Banks Work Around China’s Lending Limits; Latest Tactic in Cat-and-Mouse Game With Regulators Hides Risks, Analysts Say

August 20, 2013 Leave a comment

August 19, 2013, 12:38 p.m. ET

Banks Work Around China’s Lending Limits

Latest Tactic in Cat-and-Mouse Game With Regulators Hides Risks, Analysts Say

CYNTHIA KOONS and DINNY MCMAHON

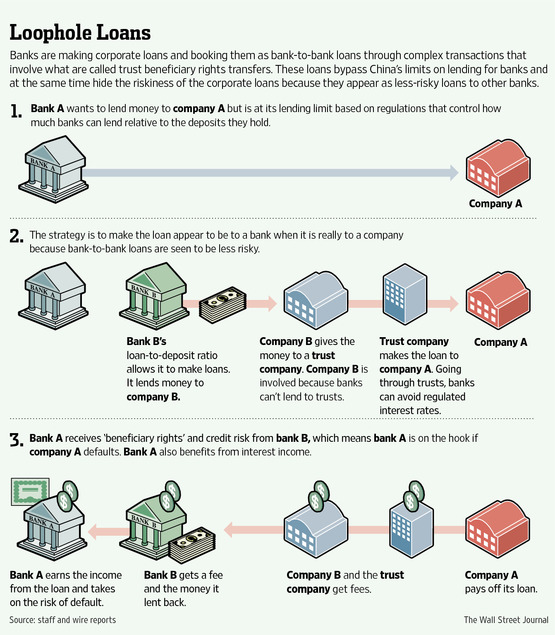

Chinese regulators have tried for months to rein in lending by the country’s banks, most recently by instigating a cash squeeze that left some scrambling for funds. But the banks have stayed one step ahead, keeping the lending spigots open largely through increasingly complicated transactions. The banks’ latest effort in their cat-and-mouse game with regulators involves making corporate loans appear on their balance sheets as less risky loans to banks. This allows banks to skirt limits on lending to customers but hides risks that they will be hit by big losses.Analysts estimate as much as 2 trillion yuan ($326 billion) could have been lent under these transactions, which are often categorized as so-called trust beneficiary rights transfers because the income and risk from a loan is transferred between banks.

The transactions are done mostly by small and midsize lenders, which were the target of the Chinese central bank’s credit squeeze in June.

“What worries me is the way banks are getting around regulations is becoming more and more convoluted,” Fitch China banking analyst Charlene Chu said. “If these exposures encounter a problem, it will be really hard to sort out.”

Investors have become increasingly skeptical of Chinese banks, largely because they don’t believe the banks’ claims that they will have only modest losses on loans they have made. Shares in most Chinese banks are trading at or below book value, a sign investors believe losses will rise.

Analysts and critics of the practice say the loans themselves often are of lower quality than typical loans, and are often made to borrowers that the government is trying to wean off easy credit, including shipbuilders, steelmakers and local governments. These loans could lead to “higher credit risks for China banks, primarily due to the more relaxed underwriting standards, weaker credit protection and weaker post-lending management compared to normal bank loans,” analysts at the regional brokerage CIMB said in a note to clients.

Banks and other investors holding assets that were riskier than they appeared were one factor that caused big losses in the global financial crisis. Lenders, insurers and other market participants held complicated financial products that were considered safe, but were stuffed with risky mortgages that ultimately recorded far higher losses than expected.

The China Banking Regulatory Commission didn’t respond to questions.

While few banks disclose these transactions, analysts say that Shanghai-listedIndustrial Bank Co. 024110.SE 0.00% and Hong Kong-listed Chongqing Rural Commercial Bank Co., 3618.HK -0.55% two midsize lenders, are among the most active users of the process. Neither bank would comment.

The end-June financial statements of Industrial Bank, which discloses more than most other banks about the extent to which it is using the lending tactic, suggests the volume of corporate loans accounted for as interbank loans may have doubled from a year earlier. The transactions, recorded under “trusts and other beneficiary interests,” were equivalent to 32% of the bank’s outstanding loans at the end of June, up from 20% a year earlier.

There isn’t official data on the amount that banks are lending to companies through this backdoor method, but executives at two trust companies—a key link in the process—said that it accounts for about 30% of their business. In the second quarter, trusts issued 724.6 billion yuan worth of new products. Estimates of the total amount of outstanding loans done through these trust arrangements range from 1 trillion to 2 trillion yuan, but it is impossible to get exact figures due to limited disclosure.

Analysts say the process allows banks to skirt regulations that limit the amount of loans to customers they can make to 75% of the deposits they hold.

According to bank analysts and people involved in packaging such loans, the process involves one bank transferring the income stream and credit risk from a corporate loan to another bank. The bank transferring the loan gets a fee and holds the loan on its books, but doesn’t bear any risk.

The loan is booked as a bank-to-bank loan rather than a corporate loan, so it doesn’t count against the lending limits imposed by bank regulators.

More important, the bank is allowed to set aside less capital to cushion against a loss because the loan is to a bank, which is considered safer than a loan to a company.

As a result of other regulatory restrictions, several steps are required to make the bank-to-bank loan. First, a trust, considered part of the “shadow banking” system, makes the loan. But because banks aren’t allowed to lend to trusts, another company takes the loan from the trust and then transfers the right to collect the income stream from the trust—known as trust beneficiary rights— to a bank. That bank then sells the trust beneficiary rights to the bank that wanted to make the loan in the first place.

To make the loans, the banks tap the surging bank-to-bank lending market, in which smaller lenders borrow from big, deposit-rich banks, so they can keep lending. The interbank lending market is what regulators tried to rein in during the June cash crunch.

Sophie Jiang, an analyst at Asia-focused brokerage Religare Institutional Research, said banks would suffer if regulators forced the banks to account for the true risk of these loans on their balance sheets. “I don’t think right now this amount could be pushed onto banks’ balance sheets,” Ms. Jiang said.

The June cash crunch in China was an effort by regulators to rein in lending among banks, which has soared in the past two years. Lending between banks is typically short-term and used by the banks to manage their liquidity. But because so much of this lending has been used to fund long-term loans to companies, banks were vulnerable to squeezes in the bank-to-bank lending market. Some grew so desperate for cash to fund their long-term loans that they offered annualized returns of more than 25%. The central bank eventually made cash available, bringing lending rates back down.