The Brazilian Billionaire Who Controls Your Beer, Your Condiments, and Your Whopper

August 30, 2013 Leave a comment

The Brazilian Billionaire Who Controls Your Beer, Your Condiments, and Your Whopper

By Alex Cuadros August 29, 2013

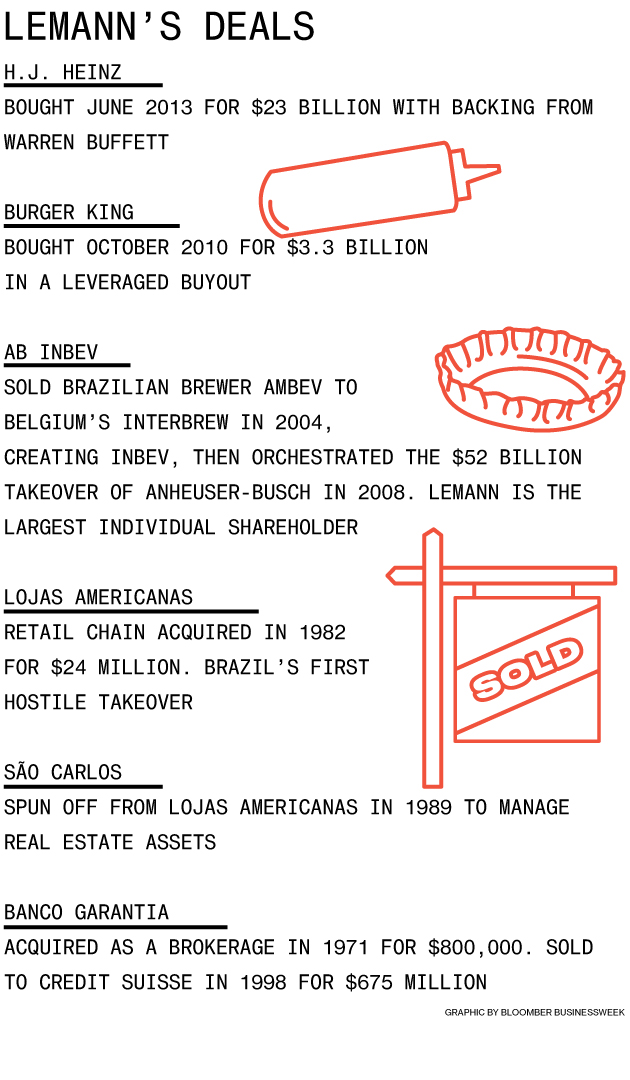

After they sold H.J. Heinz to Warren Buffett and a bunch of Brazilians in June, the ketchup manufacturer’s outgoing board of directors met for dinner at Pittsburgh’s Duquesne Club to congratulate themselves on a job well done. Twenty-three billion dollars had just changed hands. The takeover price, at $72.50 a share, was almost 20 percent higher than the company’s recent all-time high. “We said we’re all going to miss each other, but we felt we had done right by the shareholders,” says Dean O’Hare, who’d sat on the board since 2000. Heinz is an institution in Pittsburgh—the Steelers play at Heinz Field, locals of means like to get married at Heinz Memorial Chapel—and Buffett’s presence allayed fears that the 144-year-old company would be dismantled. “Seeing the name on the letter was very important to us,” O’Hare says.

The only really un-Buffettlike aspect of the deal, other than the high price, was the Brazilians. Not because of their nationality, but because they were the principals at 3G Capital, an investment firm best known for the leveraged buyout of Burger King in 2010. Had the Oracle of Omaha changed his mind on private equity, which he once compared to a porn shop? At Berkshire Hathaway’s (BRK/A) annual shareholders’ meeting in May, Buffett explained why he seemed to be breaking his own rules: his confidence in 3G’s 74-year-old chief investor and strategist, Jorge Paulo Lemann. He called Lemann “classy.” As a sign of Buffett’s esteem, 3G and Berkshire have equal stakes in Heinz despite Berkshire putting up three times as much cash. Heinz, Buffett said, would be Lemann’s show.

