Post-Ballmer, Microsoft Must Focus on Products to Avoid Extinction

August 30, 2013 Leave a comment

Post-Ballmer, Microsoft Must Focus on Products to Avoid Extinction

By Peter Burrows, Ashlee Vance, and Dina Bass August 29, 2013

Whip out the elegant, light, superthin Asus (2357:TT) Zenbook on an airplane, and you’re sure to attract stares. The PC stands out even more with Microsoft’s (MSFT) Windows 8 software, its touchscreen full of colorful tiles promising a glimpse of the future. But that view starts to get foggy when Windows 8 tries to work with Microsoft Office 2013, lagging or freezing up as it attempts a task as ambitious as saving a document. This divide—between how good Microsoft’s products look and how badly they still behave—partly led to Chief Executive Officer Steve Ballmer’s Aug. 23 announcement that he’ll leave within a year.Ballmer will hand his successor Windows 8, the Windows Phone mobile operating system, and the forthcoming Xbox One video game console. These are good and often beautiful products. Really. The not-so-small task for Ballmer’s replacement will be to turn those innovations into something more: easy, fun, useful products that don’t disappoint.

In the immediate aftermath of the announcement, critics were quick to dish out the standard suggestions to fix Microsoft: bring in someone like former IBM (IBM) CEO Sam Palmisano, jettison the money-losing consumer operations, and focus on corporate software and services. These are reasonable strategies that would look good in the short term. But Microsoft would still have to sell products that don’t quite stack up against the more polished offerings from Apple (AAPL), Google (GOOG), and other rivals.

Ballmer has already done some of the hard work. In July he led the company through a massive reorganization that vaporized traditional business units (Windows, Office) to get everyone working together on products. Top executives will now oversee technology areas such as devices, software, and services. “They lost some good people, but the reorg broke up long-standing political fiefdoms,” says Jeffrey Sonnenfeld, a professor of management at Yale University. “Now they’re organized the right way for someone to come in and make it work.” Microsoft has also overhauled most of its major product lines in the past year. Its next CEO will inherit a business that, while slumping, still produces enough profit to make any executive drool.

To avoid blowing this once-in-a-lifetime opportunity, Ballmer’s successor must first acknowledge that the current lifeblood of those profits—customers who feel locked into Microsoft’s consumer and business products—won’t last much longer. There’s no reason consumers have to buy Microsoft’s products anymore when they can head to Apple, Google, or cloud country, or just squeeze more years out of their old PCs. Few companies buy smartphones and tablets for employees as they do for PCs, so Microsoft will have to earn every point of market share in these booming markets the hard way, by making stuff that’s way ahead of the competition. That means modeling itself to some extent on Apple, which, despite its recent stock slump, remains the finest product shop in tech.

Lesson No. 2: Learn to say no. A lot. Microsoft will never have only five product lines like Apple, given its huge swath of businesses ranging from keyboards to obscure data center software. Still, the company needs to pare down its menagerie of brands—SkyDrive and Live.com probably don’t ring a bell—to push a couple that consumers can remember, if not rally around. Microsoft’s Skype (MSFT) boasts around 300 million users and engenders the kind of loyalty most of its products lack. Longtime tech investor Roger McNamee, a co-founder of private equity firm Elevation Partners, wrote in an e-mail that Microsoft should elevate Skype over Windows as a fresh, vibrant brand, creating a central Skype browser and a range of Skype phones, including some for lower-income consumers in emerging markets. Nirm Shanbhag, managing director of consultancy Interbrand, says Microsoft needs a brand that extends beyond a product, “something representative of a larger platform.”

That would pave the way for an even more radical notion—packaging all of Microsoft’s consumer products in a single bundle, the way selling Word with Excel and PowerPoint was once revolutionary. The company has taken steps in this direction, offering some free Skype minutes with a yearly subscription to its online version of Office, but it ought to take bundling further. Why not use the strong Xbox brand to pitch college students on a package that includes an Xbox One, a smartphone, a Skype number, and a student version of Office? Such bundles could expose people to services that work well but haven’t found an audience, like Xbox Music, which offers song streaming and downloads. Subsidizing these deals would be expensive in the short term, but Microsoft needs to do something drastic to boost its mobile fortunes while it still has a mountain of cash ($77 billion).

