Critics point to China’s bond market as an underrecognized risk as the country struggles to control surging lending amid a weakening economy

August 16, 2013 Leave a comment

August 15, 2013, 1:12 p.m. ET

Critics Decry Risks Posed by Link Between China’s Banks and Bonds

The Market ‘Is Like a Child Compared to That in Other Countries’

SHEN HONG

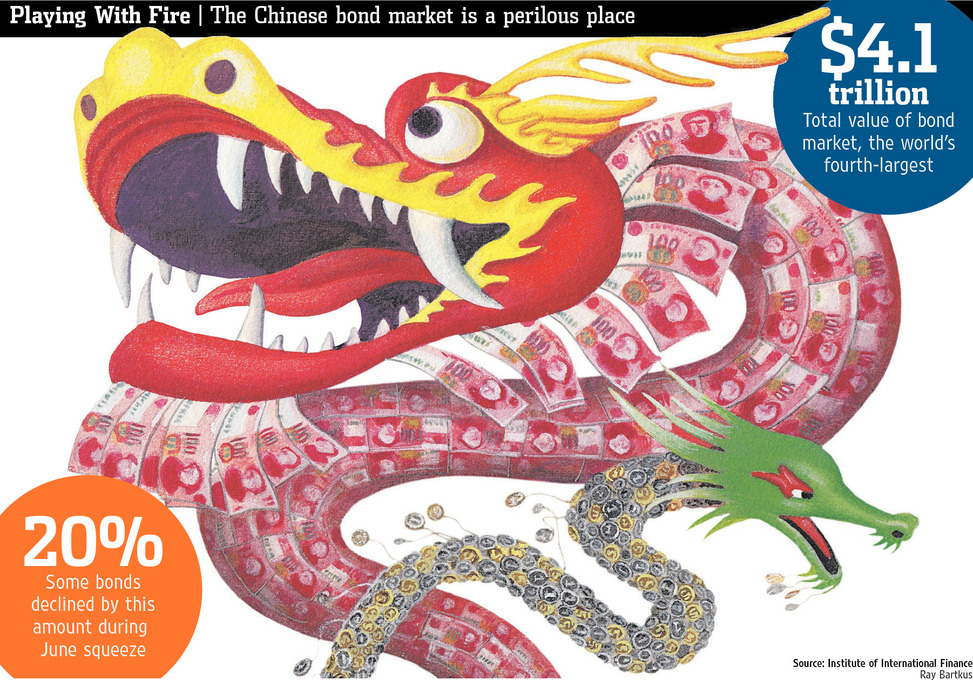

SHANGHAI—Worried about a boom in lending by the country’s fast-growing “shadow banks,” China created a cash crunch in June to squeeze their source of funding. One unintended consequence, though, was a selloff in the country’s $4 trillion bond market. The selloff—triggered by banks selling bonds to raise cash—bolstered critics of China’s financial system, who point to its bond market as an underrecognized risk to the country as it struggles to control surging lending amid a weakening economy. China’s bond market has quintupled in size to 25.5 trillion yuan ($4.1 trillion) since 2004, driven most recently by the Chinese government’s stimulus plan to combat the impact of the global financial crisis.The market trails only the U.S., Japan and France in size, according to the Institute of International Finance, a bank trade group. But it hardly resembles a modern bond market. It is overseen by a patchwork of regulators, is largely closed to foreign investors, offers few protections for investors and has a bond-ratings system where nearly every company gets top scores and bonds are rarely downgraded.

“China’s bond market is like a child compared to that in other countries,” said Jing Wang, deputy general manager of fixed income at Goldstate Securities Co., a midsize securities brokerage based in Shenzhen. The company has pared back its holdings of Chinese bonds following the selloff, because it has concerns about near-term volatility and “the lack of transparency in the market” in the long run, he said.

Most worrisome to critics is that most bonds are held and traded by the country’s banks, effectively concentrating risks in the banking system that in most other countries are spread out among investors.

“Banks are the biggest holders of bonds in China, including those of local governments. So if there’s a default by a local government, their risk will be multiplied because they also issue loans to the latter,” said Ivan Chung, analyst at Moody’s Investors Service.

The spring cash crunch was instigated by China’s central bank to rein in a lending boom that was going on outside the banking system but got some of its funding from banks. By allowing interbank loan rates to surge, the central bank squeezed the market for loans between banks, leaving some of them scrambling for cash. The bond market was drawn into the turmoil when some lenders rushed to sell bondholdings, especially short-term bonds, which tend to be more liquid.

Because there were few buyers, prices fell as much as 20%, and daily trading volume dropped from an average of 233 billion yuan this year to 15.6 billion yuan on June 9. Prices and trading volume have since bounced back, but critics say the episode showed how disruptions in the financial system can ricochet.

“The goal of developing the bond market is to reduce the dependence on banks for funding, but at the end of the day the risk is back to banks again,” said Shuang Ding, an economist at Citibank.

That hasn’t proved to be a problem yet, because no bond issuer in China has ever defaulted. Shandong Helon Co., 000677.SZ -1.84% a chemical-fibers maker in northeast China, came close last year. The company failed to pay back several loans and was downgraded by credit raters.

It was saved when Evergrowing Bank, whose biggest shareholder is a state-owned company, underwrote a bond offering whose proceeds were mostly used to repay the loans, according to the National Association of Financial Institutional Investors, a money-market regulator that later disciplined Shandong Hleon for alleged accounting fraud and misuse of bond proceeds.

An official from Shandong Helon said the people who were involved in managing its loans and bonds have left and the company has been restructured. The official declined to comment further.

One area of concern is the bond market’s overly optimistic bond ratings. A lax ratings system “makes it hard for professional bond investors to maximize their strengths in credit quality and pricing evaluation,” said Wang Yingfeng, head of trading and investment at Shanghai Yaozhi Asset Management, which manages about 2 billion yuan ($327 million) of assets.

Since 2000, 124 of 2,908 corporate-bond issuers were downgraded in China. Of those issuers, 2,444 are rated single A and above, according to the latest data from Financial China Information & Technology Co. In the U.S., Moody’s downgraded 240 bond issuers last year alone. Of more than 2,000 issuers as of July 1, just 420 were rated single A or above by Moody’s.

There are three regulators for the three different types of bonds traded in China. The country’s central bank oversees the issuance of short-term bills and medium-term notes. The National Development and Reform Commission, China’s top economic-planning agency, approves sales of the so-called enterprise bonds by the country’s large state-owned companies.

The last and smallest category is corporate bonds, which are issued by listed companies, approved by China’s securities regulator and traded on the exchanges only.

“Having multiple regulators requires a lot of coordination among them because they all have their own sets of criteria that cater to their own risk-management requirements,” said Terry Gao, an analyst at Fitch Ratings.

Issuance in the Chinese bond market is dominated by local governments and state-run enterprises, with few private companies able to issue debt. Bonds from state-run enterprises jumped 60% last year and accounted for 92% of the corporate-bond market, data from Financial China showed. Outstanding local-government debt totaled 10.7 trillion yuan as of the end of 2010, according to the latest data from China’s National Audit Office.