Too big to hail: China’s banking behemoths are too beholden to the state. It is time to set finance free

September 1, 2013 Leave a comment

Too big to hail: China’s banking behemoths are too beholden to the state. It is time to set finance free

Aug 31st 2013 |From the print edition

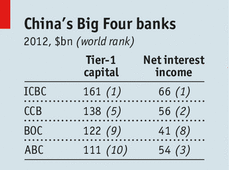

AT FIRST sight, China seems to have a superb banking system. Its state-controlled banks, among the biggest and most profitable in the world, have negligible levels of non-performing loans and are well capitalised. That appears to suggest that the country’s approach should be applauded. Not so. For one thing, though China’s banking system is stable, its banks are not as healthy as they seem. The credit binge of recent years has left them with far higher levels of risky loans than they acknowledge. And a profit squeeze is coming. The banks are having to work harder to keep both their biggest depositors, who are tempted by alternative investment products, and their biggest borrowers, who are turning to the bond market instead. As a consequence, the country’s Big Four banks—Industrial and Commercial Bank of China, Bank of China, Agricultural Bank of China and China Construction Bank—will no longer make easy money by merely issuing soft loans to state-owned enterprises, or SOEs (see article).What is more, that vaunted stability has come at a high price. China’s policy of financial repression, which forces households to endure artificially low interest rates on bank deposits so that subsidised capital can be lent to SOEs, is a cruel tax on ordinary people. The size of China’s banks may seem impressive, but in fact it is a sign that the economy is excessively reliant on bank lending. And the incentives encouraging the risk-averse Big Four, whose bosses are leading figures in the Communist Party, to funnel lending to cronies at inefficient SOEs have starved dynamic “bamboo capitalists” of credit.

Excess of caution

China’s new leaders have acknowledged that the old approach has led to excesses, notably overcapacity in state industries. They are talking of allowing more private (but not foreign) investment in the financial sector and are urging banks to lend more to private firms. That is not enough.

For a start, China should end financial repression. If deposit rates were gradually freed, banks would be forced to compete with each other for depositors and free to win back customers now lost to the shadow banking system. Most Chinese banks have no clue today about customer service, risk management or credit assessment. That would have to change. Miserable returns on bank deposits encourage punters to plough money into real estate and other riskier investments, so paying decent deposit rates might help prick the property bubble, too.

Second, China needs to go beyond banking. In many developed economies, non-bank firms and financial markets vie with banks to issue credit, but in the Middle Kingdom banks still dominate. In recent years Chinese firms raised nine times as much money from banks as they did on the country’s stock exchanges. The corporate bond market has grown quickly of late (and big banks no longer gobble up most of the offerings). This growth should be encouraged.

Third, China must separate banking from crony state capitalism. The best way to do this is privatisation. Smaller banks like China Merchants and China Minsheng, in which private investors have significant stakes, lend much more energetically to small businesses and households than do the state-controlled goliaths. Privatising the Big Four would help, though it would make it harder for the state to manage any future banking crisis. And as long as sheltered, oligopolistic SOEs exist, banks will lend disproportionately to them because they enjoy implicit state backing. So the big SOEs must themselves face greater market discipline.

Finally, China should welcome competition, from abroad and at home. Two Chinese internet giants, Tencent and Alibaba, are starting to provide wealth management, investment funds and other financial services. Banks are lobbying against them. Regulators worry about the destabilising effect of start-ups with new business models, but for newcomers that do not pose a systemic risk they can afford lighter-touch regulation.

None of these changes should happen overnight. They can be implemented gradually. But a bit of disruptive innovation would be good for China’s stodgy banks, and its people.