Five Years Later, Fannie Mae, Freddie Mac Remain Unfinished Business; Fixing the Mortgage Giants Remains the Largest Single Piece of Unfinished Business From the Financial Crisis

September 7, 2013 Leave a comment

September 6, 2013, 8:04 p.m. ET

Five Years Later, Fannie Mae, Freddie Mac Remain Unfinished Business

Fixing the Mortgage Giants Remains the Largest Single Piece of Unfinished Business From the Financial Crisis

WASHINGTON—Of all the temporary patches the U.S. government slapped onto the sinking financial system in September 2008—from pumping money into banks to rescuing insurer American International Group Inc. AIG -1.01% —none was more urgent to then-Treasury Secretary Henry Paulson than saving mortgage giants Fannie Mae FNMA +0.81% and Freddie Mac FMCC -0.88% .“It was the single most important thing we did to prevent disaster—real disaster,” said Mr. Paulson in a recent interview. But five years later, he adds, “it didn’t occur to me that we’d be here with nothing done.”

Fannie and Freddie remain the largest single piece of unfinished business from the financial crisis. As record profits have replaced huge losses, some now question whether cosmetic changes could substitute for the more radical overhaul of the companies envisioned five years ago.

The profits are even giving Fannie, the bigger of the two, some of its old swagger. In an online video touting the company’s profit streak, Fannie boasts that it will “change the way people experience housing for generations to come.” Fannie had around 7,200 employees at the end of February, up from around 5,800 when it was bailed out.

The Obama administration, congressional leaders and the financial industry all insist that Fannie and Freddie must change. But figuring out exactly how to reshape or replace them is proving harder than most anyone imagined.

“Everyone wants to get rid of Fannie and Freddie,” said Frank Sorrentino, chief executive at the $1 billion-asset ConnectOne Bank, a community bank in Englewood Cliffs, N.J. “But I don’t think this country has the political appetite to lose many of the things they enable.”

The biggest reason is that the firms play such a central role in the mortgage market, including access to the 30-year, fixed-rate mortgage. That product, which doesn’t exist in much of the world, is popular with Americans who enjoy stable payments even if interest rates rise.

The firms don’t make loans. They buy them from lenders and package them into bonds. That middleman role created deep markets for mortgage securities by matching banks with investors willing to manage the risks of holding long-term, fixed-rate mortgages.

Fannie and Freddie got into trouble because they took on more risk over the past two decades while using their political clout to beat back attempts to force them to hold more capital. They amassed huge investment portfolios to profit from the difference between their lower cost of capital—a benefit of an implied federal guarantee because Congress created the firms—and the rates they could earn on mortgages.

The companies experimented with loosening lending standards in the late 1990s. But in the early 2000s, Wall Street firms raced ahead of them by packaging larger quantities of riskier loans that often weren’t eligible for backing by Fannie and Freddie. By 2005, Fannie and Freddie were losing market share. They began loosening their own loan standards to compete, taking on more risks at what would later prove to be the worst possible time. As the housing bust deepened in 2008, lawmakers called on the firms to take on more risks to help the market.

By August 2008, Treasury officials concluded the firms didn’t have enough capital and feared what would happen if investors lost confidence in Fannie and Freddie. A failed debt auction by the companies might trigger fire-sales of bond investors world-wide. “It just would have been catastrophic,” said Mr. Paulson. “We were racing against the clock here.”

On Friday, Sept. 5, 2008, he summoned the companies’ chief executives to separate afternoon meetings and told them they were being taken over. Fannie’s board considered its options, including a court battle, but quickly concluded there weren’t any good ones. “Defending the company when the federal government had declared war on it did not seem like a prudent course,” said Daniel Mudd, Fannie’s chief executive, in a recent interview. Two days later, the firms had been effectively nationalized, and Mr. Mudd was replaced.

The Obama administration remained conflicted over the mortgage giants. In a 2011 meeting with the president, then-White House economist Austan Goolsbee compared Fannie and Freddie with comic-book villains that had been captured and imprisoned in a cell on the ocean floor. It would be folly, he said, to turn the companies loose because they promised to behave.

“If Fannie and Freddie are allowed to return to their old business model, then shame on us as a nation,” said Mr. Goolsbee, who left the administration in 2011, in a recent interview.

The government has plowed $188 billion into Fannie and Freddie. By the end of September, the companies will have sent $146 billion in dividends back to the Treasury with nearly two-thirds of those payments made this year. Many analysts forecast that within a year, the firms will have sent more to the Treasury than they borrowed.

