Hot Potato: Momentum As An Investment Strategy; momentum’s strength has eroded over the past decade. Factor-based investing requires strong conviction and a steady hand

August 24, 2013 Leave a comment

Hot Potato: Momentum As An Investment Strategy

August 2013 | Ryan Larson

Momentum investing has important features in common with other factor-based Smart Beta strategies. For example, it has straightforward index or portfolio construction rules that are easily explained and implemented. And, although momentum investing is emphatically not a contrarian strategy, neither is it necessarily inconsistent with the Smart Beta thesis that prices are noisy and mean-reverting. In this interpretation, momentum investing is a lively game of hot potato—buying rapidly appreciating stocks, holding them for a relatively short period, and selling them before their price trends reverse direction. And in favorable conditions it works very well.Nonetheless, our research raises serious theoretical and practical questions about momentum as an investment strategy in its own right. In this issue, I review the evidence for momentum investing, consider momentum in comparison with other equity risk factors, and briefly touch upon implementation issues, including portfolio construction and rebalancing policies. I argue in favor of choosing another factor for the core investment strategy and using momentum only as an ancillary trading strategy.1

Evidence and Explanations

Momentum has shown itself to be quite robust across U.S. and foreign equity markets, within industries and countries, and across many different asset classes such as stocks, currencies, commodities, and bonds. In 1993, UCLA professors Narasimhan Jegadeesh and Sheridan Titman (1993) published what is considered to be the first comprehensive study of the momentum effect. They found strong evidence, over the 1965–1989 period, that stock prices trend—at least in the “short-term” of up to two years. In Jegadeesh and Titman’s study, the best performing portfolio selected stocks on the basis of the previous 12 months of price returns, bought winners, sold losers short, and held those positions for the subsequent three months.

Other academics confirmed that momentum is at work in international equities, emerging markets, industries and sectors, mutual funds, and asset classes.2 In fact, commodity trading advisors (CTAs) have built a profitable business around trading momentum.3

Empirical studies have shown the momentum effect to be strong, but financial theory hasn’t definitively explained why momentum exists. Describing investors’ behavioral tendencies in the 1970s, Daniel Kahneman and Amos Tversky (1979) identified what they called the “anchoring and adjustment” heuristic.4 In the face of uncertainty, individuals estimate the expected future value of an asset by making adjustments to a reference price, that is, an “anchored” value. Investors manifest this tendency by anchoring to the current information (stock price) and being slow to adjust expected future values in light of new information. Thus, prices lag fundamental information and play “catch up” for a few quarters, leading to serial correlation in stock prices. Jegadeesh and Titman concluded that an under-reaction to firm-specific information was the likely cause of momentum. In further support of the anchoring hypothesis, Hong and Stein (1999) found that it takes time for information to be fully reflected in stock prices.

Other financial and psychological considerations may also prolong momentum by postponing price adjustments due to new information. Tax liabilities might make it preferable to defer the realization of capital gains. Company insiders may decide it is prudent to reduce their holdings over an extended period. Investors’ sentimental attachment to a company may discourage them from divesting the stock. (For instance, an individual might have inherited the stock, or the officers of a charitable organization may be loath to sell the stock of their founders’ company.) Serial correlation in earnings announcements might also lead to stock price momentum.5

Taken one by one, these insights make good sense. However, there isn’t a generally accepted theory that explains the causes of momentum in the financial markets. For example, it is not clear why the anchoring-and-adjustment heuristic would prevail over another psychological trait—investors’ tendency to overreact to new information. Nor is it clear that behavioral patterns which are perceptible in individual decision-making can be applied by simple extrapolation to untold numbers of investors interacting with one another.

The lack of a cogent theoretical explanation is not a trivial matter. Maintaining that, because the stock price has risen, it will continue to rise—as though the conservation of linear momentum applied, by analogy, to financial assets—is scientifically dubious. After all, an investment thesis that supports buying stocks solely on the basis of past prices violates even the weak form of the efficient market hypothesis. More than just a beauty contest, investing becomes Keynes’s (1936) third degree of speculation:

It is not a case of choosing those [faces] that, to the best of one’s judgment, are really the prettiest, nor even those that average opinion genuinely thinks the prettiest. We have reached the third degree where we devote our intelligences to anticipating what average opinion expects the average opinion to be.

Momentum as an Equity Risk Factor

From our vantage point, it appears that investors are starting to look at equity risk factors more closely. We believe there are two reasons for this new interest. One reason is to understand the nature and relative magnitude of the risks in their portfolio. This is a very sensible exercise because many actively managed portfolios have inapparent risk exposures. The other reason is that, with the growing acceptance of Smart Beta strategies, many investors are shifting their equity portfolios to capture specific long term risk premia. The commonly accepted equity risk factors are market beta (MKT – RF), value (HML), small size (SMB), momentum (MOM), and low volatility (BAB).6 Among the first four equity risk factors, over a period longer than 40 years, momentum registered the highest return and Sharpe ratio (see Figure 1).7