To prosper on the merit of its products, Microsoft needs them to work together without freezing PCs with a click of the save button. As its next CEO, or at least that person’s right hand, the company needs a harsh, demanding product expert willing to ignore internal politics, focus group findings, or complaints about impossible deadlines. Such leaders (Steve Jobs, Mark Zuckerberg, Marissa Mayer) are rare; Microsoft arguably hasn’t had a world-class one since Bill Gates in his mid-’80s prime. But only a boss who insists that products be great the first time around can squelch the dread that has long accompanied a new Microsoft release.

Finding that person requires Microsoft’s board to resist the temptation to bring in one of the usual suspects, an experienced general manager such as Palmisano or Oracle (ORCL) Co-President Mark Hurd. While such able managers could hone Microsoft’s financials, the company needs a development-focused executive at the helm to address its fundamental problems. “We’re in the era of the product person rising to the top,” says Martha Josephson, a recruiter with headhunter Egon Zehnder. “The best sales executive in the world cannot solve a lack of product vision.”

Almost as important is a fresh face. Sure, Gates has morphed from tech’s Dr. Evil to St. Bill, and Ballmer has poured billions into new businesses in an attempt to keep the former monopoly from sliding into irrelevance. But Microsoft needs someone who can persuade people to give it one more chance.

The bottom line: Microsoft’s next CEO should spend big to boost its products and give the company a fresh start.

August 29, 2013 7:48 pm

Technology: Microsoft’s outlook

By Richard Waters

Steve Ballmer’s decision to step down raises questions about whether the software group can get its groove back

The news of Steve Ballmer’s early departure as chief executive of Microsoft has created a vacancy for one of the plum jobs in business: a seat at the helm of a corporate behemoth worth nearly $300bn that remains among the most profitable companies in the world.

It has also triggered a wave of speculation about where Microsoft will go from here. When the effusive Mr Ballmer quits some time in the next year it will mark a definitive break with more than 30 years of technology history, a period in which he and close friend Bill Gates have shaped the company around the PC.

Signs that the exit was hurriedly arranged have added to the impression that Microsoft stands at a crossroads. Only weeks before, Mr Ballmer announced a sweeping reorganisation of the company that was meant to accelerate its faltering transition to the post-PC world, while putting himself more clearly at the centre.

His successor stands to be remembered either as the saviour who breathed fresh life into a fading company or as the person who was unable to reverse a decline that had already set in.

“Every 10 years there’s a big technology company we think is stagnant and going out of business – and they turn around and become dominant again,” says George Colony, chief executive of tech research firm Forrester.

The list of tech turnrounds has included Intel in the 1980s, IBM in the 1990s and Apple in the 2000s. This decade is the turn of Microsoft, predicts Mr Colony, who is among those to argue that the company is well positioned to fight back.

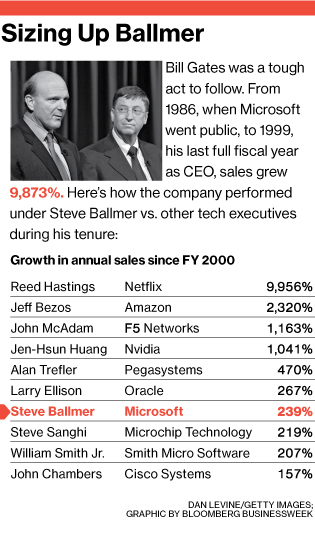

Mr Ballmer will certainly leave his successor with some powerful weapons. Thanks to its abiding PC operating system monopoly, the company has tightened its grip on the market for PC software with its Office suite of productivity tools, while extending its reach to servers and other important areas of business IT systems. Revenues have soared from $23bn in 2000, the year that he took over, to hit $78bn this year.

But this has not been enough to appease Wall Street, or silence the persistent question that has dogged Mr Ballmer’s final years: as the PC era that the company dominated passes, can Microsoft make the transition to the new world of mobile devices and services?

A central question for the company’s next boss will be how to establish an earlier foothold in the next hot technology markets, rather than ceding them to rivals – as has happened in areas such as internet search, smartphones and social networking. But releasing Microsoft’s inner innovator will be challenging as long as the entire organisation remains beholden to the old profit centres that have underpinned its fortunes.