In the U.S., Lemann is virtually unknown, even though he and his two longtime partners, Marcel Herrmann Telles and Carlos Alberto Sicupira, now control three icons of U.S. consumer culture: Heinz ketchup, Burger King, and, after the $52 billion takeover of Anheuser-Busch in 2008, Budweiser beer. The combined market value of the companies they run is $187 billion—larger than that of Citigroup (C).

In Brazil, Lemann is a business-class hero. He’s the wiry, white-haired conglomerateur who’s part Buffett, part Sam Walton, part Roger Federer. (In his younger days he was a five-time Brazilian national tennis champion.) “Lemann” is shorthand for pitiless efficiency. Last year he became the richest man in Brazil, taking the title from oil and mining tycoon Eike Batista, whose empire has since collapsed. Worth some $20 billion, Lemann is No. 32 on the Bloomberg Billionaires Index, seven slots behind George Soros and three ahead of Carl Icahn. Arminio Fraga, who worked under Lemann in the 1980s, later served as central bank chief, and now runs one of the country’s largest asset-management firms, is one of a generation of Brazilian entrepreneurs who look up to Lemann. “He carried out a revolution in the way people think about business,” Fraga says.

Lemann and his partners founded 3G in New York in 2004 to buy U.S. companies with the cash they’d earned from more than two decades of takeovers and turnarounds in Brazil. The name is a reference to the number of principals in the firm (the Brazilian press often calls Lemann, Telles, and Sicupira the three musketeers) and to Banco Garantia, the investment bank where they developed their management philosophy. Starting in the 1970s, Lemann built Garantia into Brazil’s premier financial firm. Since selling the bank to Credit Suisse (CS) in 1998, he and his partners have focused on acquisitions outside the financial industry, such as Heinz.

Lemann declined to be interviewed for this article. When contacted by Bloomberg Businessweek, some of his friends and business associates said they’d been asked by Lemann not to speak with journalists about him. Heinz likewise declined to make its executives available for comment, though a handful of press releases since June 7, when the company’s shares ceased trading and Heinz officially went private, hint at the sort of shake-ups that Lemann and his partners specialize in.

Their first move was to replace Heinz’s long-serving chief executive officer, William Johnson, with Bernardo Hees, a former Brazilian railroad executive who had most recently run Burger King (BKW). In August, Hees fired 600 members of Heinz’s office staff in the U.S. and Canada, or 9 percent of its North American workforce. About 350 of those jobs were in Pittsburgh. Then he started knocking down the walls between offices to create an open-air plan and promote communication. He also axed 11 senior executives and replaced them with top performers from inside the company. Much of this resembles the changes Lemann’s people made at Burger King, where it’s forbidden to make color copies without permission, and Anheuser, where employees no longer have access to free beer. According to a book published in Brazil this year, Sonho Grande (Big Dream), Lemann’s partner Sicupira has a favorite phrase: “Costs are like fingernails: You have to cut them constantly.”

The formula has done wonders for the profitability of Anheuser-Busch InBev (BUD), the company created by Anheuser’s 2008 merger with InBev; its stock price has increased about 150 percent in the past five years. Burger King is already valued at more than twice the $3.3 billion the three musketeers bought it for in 2010.

Burger King had languished for eight years under the ownership of the private equity firms Goldman Sachs Capital Partners, TPG Capital, and Bain Capital. In two years under Hees the company more than doubled its margins, as measured by Ebitda (earnings before interest, taxes, depreciation, and amortization), Wall Street’s preferred gauge of cash flow. He did this in part by recasting Burger King as an owner of franchises rather than an operator of restaurants and sold off locations owned by the company. This allowed Hees to shove about 28,000 employees off Burger King’s balance sheet. It also meant the company didn’t need to spend as much to refurbish aging restaurants; instead, it offered incentives and lined up loans for franchisees to revamp their locations, replacing dull old plastic countertops with shiny metallic surfaces and futuristic stripes of neon. Seeking to draw in a wider crowd, Hees scrapped an advertising strategy that catered to young males and got rid of that creepy bearded mascot, the King. And he expanded abroad, forming joint ventures in emerging markets including Brazil, where local partners put up most if not all of the cash.

