China companies feel the investment hangover

August 28, 2013 Leave a comment

Last updated: August 27, 2013 5:10 pm

China companies feel the investment hangover

By Simon Rabinovitch in Qujing

Wooden carvings of two elephants and an eagle, meant to symbolise wisdom and prosperity, flank the entrance to the Chinese chemical producer Yunwei. Today, they suggest a very different interpretation: a lumbering debt load and scavengers picking over the company’s scraps. “Lots of Chinese companies rushed to expand, to be the biggest in the world. This was a source of great pride. Now we see it as a headache,” says a soft-spoken Yunwei executive, back from a business trip where he was trying to sell more of the hard black coking coal piled high in the company’s storage facility in Qujing in the southwestern province of Yunnan.The Shanghai-listed company never quite cracked the top tier of the chemical industry in China, let alone the world, but it was not for a lack of trying. It increased its assets 30-fold over the past decade in a spree of investment, building an ethyl acetate factory, a calcium carbide production line, a coal distillation plant and lots more.

The problem is that its rivals did the same thing.

As the Chinese economy has slowed, demand for chemicals has dropped and laid bare Yunwei’s excesses. It lost Rmb1.2bn ($196m) last year, at times using just two-thirds of its production capacity. It has avoided large-scale lay-offs but only by enforcing a system of extended, unpaid holidays. Borrowing cash to stay afloat, its debt-to-asset ratio has tripled from 10 years ago to 90 per cent today, making it one of the country’s 100 most debt-laden companies, according to Chinese data provider Wind.

It is a trajectory of rising indebtedness that has been repeated across the chemical industry. Companies had been mistaken in their optimism about the Chinese economy, says Ren Jianxin, general manager of ChemChina, the country’s biggest chemical producer.

And this is just the tip of corporate China’s debt woes. Chemicals are a crucial feedstock for everything from steel to paint and plastic to textiles, so the distress of chemical companies reflects financial troubles spreading throughout China.

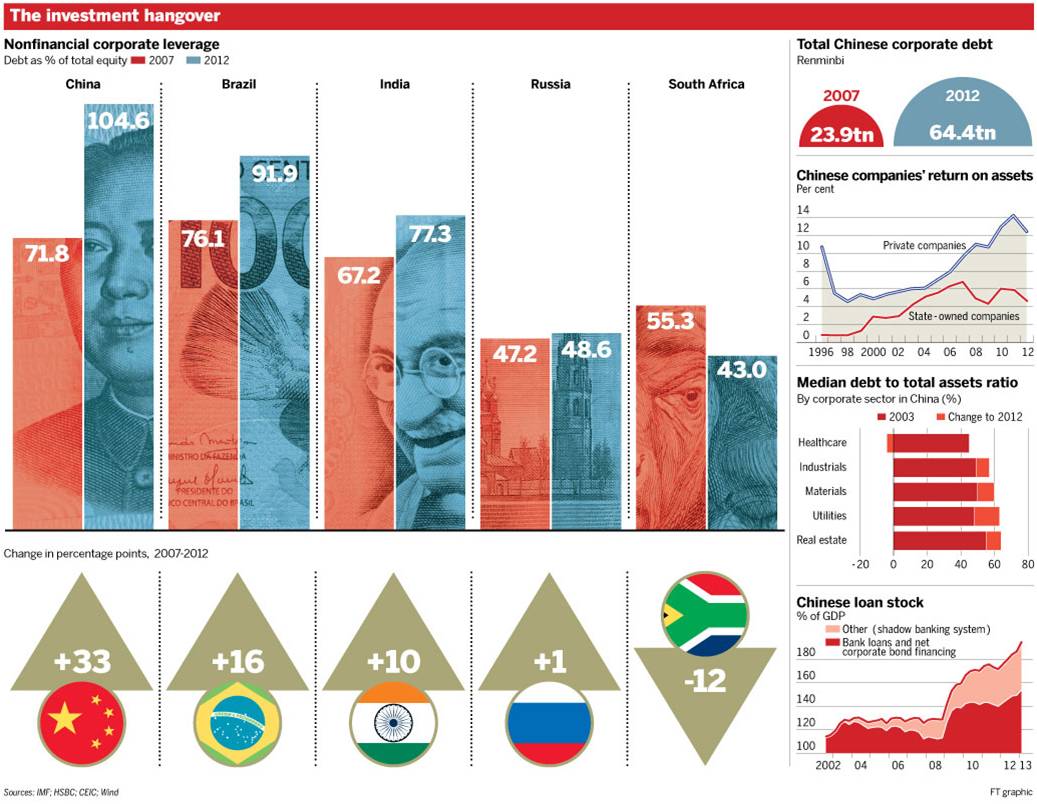

The rise in Chinese government debt levels has gathered more attention in recent years, but the increase in corporate debt has been even bigger. Themoney owed by Chinese companies shot up from 90 per cent of gross domestic product in 2007 to 124 per cent of GDP, or Rmb64tn, at the end of last year, according to JPMorgan.