“It’s very frustrating if you’re trying to get into a new business and you’re protecting your cash cows like Windows and Office,” says Arne Josefsberg, a former Microsoft general manager who was involved in the development of Windows Azure, the attempt to build a new “cloud” based operating system. In new technology markets, he adds, “you can’t be in it halfway.”

The next head of Microsoft will not be given carte blanche when they start. Mr Ballmer’s attempt to reposition the company around mobile devices and services has had the full backing of the board, even if the CEO himself is on the way out. Yet, as the new head of a technology giant in transition, she or he will still face big decisions: how to refocus the company’s efforts, where to channel extra investment or pull back, and how to tap more effectively into the deep pool of talent and intellectual property that still makes Microsoft one of the most feared competitors in the tech world.

Those questions suggest a number of options. The company’s preferred route is not likely to be limited to any one direction: big acquisitions and divestitures may both follow, even as Microsoft commits itself to stricter financial discipline that involves returning more of its cash to shareholders.

Rediscovering the inner innovator: The big break-up

The US Department of Justice pushed for a break-up of Microsoft more than a decade ago but was later overruled by the George W Bush administration. Some observers argue that it is a shame the trustbusters did not prevail: it might have ended up being the best thing that happened to Microsoft.

According to this view, the company has had too much cash at its disposal and too many options to focus clearly on any one route. Mr Ballmer has been too ready to place multiple bets without being committed to any individual course, says Michael Cusumano, a professor at Massachusetts Institute of Technology who has followed the company closely for a number of years. How could one company fight on so many fronts?

By contrast, the turnrounds at Apple and IBM only came about after those companies were forced by necessity to make clear bets on a narrower range of businesses with the potential to lead a revival.

Carving off businesses such as internet search and video gaming, where Microsoft makes little money, might be a good place to start. But why stop there?

The Office suite of applications has suffered from being joined at the hip with Windows, according to the company’s critics. To stimulate more demand for tablets running Windows, Microsoft has postponed releasing an Office app for Apple’s iPad or tablets based on Google’s Android operating system. That has reduced the visibility of Office on an important new computing platform. But it has not helped sales of Microsoft’s Surface tablet either, to judge from the $900m writedown taken on that operation.

Broken up into different companies, Microsoft’s core businesses would be freer to pursue their own strategic goals. These nimble “Baby Bills” could focus on infrastructure software and platforms such as the Windows operating system; business applications such as Office; and consumer devices and internet services.

Those who argue against a break-up point out that it would run counter to a powerful trend in technology: the emergence of mobile ecosystems that combine devices, software and internet services, putting a premium on tight integration between a wider range of technologies. Microsoft, though well behind, is the company best positioned to challenge Apple and Google, says Mr Colony – but only if it remains a single company.

The cultural revolution

With $10bn in research and development spending a year, Microsoft is among the very few tech companies left with an extensive and ambitious research programme.

So why, runs the frequent Wall Street lament, does it not have more to show for it? From tablet computing to online maps, Microsoft has been a pioneer in promising new tech markets. But it has not been the one to capitalise on them first.

Former Microsoft executives complain of insurmountable cultural and business hurdles. Big-company blues have played a part, with too many layers of approvals to get through before a new idea can get full support within the organisation.

Even Mr Ballmer has expressed regrets about not having backed enough promising new business ideas because they did not seem to have the potential to become significant businesses.

“These kinds of things get squelched, they get killed,” says Mr Josefsberg, former general manager for Azure, the software vital to Microsoft extending its operating system business into the era of cloud computing.

Inter-divisional rivalry with the more established Windows group led to tensions, threatening the upstart business – a pattern that has played out many times over the years as promising new ideas have been forced to play a supporting role to the PC operating system division.

In the case of Azure, a new product that was considered strategically essential, Microsoft overcame the tensions by setting the new business up in a separate location and insulating it from the rest of its operations.

The approach paid off, with Azure finally gaining momentum after a slow start.

Mr Ballmer’s attempt to restructure Microsoft – a task that the company says will take years – is one response to this problem. By scrapping divisional boundaries, it would create a centralised organisation that would leave Microsoft looking far more like Apple.