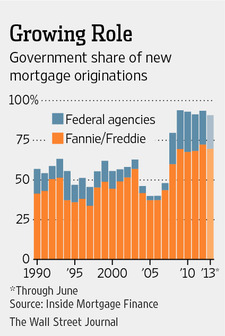

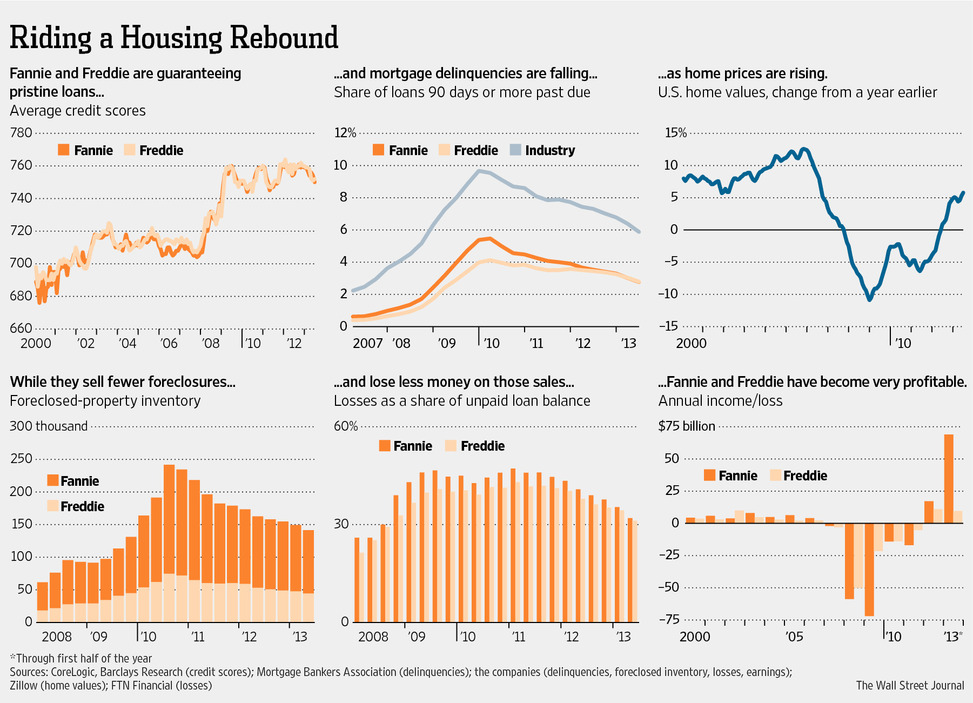

Fannie and Freddie are reporting banner profits thanks to rising home prices and falling mortgage delinquencies. They have boosted the fees they charge lenders while refusing to guarantee risky loans. Private investors have shied away from buying mortgages without federal backing, leaving Fannie, Freddie and other federal agencies responsible for insuring nearly 90% of all loans.

As the debate over the companies’ future comes to a head, policy makers’ views of the causes of the 2008 crisis have shaped their proposed solutions.

Some conservatives see Fannie and Freddie as the chief culprits of the bubble, saying that they pioneered risky lending standards at the urging of politicians who wanted to boost the homeownership rate. Rep. Jeb Hensarling, a Texas Republican who chairs the House Financial Services Committee, is moving forward a bill to wind down Fannie and Freddie over five years and cede their roles to the private sector.

Other lawmakers say Fannie and Freddie helped inflate the bubble but weren’t necessarily the worst offenders. In their view, the companies ran off the rails because as shareholder-owned firms, executives couldn’t resist the urge to buy riskier loans to grab extra profits even as the housing market overheated.

A Senate bill, introduced in June by Sens. Bob Corker (R., Tenn.) and Mark Warner (D., Va.) would replace Fannie and Freddie with federal reinsurance for mortgage-backed securities, much the way the Federal Deposit Insurance Corp. insures bank deposits. The goal is to restore private investors to the position of taking the first losses on mortgages but provide the guarantees that many believe are needed to preserve access—especially during downturns—to 30-year, fixed-rate loans.

President Barack Obama waded into the debate for the first time last month when he said that he supported the general aims of the Senate bill. The White House also is working behind the scenes with the Senate on a related proposal that could potentially use parts of a shuttered Fannie and Freddie to fashion new mortgage-guarantee entities, according to people familiar with the discussions.

Everyone is digging in for a protracted battle. At one end are home builders, real-estate agents, small lenders and consumer advocates who want to preserve the largest possible federal safety net. At the other end are free-market economists who believe housing receives too much government support. Loan guarantees, they say, put undue risk on taxpayers while diverting investment from other sectors of the economy.

