Chinese Banks Feel Strains After Long Credit Binge; Rapid Loan Growth Has Led to Serious Debt Problems at Local Governments

August 15, 2013 Leave a comment

Updated August 14, 2013, 6:05 p.m. ET

Chinese Banks Feel Strains After Long Credit Binge

Rapid Loan Growth Has Led to Serious Debt Problems at Local Governments

LINGLING WEI and DANIEL INMAN

A cornerstone of China’s financial edifice is beginning to show some cracks. The country’s banking sector, a key part of a financial system that has powered China through three decades of breakneck expansion, is feeling the strain of years of rapid credit growth. Bank-fueled lending to state enterprises and local governments has led to overcapacity; serious debt problems for local governments, companies and lenders alike; and numerous white-elephant projects, from nearly empty malls and resorts to bridges to nowhere.

Chinese banks now are trying to strengthen their balance sheets ahead of an expected rise in bad loans coupled with slower earnings growth. Raising capital will likely be expensive for the banks because investors, who have sold off shares of banks, are worried about their deteriorating health and China’s slowing growth.“The problem [banks] face is that market sentiment is very bad,” says Mark Mobius, executive chairman of Templeton Emerging Markets Group, a part of Franklin Templeton Investments, who manages more than $50 billion of emerging-market equities

The weakness at the banks is a major part of broader problems in China’s financial sector. Many investors worry about the surge in off-balance-sheet loans employed by banks as a way to get around official lending limits, keeping the credit flowing to local governments and other high-risk borrowers. The surge in such “shadow-banking” activities prompted China’s central bank to allow interbank borrowing costs to rise sharply in June—an attempt to rein in reckless lending. With short-term borrowing rates spiking close to 30%, banks scrambled for funds, triggering near-panic in China’s broader equity and bond markets.

In a bid to beef up their capital base, the country’s four largest state-owned banks by assets—Industrial & Commercial Bank of China Ltd., China Construction Bank Corp., Agricultural Bank of China Ltd. and Bank of China Ltd.—recently won board approval to issue up to a total of 270 billion yuan ($44.1 billion) in securities in the next two years. The figure is bigger than the total amount of issuance by the Big Four in the past two years.

But the push to raise more capital comes at a time of weak market sentiment. The Hang Seng China Enterprises Index, which tracks Chinese companies listed in Hong Kong and is heavily weighted toward the banking sector, is down 10.9% year to date as of Wednesday.

China’s state-run banks have long provided the fuel for the engine that powered China to become the world’s second-largest economy. In the process, they surpassed their Western rivals in market value, as investors scrambled to buy a piece of the country’s growth. Based on market capitalization, four of the 10 largest banks in the world are Chinese.

Much of that growth was built on politically directed lending. Some of it ended up establishing globally competitive industries ranging from steel to energy to solar panels. But a large portion also was used to build highways, railroads and other infrastructure projects sponsored by local governments.

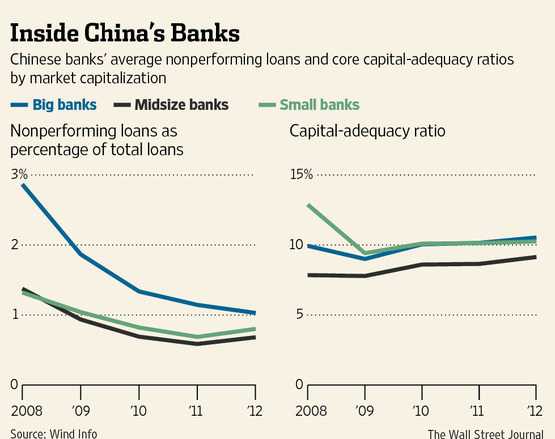

Assets in China’s banking sector jumped 126.5% to about $21 trillion as of the end of last year from four years earlier, making it the fastest-rising banking system among emerging economies, according to Fitch Ratings Inc. But it also is the most thinly capitalized among those economies, with the amount of equity representing only 6.5% of total assets in China’s banking system. By contrast, equity represents an average of 11.2% among 48 emerging economies.

Chinese regulators are taking note. In a rare interview with state broadcaster China Central Television on Aug. 2, Shang Fulin, chairman of the China Banking Regulatory Commission, acknowledged that important risks stem from loans to local governments and those created outside banks’ balance sheets.

Mr. Shang said Chinese banks have to deal with a large quantity of maturing local-government debt this year. Many banking analysts have warned that some local governments may run into trouble repaying their bank loans due to slumping revenue from their land sales—a main source of income for Chinese governments. Mr. Shang said the commission will come up with ways to help banks “control that risk.” So far, many Chinese banks have resorted to extending maturing loans to avoid defaults.

Mr. Shang also said the agency is monitoring “very closely” the risks posed by banks’ off-balance-sheet lending activities. But overall, the risks are “manageable,” Mr. Shang said, and added, “China’s banking industry remains relatively stable and healthy.”

Still, Chinese banks are seeing greater needs for capital as a weakening economy leads to slower profit growth and increases the prospects of more bad loans.

“For many Chinese banks, they are growing faster than their earnings can keep up with contributing to their capital base,” said Charlene Chu, senior director of Fitch in Beijing.

A new report issued by the China Banking Association, a trade group, shows that Chinese banks likely will see net-income growth decline to about 8% this year because of smaller profits from loans and an expected increase in nonperforming assets. In 2012, China’s banking industry generated 1.51 trillion yuan in net profit, up 21% from a year earlier. Net profit at the Big Four banks rose at an average compound annual growth rate of 28% in the five years to the end of 2012.

Most of the securities sales planned by the top four banks involve a kind of debt that banks can use to meet capital requirements and absorb losses from bad loans under new global and Chinese banking rules. The banks are seeking debt that doesn’t mature for at least five years, providing a more stable source of liquidity than the short-term funds they lend to one another.

Some of the Big Four banks, including Bank of China, are considering selling the debt in markets outside mainland China, to tap deeper liquidity and a broader investor base than the mainland market. Traditionally, Chinese banks have largely turned to the mainland to raise funds.

A recent analysis by ChinaScope Financial, a research firm partly owned by Moody’s Corp., shows that China’s banks would have to raise between $50 billion and $100 billion through equity sales in the next two years to maintain their current capital-adequacy levels.

“When the banks are expecting to see lower returns on equity, they would need to either restrict the expansion of their balance sheet or prepare to raise more capital,” says Tom Liu, chief executive of ChinaScope.