Rising credit yet falling NPL ratio; Flood of problem loans to stretch China’s bad banks

August 16, 2013 Leave a comment

August 15, 2013 4:29 pm

Flood of problem loans to stretch China’s bad banks

By Paul J Davies in Hong Kong

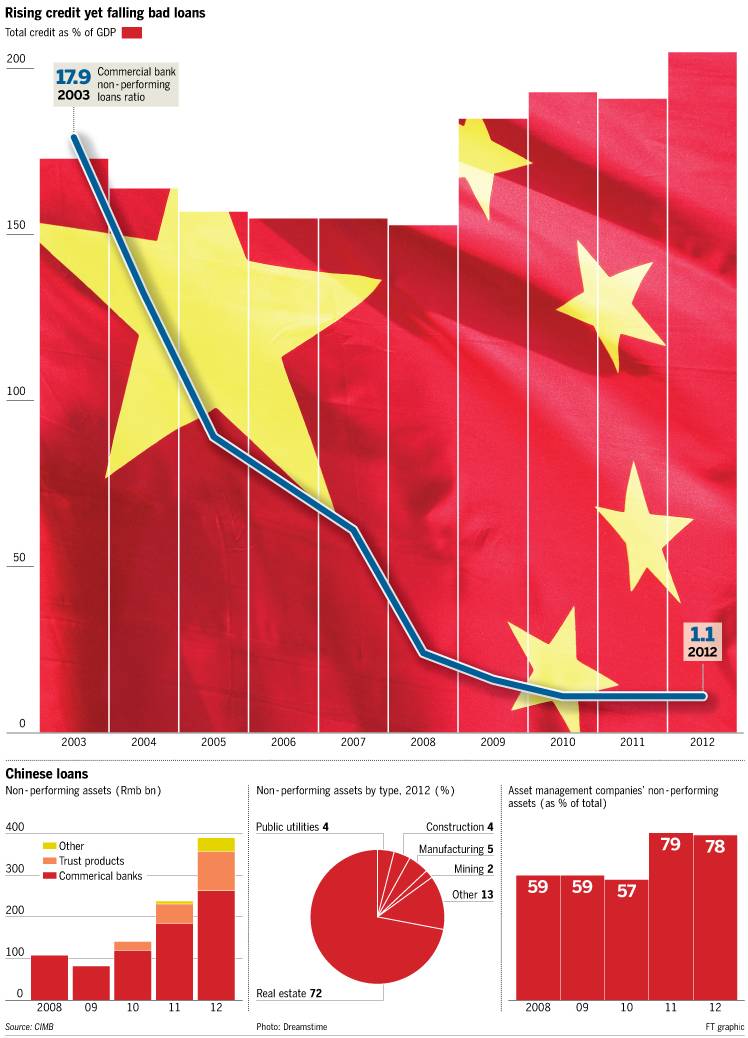

When Goldman Sachs economists wanted to bring their global clients up to speed on the risks in China’s credit boom, they spoke to Charlene Chu, the Fitch Ratings analyst known for her bearish views. Ms Chu has studied China’s shadow finance sector to come up with one of the highest estimates of the country’s debt pile at more than 200 per cent of gross domestic product. She also warns that the banking sector is far more exposed to many of the shadow loans than most people realise. The latest official figures show non-performing loans (NPLs) at Chinese banks grew by Rmb13bn ($2bn) in the second quarter to Rmb540bn, increasing for a seventh straight quarter.More than a decade ago, Beijing set up four state-funded asset management companies (AMCs) to take over the bad debts of the four biggest state-owned banks. After a rocky start, the bad banks have become adept at working out problem loans in only the past couple of years, according to bankers.

Profit figures are hard to come by for these privately held companies, but Trevor Kalcic, analyst at CIMB, reckons their combined return on equity has increased from 8.9 per cent in 2009 to 15.5 per cent last year. He also calculates that the four saw total pre-tax profits grow by 29 per cent last year.

“The AMCs are now already playing an important and largely unrecognised role in solving the country’s bad debt problem,” Mr Kalcic says. “This is probably one of the key reasons why the system-wide NPL balance has remained relatively low in spite of the large increase in system leverage in recent years.”

Now, two of those AMCs, Cinda and Huarong, are raising fresh private capital in order to play a much bigger role in the next round of bad debts that are expected to emerge from the huge expansion in lending that has taken place in China since 2008.

This will not only come from the commercial banks but also from wealth management and trust products and from the balance sheets of ordinary companies which are owed money by other businesses unable to pay it back.

Cinda and Huarong were set up to take on the bad debts of China Construction Bankand Industrial and Commercial Bank of China, respectively.

For the love of bad banks

Why would investors want to buy shares in a bad bank? Especially one from Chinawhere things financial are almost never entirely clear and transparent.

According to bankers involved, Cinda and Huarong, which are both moving towards initial public offerings in Hong Kong, make their best profits these days from working out bad debts, having become quite adept at it.