Big banks generally fall somewhere in between. They have long viewed Fannie and Freddie as competitors, but they don’t want to lose access to a government guarantee that keeps markets functioning smoothly. Banks have profited handsomely over the past two years by collecting fees for refinancing loans that can be sold to Fannie and Freddie.

Some critics warn that the suggested replacements gloss over the private sector’s role in producing lots of shoddy mortgages. “All of the proposals we’re seeing have one thing in common: They would essentially give greater control over the market to the biggest banks that were key participants in the bubble,” said Joshua Rosner, managing director of research firm Graham Fisher & Co. and a longtime critic of Fannie and Freddie before their collapse.

Fannie Mae Chief Executive Timothy Mayopoulos is prodding Washington to make up its mind. He says he is concerned that continued calls for liquidating the company could send his best employees for the exits. They “have families to feed,” he said in a May speech to officials from the nation’s biggest banks.

After Fannie reported a $58.7 billion profit during the first quarter, in part from reversing certain write-downs it had taken after the bust, it launched the online “progress report” that touts its recent achievements, including charitable giving.

Compared to Freddie Mac, “the culture at Fannie has always been much more self-confident, much more ‘We’re going to survive this thing,’ ” says Robert Bostrom, former general counsel at Freddie Mac.

Mr. Mayopoulos didn’t endorse a particular outcome in his May speech. But he reminded the bankers that 30-year, fixed-rate mortgages weren’t a “naturally occurring phenomenon in financial markets.” And there was “limited evidence,” he said, that private capital was ready to return in large scale.

“We fully appreciate that Fannie Mae should play a smaller role in a properly functioning market,” he added, “and we are working to make that happen.”

While Fannie and Freddie aren’t permitted to lobby, allies have begun speaking up in their defense. Small banks worry that without the firms, they would have to sell more of their loans to megabanks like Wells Fargo & Co. that would turn around and sell other services such as checking accounts to those borrowers. “I would be handing my clients to them on a silver platter,” said Mr. Sorrentino of ConnectOne Bank.

Hedge funds and institutional investors that have bought Fannie and Freddie shares represent another unlikely ally. They say that rather than plowing the companies under, the government should instead place new curbs on their activities, subject them to higher capital requirements, and spin them off as private firms.

“It seems like the lawmakers are hellbent on waging this sort of Don Quixote kind of battle against demons that are no longer there,” said Michael Kao, chief executive of Akanthos Capital Management in Woodland Hills, Calif., which has invested in both companies since before their collapse.

All of the alternatives being proposed in Washington “simply won’t work,” says Bruce Berkowitz, chief investment officer of Miami-based Fairholme Capital Management, which sued the Treasury in July to challenge the terms of the government’s bailout. The lawsuit alleges that the Treasury is illegally expropriating the company’s profits. A Treasury Department spokesman said, “We fully believe our actions have been lawful and appropriate.”

To avoid consolidating more than $5 trillion in assets and liabilities onto the federal ledger, the government never took full control of Fannie and Freddie when it bailed them out. Instead, the U.S. agreed to inject vast sums of aid in exchange for a new class of stock—”senior preferred” shares—that paid a 10% dividend. The government also received warrants to acquire nearly 80% of the firms’ common stock.

The shares, considered worthless, were delisted from the New York Stock Exchange in 2010. But soon after, some investors concluded the firms would become profitable one day and began buying their shares at deep discounts. The government upended those bets last year when it amended the terms of its rescue.

The new agreement requires all of the firms’ earnings to be sent to the Treasury as dividends. Those payments don’t reduce the senior preferred shares held by the Treasury, however, and they prevent the firms from building capital. As a result, restoring them to private ownership requires Congress or the Treasury to change the bailout terms.

Hedge funds have taken to Capitol Hill to build support. In a June letter to Treasury Secretary Jacob Lew, Rep. Michael Capuano (D., Mass.) called the current bailout terms “outrageous usury” and introduced a bill that would relax them, making it more likely that Fannie and Freddie could one day exit government control.

But shareholders have found mostly an unreceptive audience. Taxpayers should be entitled to every penny of profit for so long as Fannie and Freddie are viable due solely to their government support, said Mr. Corker, the Tennessee Republican. His bill would leave little for shareholders.

“These entities are totally worthless from the standpoint of generating any kind of [income] without the federal government’s” backing, he said in July. “For the sake of the taxpayers, I hope that you do not win. But you have at it.”