Whether that is enough to unblock the creative wellsprings of the company under its next CEO is another matter. The next boss will still face a problem that bedevils all giant corporations: how to get in early enough on new ideas that will not make a material impact in financial terms for years but will eventually come to represent the tech markets of the future?

The cash machine

At $23bn, Microsoft’s free cash flow in its most recent fiscal year is double what Google produces – and Microsoft is not spending money on long shots such as driverless cars and “smart” glasses.

It also has more than $77bn in the bank.

“Even though they make a bit less every year, they’re still a moneymaking machine – and will probably be very healthy for the next five to 10 years,” says MIT’s Prof Cusumano.

Microsoft has showered its cash on shareholders before, appeasing Wall Street with a record-breaking $32bn special dividend in 2004.

More recently, though, Mr Ballmer has become a hoarder, leaving Wall Street increasingly restless over the mountain of money that has been building up.

Little wonder then that Wall Street has been hankering after a big payday. Following Apple’s lead from earlier this year and borrowing massively to buy back stock – followed by a clearer commitment to return excess cash to shareholders in the future – might do wonders for Microsoft’s stock price.

It might well push the shares back above $40 for the first time since the dotcom crash of 2000, according to Rick Sherlund, a software analyst at Nomura.

A change in business strategy would underpin this commitment to a more predictable distribution of excess cash. Ending its expensive bets on consumer technology – even the Xbox games console, widely seen as a success, may not have made a positive return in its 12-year life – would let Microsoft tie its fortunes directly to the more stable business IT market, where it has become a powerful force under Mr Ballmer.

It was a similar argument to this that persuaded investor Warren Buffett, the chairman and CEO of Berkshire Hathaway, to overcome his unease about the fleeting fortunes of tech companies with an investment in IBM. That came only after Big Blue had demonstrated the highly predictable operating and financial profile of a blue-chip.

Such a move, however, would fly in the face of another trend in technology: consumerisation, which has put individual users in the driving seat when it comes to choosing technology, often including the devices and applications they use at work.

It would also rob Microsoft of a potentially important strategic position, being able to span both the work and personal lives of its users.

The Hail Mary

Microsoft has taken more than a decade to turn the Xbox into its only undisputed hit consumer product. Its attempt to become a force on the consumer internet, first with the MSN internet portal and later with search, has taken far longer and soaked up billions of dollars.

How much more effective it would be, then, to use the company’s sizeable rainy-day fund to buy businesses that would provide a foothold in the new devices and services markets where Microsoft wants to make an impact.

Mr Ballmer had the right idea, according to this view, offering more than $40bn in a failed bid for Yahoo in 2008. But why blow so much cash on a company whose glory days lie more than a decade in the past? Rather than wasting time on the Zunes, Kins and Bings, which failed to make Microsoft a leader in music players, smartphones and search, respectively, would it not be easier to buy off the shelf?

In hardware devices, there is plenty of lost ground to make up. Google and Apple both sell smartphones, tablets and laptop computers, while Amazon is making inroads with its Kindle.

Fortunately, acquisitions here would be cheap. There is Nokia, of course, a company whose fortunes have become inextricably tied to Microsoft, as it has become the sole handset maker to bet its entire future on Windows software. The tight integration of Nokia and Microsoft technology has produced some well-regarded products, even if sales have not taken off.

For a play in PCs there is still time to make a bid for Dell, whose disgruntled shareholders would jump at anything worth more than the buyout offer from Michael Dell, the founder. That would also bring a bonus of a wider array of hardware and services in the business technology markets.

For good measure, the next Microsoft CEO could consider topping off the acquisition list with Sony (a deal that would bring entertainment to feed its growing array of hardware devices and online channels, leapfrogging Apple and Google) and Twitter. Current cash reserves exceed the combined market value of all of those companies, although acquisition premiums would push up the price.

To succeed in the acquisition department, the next head would certainly need to bring new skills to the company. One of its biggest deals, the $6bn purchase of aQuantive, an online advertising company, resulted in a write-off of nearly the entire purchase price, while Mr Ballmer fumbled and failed in what should have been a knockout bid for Yahoo.