Asia 1997 vs. Asia 2013

August 22, 2013 Leave a comment

August 22, 2013, 3:48 AM

Asia 1997 vs. Asia 2013

By Alex Frangos

It seems all too familiar. Currencies are plunging. Current account deficits are widening. Central bankers are tripping over themselves to settle markets. So is this the 1997-98 Asian Financial Crisis redux? For one economist who lived through the crisis, history isn’t repeating itself just yet. “If the Asian financial crisis was a 10. I’d still be on a 3. My instinct is this is a short term portfolio adjustment that will pass,” says Stephen Schwartz, chief Asia economist for BBVA. He saw the Asian financial crisis up close as an International Monetary Fund staffer covering the region, and later lived in Indonesia working for the IMF as Asia licked its wounds during the 2000s.

“These episodes are comparable only in the sense that it was a period of big capital inflows and then outflows. But the underlying conditions are very different from 1997,” he says. To be sure, having lived through 1997, he’s reluctant to sound an all clear: “I don’t want to minimize the difficulties.” Policy missteps, like those seen in India the past week, have a way of letting matters spin out of control.

Recent turmoil in some Asian emerging economies is certainly troubling and one lesson from every crisis is to expect the unexpected. Foreign investors, who flooded into the region the past five years, are turning tail from places like Indonesia, Malaysia and Thailand.

India’s currency has plunged 15% against the dollar since May, when the U.S. Federal Reserve signaled it might cut back its bond-buying stimulus program. That’s tightening credit and raising worries that an economic slowdown already underway will get worse in the countries affected.

Here are several ways 2013 is different from 1997:

1. Floating exchange rates. Unlike 1997, economies in Asia for the most part don’t maintain currency pegs, which are hard to defend against speculators. So when the rupee or baht or rupiah drops 10%, it might hurts investors and unnerve businesses in the short term. But in the medium term, it can be a relief valve for the economy, making goods more competitive on the world market and encouraging local consumers to import less. It also lets central banks preserve their foreign exchange reserves to pay for imports and foreign debt.

2. Foreign reserves. The war chests central banks hold are substantially larger than 1997. While India’s central bank has taken criticism for not building up its reserves even higher, at $254 billion, they are hardly negligible. Thailand, epicenter of the 1997 crisis, has $170 billion today, compared to essentially zero when it was bailed out by the IMF.

3. Transparency. Back in 1997, Thai authorities didn’t disclose $30 billion in bets the country had made in currency forward markets. “It came as a shock even to the IMF team that the Bank of Thailand had effectively run out of reserves,” says Mr. Schwartz. “Today all these countries provide detailed data on reserves, on nonperforming loans in the banking system. That allows markets to react much earlier and adjustments are less abrupt.”

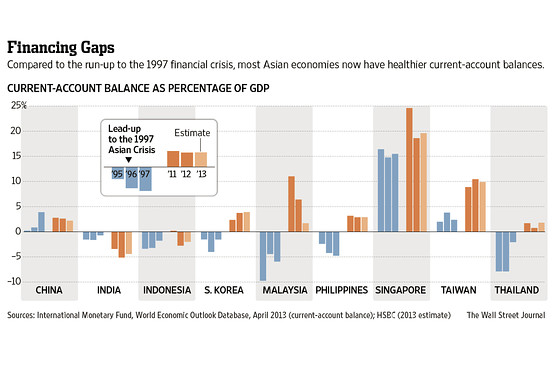

4. Current account balances. The current account measures whether a country needs to attract foreign capital to keep its financial system afloat. Things have deteriorated in this regard for India and Indonesia, and to a lesser extent Thailand and Malaysia. But compared to 1997, the problem is far less wide spread. In the three years before the crisis, Hong Kong, India, Indonesia, South Korea, Philippines, and Thailand all ran substantial deficits, some in double digits. Today, Hong Kong, Philippines and South Korea are in surplus and Taiwan’s surplus has grown even larger than 1997.

5. Foreign debt. This was the killer in the Asian crisis. Companies, banks and governments had borrowed vast sums in dollars, but their revenue was in local currencies. When currencies devalued, companies and banks were unable to pay back the debt. While debt levels have risen the past few years, most of it has been in local currency. So if you’re a Thai consumer who borrowed 1 million baht to buy a house, baht weakness against the dollar is unlikely to affect your ability to repay the loan. That doesn’t mean the dollar outflows won’t cause some casualties, but the pervasiveness of the damage is likely to be less.

South Korea especially has greatly reduced the liabilities its banking system has to short-term foreign currency debt. That could explain why the nation has actually seen capital inflows the past few weeks even as Southeast Asia suffers.

6. Banking reform. In the 1990s, banking supervision was primitive by today’s standards, with money being thrown around at dubious ventures. “The quality of the usage of the funds was weaker than now. There were currency mismatches, duration mismatches and investments in the wrong sectors,” says Mr. Schwartz. In Indonesia and South Korea, coziness between banks and companies led to bad lending decisions. While there’s still bad lending decisions everywhere, the oversight is much tighter. For evidence, look no further than the curbs authorities have placed on lending in speculative areas, such as auto sales in Indonesia, consumer loans in Malaysia, and property loans in Singapore and Hong Kong.