Hees didn’t know anything about fast food before becoming CEO of Burger King. He started his career as a logistics analyst at a Brazilian railroad Lemann and his partners took over in the 1990s, rising to CEO after just seven years. Putting a railroad guy in charge of a fast-food chain makes no sense at first blush, but this, too, is a typical Lemann move. “What’s important is not knowing hamburgers, it’s knowing how to lead a company,” says Paulo Veras, an Internet entrepreneur who for several years led one of the trio’s foundations. “It’s the kind of intelligence that transcends any specific business segment.”

Lemann was born and raised in Rio de Janeiro. The surname is Swiss—his father, a dairy entrepreneur, was born in Switzerland, as were his maternal grandparents. Lemann went to the American School of Rio de Janeiro, where he was voted most likely to succeed, even though he spent much of his time surfing and playing tennis. He played at Wimbledon and competed in the Davis Cup twice—once for Brazil and once for Switzerland (he has dual citizenship). In 1958 he was accepted by Harvard University at a time when few Brazilians went; as he explained in a 2011 speech to a group of high school students in São Paulo, he probably got in because of his tennis game.

In the speech, Lemann said he didn’t like Harvard. He hated the cold and missed the waves of Leblon beach in Rio. So he designed a system to get his bachelor’s degree in just three years: Before signing up for a class he gathered information on the syllabus by interviewing the professor and students who’d already taken it. He also discovered that the final exams from previous years were archived at the library and noted that they varied little from year to year, allowing for easy cramming. Harvard was mainly worthwhile, he said, because it forced him to get creative so he could finish early.

One day, when he was in Rio on summer vacation from Harvard, a powerful storm had created waves more than 30 feet tall that broke perilously late, right on the beach. Used to 10-foot waves, he decided to go for it anyway. “I took the wave and felt the blood go to my feet. It was a lot faster than I was used to, and a lot taller, but I went for it, and I managed to get out before it crashed. My adrenaline was at the maximum,” he told the Brazilian high school students, a broad smile across his wrinkled face. At key moments in his career, “I thought back to that wave I surfed in Copacabana far more than I thought about the things I learned in college. It gave me a certain self-confidence when it came to taking risks.”

After graduating in 1961, Lemann juggled a tennis career with a series of jobs in Brazil’s fledgling financial industry. In 1971 he joined with a few other traders to take over an inconsequential brokerage known as Garantia. Luiz Cezar Fernandes, one of those original traders, says Lemann instituted the partnership model of Goldman Sachs (GS), with a twist. Instead of simply awarding shares once a year for a job well done the way Goldman did, Lemann offered the best performers the chance to use their bonus to buy shares. Because they offered lower salaries than the competition, this meant that becoming a partner was a risk. “You had to give up buying a house, a car,” says Fernandes. As Garantia grew, it also meant that becoming a partner would make you very rich on paper. Seniority didn’t matter: To reward top-performing newcomers, the bank would shrink the bonus pool for laggards.

Lemann always made a point of personally hiring employees, whom he considered potential partners. In the past, Brazil’s best jobs were in the local offices of multinational corporations, but by the 1980s, Garantia had become one of the most sought-after employers for smart young men. (There are few women in Lemann’s world, even today.) Résumés didn’t matter much. Candidates had to go through a gauntlet of interviews with 8 or 10 partners who had an acronym for the profile they were looking for: PSD, for poor, smart, deep desire to get rich. Sometimes the partners posed odd or even offensive questions just to throw interviewees off balance and see how they reacted. Paulo Lerner, who worked at Garantia in the early ’90s, remembers being asked whether he had sex with his girlfriend. He wasn’t too fazed, and he made it through, one of a handful among the hundreds who applied each year.

Garantia was a place where the words fanático and obsessivo were considered compliments. The first person to go home for the day often received ironic applause. “No one came and handed anything to you on a platter,” says Lerner. “A lot of people couldn’t handle it.”

The Garantia style was personified by Sicupira, who joined in 1973. At 17 he had emancipated himself from his parents and founded a brokerage, selling it the following year. He first met Lemann because they are both avid spearfishermen—Sicupira once caught a 301.2-kilo (664-pound) blue marlin, which set a world record. In 1982, Sicupira led Garantia’s first major foray outside finance, the acquisition of an ailing retail chain known as Lojas Americanas, or American Stores. It was the first hostile takeover in Brazil, where stratospheric interest rates and the general chumminess of business had long kept such moves in check.

