The debt dragon: Credit habit proves hard for China to kick

August 27, 2013 Leave a comment

Last updated: August 26, 2013 7:54 pm

The debt dragon: Credit habit proves hard for China to kick

By Simon Rabinovitch in Guiyang

The Chinese government says its debt problem is under control, but the people of Pianpo village have cause to disagree. Over the past year they have seen their water cut off, rubbish pile up in the streets and their wages go unpaid as debt has mounted. An elevated motorway soars over the villagers’ concrete homes, meant to connect them to central Guiyang, one of China’s fastest-growing cities. Instead, the slip road to Pianpo ends in a patch of gravel. The state-owned company building the road took on too much debt and could not pay its construction workers. Water pipes were dismantled when the roadworks began but were never repaired when cash ran short. A couple of times a day, Chen Xiuxiang, 75, trudges up a hill to fetch his weight in water – 120 pounds – from a working tap, carrying two buckets on a wooden pole across his shoulders. Most of his neighbours do the same. “They keep promising they’ll fix things but they never do,” says Mr Chen.For most of its past 30 years of growth averaging 10.5 per cent, China did not rely on credit. But it has become ever more reliant on debt since the global financial crisis, drawing on banks, bonds and an array of lightly regulated institutions to keep its economy roaring.

This debt dependency has put China at a dangerous crossroads. If the government is serious about containing financial risks, growth may slow sharply as it weans the country off debt, burdening the global economy. Yet that prospect is less frightening than the alternative. If the government loses its nerve, the debt bubble will continue to expand, raising the spectre of economic turmoil.

“Risks over China’s financial stability have grown. Credit has grown significantly faster than gross domestic product,” Fitch Ratings gave warning this year when it cut China’s sovereign rating, the first such downgrade by a big international agency since 1999.

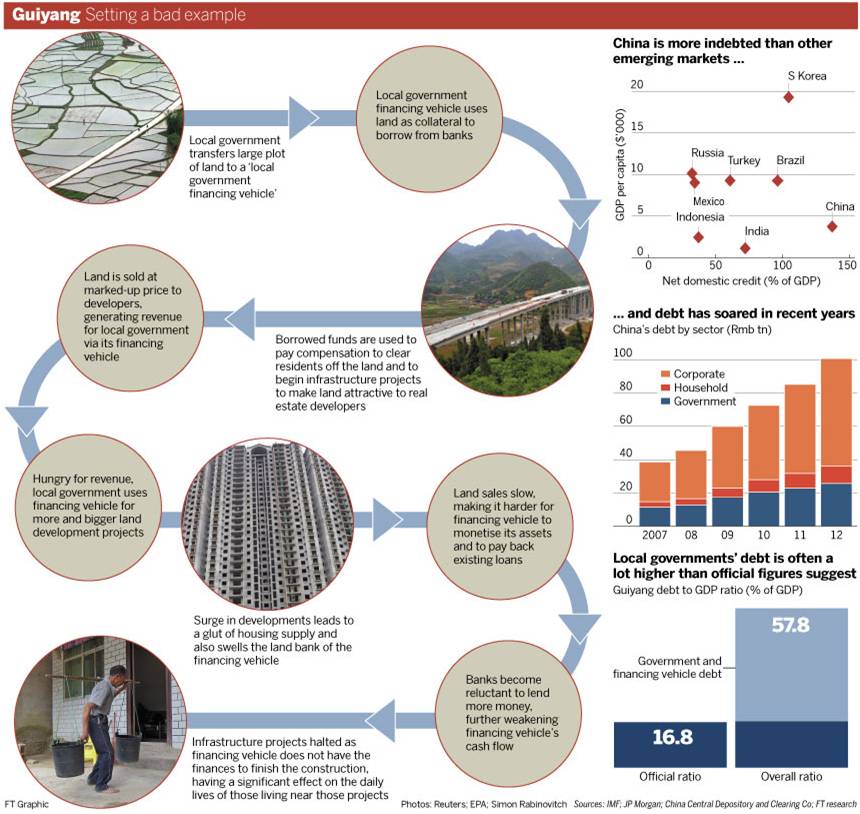

Total debt in China – government, corporate and household – has shot up from 130 per cent of gross domestic product in 2008 to nearly 200 per cent today, or more than Rmb100tn ($16.3tn), according to Chinese central bank data. Such a rapid increase in borrowing has historically led to crises in countries from Argentina to South Korea.

The trail of debt in China starts on the desks of ambitious government officials, especially at the municipal level. Capital of the southwestern province of Guizhou, Guiyang is one of China’s poorer cities, but it has boomed in recent years – and it is a prime example of its debt-fuelled economic model. “We need to struggle for GDP,” Yuan Zhou, Guiyang’s then mayor, thundered in a radio interview in 2011. “Only with higher GDP will people’s lives be improved.”