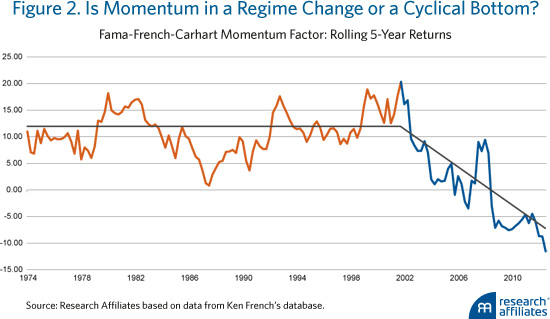

As attractive as momentum appears in Figure 1, it must be borne in mind that all equity risk factors are time-varying. That is, risk factor exposures will not add value consistently and all of the time. There will be some periods when certain risk factors are in favor and others when they are not—including extended intervals when factor-based investing is very discomfiting. As shown in Figure 2, the momentum risk factor has earned a negative risk premium for the 13 years ending June 30, 2013. We have also observed that momentum’s strength has eroded over the past decade. Factor-based investing requires strong conviction and a steady hand.

The other major challenges with momentum include higher volatility and the associated left-tail risk of severe performance crashes. These traits make it difficult to adopt momentum as an investment strategy and may explain why we don’t see many pure momentum strategies in the marketplace, where value strategies are ubiquitous. Although momentum and value factors have similar Sharpe ratios over time, momentum has 50% higher volatility, whereas value is more stable and, perhaps, more intuitively appealing.

Additionally, the momentum anomaly works best in illiquid, smaller cap stocks (Fama and French, 2011), and turnover is very high. Jegadeesh and Titman calculated turnover at 170% annually for their long/short portfolios. The trading costs are real and can substantially erode the risk premium due to momentum. Research is mixed about the alpha net of trading costs, but there is evidence that momentum’s high transaction costs offset the alpha potential at a fairly low level of assets invested in momentum strategies (Korajczyk and Sadka, 2004).8

Implementation Matters

A better form of momentum strategy can be implemented by adopting portfolio construction rules that adjust for systematic risk. Naïve momentum strategies hold high beta stocks that lead to crowding into expensive stocks during bubbles. When the inevitable market correction occurs, high momentum stocks reverse (that is, revert to the mean) strongly, and the high beta names naturally tend to overcorrect. One of our colleagues, Denis Chaves (2012), finds that the alpha produced by idiosyncratic momentum is significantly more robust than the alpha associated with traditional momentum. The Carhart four-factor model explains less than half of the return generated by an idiosyncratic momentum strategy.

Chaves corrects for beta in calculating momentum for the purpose of stock selection. For example, if the market rises 20% and a stock with a beta of 2.0 rises 40%, the idiosyncratic momentum of that stock is zero because the stock is expected to rise twice as much as the market. All else equal, this stock is unlikely to be selected for an idiosyncratic momentum portfolio, but it would probably be held in a traditional or naïve momentum portfolio. Intuitively, adjusting for beta allows us to differentiate between stocks whose prices are rising for “authentic” reasons, and those that are just moving with the market.9

Apart from the equity market factor, the value factor is probably the best documented and most commonly targeted source of risk premium. Nonetheless, it is not entirely clear what value is. Some theorists refer to an unknown or hidden risk (e.g., default). We have a different view. We maintain that the value premium (and the size premium as well) is a byproduct of noisy, mean-reverting stock prices, and it can be captured through contra-trading.10 In the RAFI® Fundamental Index® methodology, contra-trading is accomplished by means of systematic rebalancing to constituent weights that are not related to prices. Rebalancing, in this approach, does not merely correct for style drift; it is integral to the strategy. We favor annual rebalancing because it minimizes turnover and, therefore, transaction costs. Value investing is a long-term proposition.

Momentum strategies, in contrast, are profitable in the short run, and they call for more frequent rebalancing.11 But, obviously, more frequent rebalancing entails higher transaction costs. In addition, rebalancing a non-price-weighted portfolio has a strong positive value factor loading and a negative loading to momentum. These opposing characteristics are hardly surprising; momentum and value strategies are themselves opposites—procyclical vs. contrarian, short-term vs. long-term, and based upon trending vs. reverting to the mean. Recognizing these oppositions, I submit that complementing a long-term fundamentals-weighted strategy with a judicious commitment to a short-term momentum strategy might, in aggregate, produce attractive risk-adjusted returns. Indeed, Morningstar found a blended portfolio of value and momentum outperformed a blended portfolio of value and growth by nearly 1% annually.12

And Yet…

So what are investors to do with momentum? Our conclusion is that momentum is inadvisable as a stand-alone strategy due to the risk of precipitous losses. Rather, we suggest that long-term investors seeking to tap more than one source of equity premium choose another, more stable factor for their core investment strategy (value is certainly a strong candidate), and consider adding momentum as a short-term trading strategy when market conditions are favorable.

Endnotes

1. For the record, the opinions expressed in this piece of writing are the author’s; they do not necessarily reflect Research Affiliates’ views.

2. See, for example, Rouwenhorst (1998), Griffin, Ji, and Martin (2005), Rouwenhorst (1999), Moskowitz and Grinblatt (1999), Carhart (1997), and Asness, Moskowitz, and Pedersen (2009).