Sicupira knew little about retail. He was, however, well aware of a Lemann maxim, one of 20 laid out in a document distributed to Garantia executives: “Innovations that create value are useful, but copying what works well is more practical.” So Sicupira wrote letters to the CEOs of the world’s largest retailers, asking if he could pay them a visit to learn about their business. One responded personally: Sam Walton, founder of Wal-Mart Stores (WMT).

Lemann and Sicupira visited Walton in Arkansas and saw firsthand how the American billionaire squeezed suppliers, controlled inventories, and paid obsessive attention to cost. They also saw how he leveled with employees and customers. Walton’s philosophy worked for Wal-Mart, so Sicupira copied it. Much as Walton promised his executives he would dance the hula on Wall Street if Wal-Mart reached a certain mark of profitability—and followed through—Sicupira, upon achieving a 6 percent Ebitda margin at Lojas Americanas, did the samba in carnaval dress in downtown Rio.

Sicupira also incorporated some of the Garantia culture, lowering executives’ base salaries, cutting perks, and implementing big, target-based stock incentives. Lojas Americanas’ top management mutinied, calling for the return of the cushy old system. After the executives made their demands—and went out for lunch—Sicupira fired them and locked them out of the building. Sicupira, Telles, and Lemann still own Lojas Americanas. Its share price has increased tenfold in the past decade.

Lemann once told Brazil’s HSM Management magazine how he’d visited Konosuke Matsushita, the founder of Panasonic, a few years before his death in 1989. “Suddenly he starts telling me about his plans for the next 500 years of his company, as if that were normal,” Lemann said. This was at a time when hyperinflation kept most Brazilians from planning for the future at all. Lemann also considered General Electric’s (GE) annual reports a kind of bible and adopted Jack Welch’s 20-70-10 rule—promote the top 20 percent of your employees, maintain the middle 70, and fire the rest. Claudio Galeazzi, a management consultant who led Lojas Americanas in the late 1990s, compares Lemann and his partners to sponges. “They weren’t ashamed to copy the best examples of management,” he says. “Then they made it better, applying their own ink.”

The seed for what would become AB InBev was Brahma, a Brazilian beer manufacturer that Lemann acquired in 1989, putting Telles in charge. They hired a management consultant named Vicente Falconi, who put in place a system where, instead of basing budgets on the previous year’s, managers started at zero every 12 months and had to make a case for why they should get more. Hees used the same system at Burger King. “People say the customer comes first and all that,” says Falconi, who still advises Lemann’s companies, “but actually it’s cash.”

Through it all, Lemann kept up his tennis. Even while overseeing Garantia, Lojas Americanas, Brahma, and, starting in 1993, a buyout firm called GP Investimentos, Lemann played almost every morning at 6:30 a.m. The adrenaline eventually took its toll. Although obsessed with fitness and healthy eating, he suffered a heart attack in 1994, at 54. For perhaps the first time in his life, he was forced to slow down.

At the time, Garantia was at its peak. Margaret Thatcher had recently paid a visit, signaling its clout. It was a pioneer in Brazil for making risky bets of the sort favored by U.S. investment banks, and in 1994, according to Sonho Grande, it cleared $1 billion in profit. Its traders got cocky. Without properly hedging itself, Garantia sold huge amounts of insurance on Brazilian government bonds, and when the Asian financial crisis exploded in 1997, sending interest rates soaring in emerging markets around the world, the bank lost hundreds of millions of dollars in a single year. It was the bank’s first loss in two decades, and its aura of invincibility was ruined. The next year, Lemann and his partners sold it to Credit Suisse for $675 million, a fraction of the price they might have gotten before the losses.

Then life got worse for Lemann. In 1999 criminals attempted to kidnap his three young children. A driver was taking them to school when two cars blocked the street. The would-be kidnappers opened fire. Although the driver was wounded, he managed to get the children to safety. Lemann would soon move his family to Switzerland, but on the day of the shooting his children did not miss school. Nor did Lemann himself miss any meetings, according to Sonho Grande and a former associate who asked not to be named. To his business partners, the only sign something was amiss was that he arrived late.