The International Monetary Fund calculates that the average debt-to-equity ratio of Chinese companies increased to nearly 110 per cent last year, making China’s corporate sector more highly leveraged than those of all other big emerging markets. Corporate Brazil’s debt-to-equity ratio was less than 100 per cent, India’s was closer to 80 per cent and Russia’s was 60 per cent.

The stimulus unleashed by Beijing to counter the global financial crisis was seen as the salvation of companies at the time, but many now blame it for the increase in debt and excess capacity. “It was unavoidable. We were dragged into it by the government,” says the Yunwei executive, who spoke on the condition of anonymity.

The race to invest and get bigger took on a momentum of its own. Too much steel was being made, but so long as too many factories and homes were also being built, there was an artificially inflated market for it. The result has been a steady build-up of leverage that is eroding the strength of corporate balance sheets, says the International Monetary Fund.

Debt is widespread and it is hard to avoid. Fang Peiwen runs a car parts company on the outskirts of Shanghai, his office permeated by the smell of grease and the screech of metal cutters. His business is too small to be able to borrow from China’s banks, which favour bigger, typically state-owned enterprises. But over the past two years, the debt on his books swelled in a form unusually popular in China.

His clients, some of the biggest Chinese carmakers, began paying him less and less cash. Instead, they gave him bankers’ acceptances – a promissory note guaranteed by a bank and redeemable for cash at maturity, usually in about six months. Mr Fang says the acceptances account for two-thirds of the payment his company receives.

And that means he does not have enough cash on hand to pay his suppliers, unless of course they too are willing to accept IOUs in lieu of money. “Some companies refuse bankers’ acceptances and insist on cash. I’m too small; I have no choice,” he says, shrugging.

His accountant flashed one acceptance note, worth a little more than Rmb1m. It originated from a car company in Jilin in the northeast and had already been used as payment twice – each time, a different company had stamped its official seal on it – before it wound up in Mr Fang’s hands. For China as a whole, these bankers’ acceptances were just 3 per cent of GDP in 2008; they rose to more than 11 per cent last year.

The government is trying to contain the risks. It long ago ordered banks to stop lending to sectors with excess capacity, but ‘shadow banks’ such as trust companies filled the gap; regulators have recently made it harder for them to access financing. Beijing has also started to crack down on the issuance of bankers’ acceptances and lenders have signed off on far fewer of these since May.

The combined effect of these tightening measures has been a rising cost in financing. That is forcing companies across sectors ranging from sports apparel to heavy industry to reduce their debt loads, often by downsizing their operations.

With the steady stream of bailouts, what is nominally classified as corporate debt very quickly becomes government debt. This allows China to avoid the pain of defaults, but the debt remains in the system, just in a slightly different guise

The executive at Yunwei, the chemical producer, says local banks have demanded it pay interest rates as high as 8 per cent, or about 30 per cent above the benchmark level. It is a tough new reality. “We used to get our loans at benchmark because the creditworthiness of listed state-owned companies was seen as very good,” he says.

In July, Yunwei announced it hoped to raise Rmb870m by selling a set of its facilities. Some of the assets it put on sale had been built just a few years earlier, when cash was easy and optimism abounded. “Of course, we knew that the economy had cycles, that there would be declines and troughs. But when times were good, I can’t say we expected that it would get this bad,” says the executive.

As things deteriorate, Yunwei at least has a cushion to fall back on. Its parent company is owned by the Yunnan provincial government and officials in China have shown repeatedly that they are extremely reluctant to see their local champions fail.Rongsheng, shipbuilder, Shandong Helon, textile maker, and Suntech, solar panel producer, are three high-profile cases of companies that have received crucial government support since the start of last year.

Yet this does not solve the problem. With the steady stream of bailouts, what is nominally classified as corporate debt very quickly becomes government debt. This allows China to avoid the pain of defaults, but the debt remains in the system, just in a slightly different guise.

A Chinese executive with a big international chemicals company says the day of reckoning is not far off. “Winter is approaching. You can still take your coat off and pretend it’s warm, but actually it is beginning to bite.”