3. For a fee on the order of 2 + 20%, CTAs will gladly provide you with the momentum returns across assets.

4. Kahneman devotes a very readable chapter to anchoring in Kahneman (2011).

5. Soffer and Walther (2000); Chordia and Shivakumar (2002).

6. Beta, value, size, and momentum constitute the classic “four-factor” Fama–French–Carhart risk model.

7. The risk factor portfolios are courtesy of Ken French at Dartmouth. Risk factor returns are calculated for zero-cost long/short portfolios. Momentum is calculated by taking the returns of all stocks from 12 months ago to 2 months ago, ranking them and selecting the top returning 30% of stocks for the long portfolio and shorting the worst 30% performing stocks.

8. The authors estimated that, for a single fund, momentum loses its statistical significance at $1–2 billion, and its profits at $5 billion.

9. Of course, traditional momentum portfolios have alpha beyond the beta risk factor, but idiosyncratic momentum dampens volatility, resulting in a more attractive risk premium.

10. If the stock market is not perfectly efficient for any reason, half of stocks are overpriced and half are underpriced. As market participants seek fair value, prices mean revert resulting in a return that has been shown to be approximately 2% over the capitalization-weighted index in developed markets such as the United States (Arnott, Hsu, and Moore, 2005).

11. Vayanos and Woolley (2013) determined that the Sharpe ratio of the momentum strategy is a function of the length of the window over which past returns are calculated, and they found that the highest Sharpe ratio was achieved using a window of four months. This implies a rebalancing frequency of three times per year.

12. Beginning in 1993 through June 2013, an equal-weighted Russell 1000 Value Index and AQR Momentum Index returned 9.53% relative to an equal-weighted Russell 1000 Value Index and Russell 1000 Growth Index that returned 8.63%. They had similar standard deviations of 15.4% (Bryan, 2013).

References

Arnott, Robert D., Jason C. Hsu, and Philip Moore. 2005. “Fundamental Indexation.” Financial Analysts Journal,vol. 61, no. 2 (March/April):83–99.

Asness, Clifford S., Tobias J. Moskowitz, and Lasse Heje Pedersen. 2010. “Value and Momentum Everywhere.” American Finance Association 2010 Atlanta Meetings Paper.

Bryan, Alex. 2013. “Does Momentum Investing Work?” Morningstar (April 10).

Carhart, Mark M. 1997. “On Persistence in Mutual Fund Performance.” Journal of Finance, vol. 52, no. 1 (March):57–82.

Chaves, Denis. 2012. “Eureka! A Momentum Strategy that Also Works in Japan.” Research Affiliates Working Paper (January 9).

Chordia, Tarun, and Lakshmanan Shivakumar. 2002. “Momentum, Business Cycle, and Time-Varying Expected Returns.” Journal of Finance, vol. 57, no. 2 (April):985–1019.

Fama, Eugene F., and Kenneth R. French. 2011. “Size, Value, and Momentum in International Stock Returns.” Fama–Miller Working Paper; Tuck School of Business Working Paper No. 2011-85; Chicago Booth Research Paper No. 11-10.

Griffin, John M., Xiuqing Ji, and J. Spencer Martin. 2005. “Global Momentum Strategies: A Portfolio Perspective.”Journal of Portfolio Management, vol. 31 no. 2 (Winter):23–39.

Hong, Harrison, and Jeremy C. Stein. 1999. “A Unified Theory of Underreaction, Momentum Trading, and Overreaction in Asset Markets.” Journal of Finance, vol. 54, no. 6 (December):2143–2184.

Jegadeesh, Narasimhan, and Sheridan Titman. 1993. “Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency.” Journal of Finance, vol. 48, no. 1 (March):65–91.

Kahneman, Daniel. 2011. Thinking, Fast and Slow. New York: Farrar, Strauss, and Giroux.

Kahneman, Daniel, and Amos Tversky. 1979. “Prospect Theory: An Analysis of Decision Under Risk.”Econometrica, vol. 47, no. 2 (March):263–292.

Keynes, John Maynard. 1936. The General Theory of Employment, Interest and Money. London: Macmillan Cambridge University Press.

Korajczyk, Robert A., and Ronnie Sadka. 2004. “Are Momentum Profits Robust to Trading Costs?” Journal of Finance, vol. 59, no. 3 (June):1039–1082.

Moskowitz, Tobias J., and Mark Grinblatt. 1999. “Do Industries Explain Momentum?” Journal of Finance, vol. 54, no. 4 (August):1249–1290.

Rouwenhorst, K. Geert. 1998. “International Momentum Strategies.” Journal of Finance, vol. 53, no. 1 (February):267–284.

———.1999. “Local Return Factors and Turnover in Emerging Stock Markets.” Journal of Finance, vol. 54, no. 4 (August):1439–1464.

Soffer, Leonard C., and Beverly R. Walther. 2000. “Returns Momentum, Returns Reversals, and Earnings Surprises.” Working Paper (January).

Vayanos, Dimitri, and Paul Woolley. 2013. “An Institutional Theory of Momentum and Reversal.” Review of Financial Studies, vol. 26 no. 5 (May):1087–1145.