The sale of Garantia was a blow to Lemann, but it left him with cash to invest, so he started buying shares in Gillette(PG), the razor manufacturer, and won a seat on the board. This is where he met Buffett, who had invested $600 million in the company in 1989. They had similar boardroom styles, says James Kilts, Gillette’s chairman and CEO from 2001 to 2005. He praises Lemann’s intellectual curiosity and nimbleness in an industry where he had no expertise. Once, in a debate over the wisdom of buying the largest battery manufacturer in China, Lemann prevailed on his fellow board members by saying the strategic value of the acquisition outweighed concerns over price. Kilts says the bet ultimately paid off. “He had this ability to step back from a situation and capture the essence,” Kilts says. “He’s a great listener, not a big talker.”

At his own companies, Lemann’s single-minded focus on cash flow explains how, after the takeover of Anheuser-Busch in 2008, AB InBev had little trouble paying down its massive debt amid the global financial crisis. It could also explain why consumers in the U.S. have lately taken to suing the company for allegedly watering down its Budweiser. People who know Lemann say he personally avoids the products he now peddles; he’s a teetotaler who prefers a bottle of water and a salad. According to Sonho Grande, he ate his first Burger King hamburger only after acquiring the company and commented that he found it too big. What he liked about Burger King was how it generated cash.

Veras, the Web entrepreneur, says Lemann and Sicupira have a saying: “Any organization, to be successful, must grow.” Once they’ve streamlined away a company’s inefficiencies and there’s nothing left to improve, however, the only way to keep growing is through acquisitions. “It’s essential to keep this immense machine operating and renewing itself,” says Thomaz Wood Jr., a management professor at São Paulo’s Fundação Getúlio Vargas business school. It’s a heady but vicious work environment; Wood says he wouldn’t recommend his students take jobs at Lemann’s companies.

AB InBev is the world’s largest brewer. It sells almost one in every five beers consumed on earth. Those huge economies of scale allow it to return more value to shareholders, but Wood suggests the benefits have mostly accrued to Lemann, Telles, and Sicupira’s bank accounts. This is more than an abstract discussion. In 2009 the three men paid 15 million reais ($6.4 million) to Brazil’s securities regulator to settle allegations that they had abused their control of AmBev, the product of their merger of Brahma with another Brazilian beer company. The regulator, known as CVM, said they had used stock options to boost their holdings in AmBev’s voting shares before selling it to Belgium’s Interbrew in 2004, to the detriment of minority investors. None of the three admitted wrongdoing as part of the settlement.

Heinz is different from Lemann’s past acquisitions in that there’s less fat to trim. This has a lot to do with billionaire investor Nelson Peltz. His firm, Trian Fund Management, bought a 5 percent stake in 2006 and helped usher in aggressive cost savings and asset sales, allowing for more marketing spending as well as higher dividends and share buybacks. Analysts credit him for the rally in the share price in the years before Lemann and Buffett acquired the company. How, then, to wring more value from Heinz? Peter Rossman, a spokesman for the IUF, an international association of unions in the food industry, says Heinz workers are nervous, though its factory jobs have so far gone untouched.

If AB InBev is any indication, Lemann didn’t buy Heinz just to downsize it. O’Hare, the longtime Heinz board member, says 3G relayed the message that it plans to use the company as a platform for acquisitions. Fernandes, the onetime partner at Garantia, says he’d bet money that Lemann will try to take over PepsiCo (PEP). (A spokesperson from PepsiCo declined to comment.)

Lemann once told a Brazilian tennis magazine he decided to pursue business only after he realized he was unlikely to be one of the world’s 10 best tennis players. He said, “I saw that I would never be an astro”—a star. People who know him say he hates seeing his name on rich lists, but it seems more an aversion to publicity than an aversion to riches. He’s an empire builder. “People in the U.S. are moved by the American dream,” says Fernandes. “Jorge Paulo, as soon as he fulfills one dream, he’s on to the next.”