could sell it to companies eager to keep staffing lean. But he gave up on his new business venture this spring, after just one year. Faced with $400-a-month payments on nearly $40,000 in student-loan debt, he says he had little choice but to look for the steady paychecks that accompany a regular job.

If he didn’t face student-loan payments, he says, he would have worked at his nascent business venture for at least another six months. “I love the startup world. I would be a serial entrepreneur if it weren’t for my student loans,” says Mr. Solway, who earned a political science degree in 2009 from Colorado College.

At least one state has taken steps to alleviate the pressures. California this year enacted legislation that will reduce college costs for middle-class Californians who attend its public universities.

Similarly, the Rhode Island Student Loan Authority, a quasigovernmental nonprofit group, is looking at whether it is feasible to temporarily forbear or reduce payments for recent graduates who start a businesses or go to work for a new venture. The aim is to give recent graduates “the opportunity to try working for a startup or creating a startup instead of having to run off to Arizona and start working for Intel,” says Charles P. Kelley, Risla executive director.

Starting a new venture is a big risk, of course. For most entrepreneurs, the biggest challenges are “starting and getting your company a corporate life” and “getting market traction,” says Dane Stangler, director of research and policy for Ewing Marion Kauffman Foundation, a Kansas City, Mo., nonprofit that studies entrepreneurship.

Like other borrowers, entrepreneurs struggling to make federal loan payments may be able to take advantage of deferments or forbearance to temporarily delay their loan payments, though, in many cases, interest will continue to accumulate. The federal government also offers several programs that let borrowers tie monthly loan payments to income. Options for borrowers with private loans are more limited.

Sara Gragnolati, 36, accumulated more than $90,000 in federal and private loans, most while earning an M.B.A. from Babson College in 2010. Her Boston-based company, Cocomama Foods Inc., now sells its gluten-free hot cereals in about 300 stores and is getting ready to launch a second product line, crunchy dried cereals made of grains such as quinoa, millet and flax. But while business is expanding, Ms. Gragnolati still isn’t drawing a salary. Although she has been deferring payments, she must begin repaying $200 monthly on her private student loans in November. She hopes she can either continue to defer the $559 monthly payments on her federal loans, or perhaps make reduced income-based payments. Figuring out the best way to manage student loans is difficult, because loan programs “don’t really recognize my entrepreneurship,” she says.

Levi Belnap and Alex Pak graduated from Harvard Business School in May with $250,000 in student loans between them. The pair have received $200,000 in seed capital for FindIt, which helps users locate emails and documents on their iPhones. With loan payments coming due this fall, they will soon have to seek additional funding. “It’s basically forced us down a path, for better or for worse because of that debt burden,” says Mr. Belnap, 29, who is married and has two young children. “We have real responsibilities that we have to face.”

Some entrepreneurs view their student-loan payments as a motivator. “We are under the clock to get our product out there and make sales,” says Andrew Torba, co-founder and chief executive of Kuhcoon, a tool for managing social media.

Mr. Torba, 22, a philosophy major who minored in entrepreneurship and political science, graduated from University of Scranton in May with $30,000 in debt. His loan payments kick in this November, when the standard six-month grace period for most student loans ends. Student-loan payments are “pushing me forward,” he says. “I’m making sure that I make every single day count.”