To stimulate growth, local officials deployed a simple technique, one replicated throughout the country. The government appropriated rural land on the cheap from farmers, sold it to property developers at a mark-up, and the developers in turn built dense clusters of tower blocks.

“The government is the engine and the market gives it a push,” is the slogan at an urban planning hall, where a diorama of the Guiyang of the future looks like Manhattan on steroids.

Guiyang’s growth has relied on a constant ratcheting up of investment. To keep the local economy growing at 15 per cent a year, the government has needed real estate companies to buy ever more land and build ever more homes.

One of the city’s first big developments was Century Town, completed in 2010 and designed for 40,000 people. Soon after came Future Ark, planned to accommodate 170,000 residents. Cranes are now erecting towers for Garden City, which will be large enough for 350,000 people – more than one in 10 of Guiyang’s residents.

Garden City will have 31 bus lines, 10 shopping centres and eight schools. Its showroom, which sits just beyond a fake lake festooned with plastic dinosaurs, has been buzzing with prospective homebuyers this summer. But the property developments that preceded it offer cautionary tales.

Zheng Wei, a salesman at Century City, says that its rows upon rows of identical grey flats are only half occupied. Many of the shop spaces at its base are shut, a thick film of dust coating their windows. “Because there are so few people here, no businesses dare open,” he says.

Future Ark has plastered Guiyang in advertisements – motorway hoardings, glossy leaflets, signs on taxis and jingles on the radio. “Buyers used to chase us. Now we chase them,” a saleswoman says.

The slowdown in housing sales is not just a problem for the developers. It has also started to expose the extent to which government debt has underpinned the property frenzy.

Because there are so few people here, no businesses dare open

– Zheng Wei, Century City salesman

Officially, Guiyang’s debt load is tiny, just 17 per cent of its municipal GDP. Yet any accurate tally has to look beyond the official figures to what are known as “local government financing vehicles”.

By law, China’s local governments are not allowed to fall into debt – they cannot borrow from banks or issue bonds. But there is a loophole. Cities, towns and villages can create financing vehicles at arm’s length. Owned by local governments but incorporated as companies, they have a free hand to borrow cash.

And borrow they have, playing a crucial role in the transfer of government-owned land to property companies. The financing vehicles raise the funds needed to resettle displaced farmers, build roads and dig sewers, making the land attractive to investors.

In Guiyang, there are at least five official financing vehicles, all established since 2008. If their liabilities are added up, the city’s debt ratio last year would have tripled to 58 per cent of GDP. It’s a similar picture across China: analysts think government debts run anywhere from 40 to 80 per cent of GDP, up at least twofold since the start of the financial crisis.

The biggest of Guiyang’s financing vehicles is the City Construction and Investment Group, the company that was responsible for building the half-finished motorway through Pianpo.

For a company so central to Guiyang’s development, it is very discreet. Its listed address does not exist. With help, it can eventually be tracked down to a four-floor villa in a quiet residential neighbourhood, identified only by a small doorplate. Guiyang City Investment, as it is known, declined to comment for this article, saying it was too busy.

Disclosure requirements have forced it to be more forthcoming when issuing bonds. It has explained that it is the “main body” for financing Guiyang’s infrastructure development. Those bond documents also reveal that its debt-to-asset ratio fell to 51.2 per cent this year from 73 per cent in 2010. If all was well, this decline would indicate a reduction in leverage. But what it actually reflects is an increase in its asset holdings – that is, land – and in the value ascribed to that land. Its assets nearly doubled from Rmb35bn in 2010 to Rmb64bn this year.

And those assets have not fared so well of late. With the property market coming off the boil, Guiyang City Investment has not sold enough land to real estate developers meet its financial commitments. “Its ability to service its debt is continually declining,” says Dagong, a Chinese rating agency. So vast are its land holdings that Dagong estimates it would take 28 years to sell them.

Late last year the worries about debt stopped being hypothetical for Guiyang City Investment. Regulators deemed it unable to make interest payments in full and China Development Bank, a large lender, refused to advance it any more money, according to a local government notice.

The motorway through Pianpo was one casualty. Unpaid construction workers went on strike. “We blockaded the motorway with trucks until we got what was owed us,” says Wen Zhang, a burly driver.

The residents of Pianpo did not have the same influence. First, they lost their running water. Then the government stopped paying sanitation workers, leaving rubbish to pile up on the streets. Determined to complete the motorway, Guiyang City Investment went back to China Development Bank to negotiate financing.

When enough land was posted as collateral, the bank relented, though only in part. It lent Rmb1bn – half of what had been requested. The money was enough to pave the road through Pianpo but not to finish the sliproad or connect the water pipes.