Their other sources of income are from the huge array of financial industry licenses they have picked up over the years to provide other revenue streams. These include everything from securities dealing to lease financing, insurance and private equity.

But it is the debt work out that brings in the most, bankers say. “As an investor, if you hate the Chinese banks because of concerns about their asset quality then you should love the Cindas and the Huarongs for the other side of that trade,” one says.

Trevor Kalcic at CIMB reckons Cinda, Huarong and their two bad bank peers now make returns on equity of more than 15 per cent – better than most banks in the west.

However, one thing to note is that in past couple of years, the Ministry of Finance, which set these vehicles up originally, has taken over a chunk of their original liabilities – Rmb560bn worth according to CIMB.

This role in buying a broader set of non-performing loans and receivables from across the financial sector is what many bankers and analysts see as the market-based future of how China will deal with bad debts.

China at present lacks significant players to ensure the next round of working out non-performing loans will be market-driven. But “when Cinda and Huarong are privatised and become more professional, they are expected to become a force in the NPL markets”, says one senior Hong Kong-based banker not involved with Cinda or Huarong’s capital raisings.

Mr Kalcic says the government is preparing these businesses to play a bigger role in working out some of the problem assets in the financial system. After the capital raisings, and further increases in leverage, the four AMCs combined could take up to Rmb1.2tn of non-performing loans or assets out of the financial system, which equals 1.85 per cent of total bank loans outstanding.

“We believe the four AMCs combined have a significant capacity to assume bad debts from the banking system as well as poor credit from the broader economy,” he says.

In 1998, when these AMCs were formed, the first Rmb1.4tn batch of bad loans were bought at face value, or 100 cents on the dollar, which was great for the big four banks, but less good for the bad banks. They recovered only about 20 cents on the dollar.

However, in the late 1990s, that Rmb1.4tn accounted for about 15 per cent of bank loans, according to CLSA. Ms Chu calculates that the Chinese banking system’s assets grew by $14tn between 2008 and 2013 – equivalent to adding the entire US banking system to its banks’ balance sheets.

This illustrates why China needs more than merely a government bailout to tackle bad loans this time and that it will probably take a lot more than four privatised AMCs.

“There is tremendous confidence in the ability and the willingness of the Chinese Communist party to bail everyone out,” Ms Chu said in Goldman’s flagship economics and strategy publication last week. “But as the system gets bigger and bigger, there are more questions about how feasible that is.”

August 15, 2013 4:38 pm

China moves towards market remedy for bad loans

By Paul J Davies in Hong Kong

Goldman Sachs, Deutsche Bank and Morgan Stanley have held talks with one of China’s biggest bad banks about investing in its $1.5bn stake sale ahead of a planned Hong Kong listing next year, according to people close to the process.

The move is one sign that the Chinese government will not entirely bail out the next round of problem loans emerging from China’s credit boom, but will instead rely more on market driven remedies.

The capital raising by state-owned Huarong is expected ahead of an initial public offering of its larger bad bank cousin, Cinda, later this year.

Goldman Sachs is leading the race to take the lion’s share of the stake in Huarong, according to two people close to the deal. However, another banker with knowledge of the process said only a couple of meetings had been held so far and a deal is not expected until December. The three banks declined to comment or could not be reached, while Huarong declined to comment.

Huarong and Cinda are two of four asset management companies set up by the Chinese government in 1998 to take on Rmb1.4tn ($229bn) of non-performing loans from the country’s four biggest banks. Huarong bought bad loans from Industrial and Commercial Bank of China, while Cinda bought debts from China Construction Bank.

The four bad loan managers were lossmaking for many years, but since the huge stimulus programme launched by China in 2008, they have converted many old debts into equity stakes and made attractive returns, according to bankers familiar with the businesses.

Cinda, for example, saw pre-tax profits of Rmb7.2bn in 2011 and Rmb4.6bn in the first half of 2012, according to ChinaScope Financial, a specialist research service that compiles data on public and private Chinese companies.

Goldman, Deutsche Bank and Morgan Stanley have all formed joint ventures with Huarong to buy its bad loans in the past, while Deutsche Bank still has an active joint venture with the asset manager. Goldman was also a big investor in ICBC ahead of its part-privatisation, only selling the final part of its holding this year.

Cinda, which last year sold a $1.6bn stake to four strategic investors including UBSand Standard Chartered, is in the process of finalising its prospectus and hopes to launch an IPO this year in Hong Kong, according to bankers close to the process.

Cinda aims to raise $2bn-$3bn, which would value it at about $15bn, according to a banker involved in the process. Huarong is planning for a Hong Kong IPO as early as next year, once it has strategic investors in place.

The money raised by Cinda will be used to replenish its stock of bad loans, and it can borrow against its new equity to increase its purchasing firepower. “Cinda can leverage up its money by 6-8 times, so the IPO proceeds at the low end would allow it to buy $12bn-$16bn of NPLs (non-performing loans),” said the banker close to the process. “We think there will be a lot of NPLs coming out of the banks in the next three to four years.”