It’s well known that September has been the worst month, on average, for stocks. But no one has come up with a plausible explanation for why that is.

September 7, 2013 Leave a comment

Updated September 6, 2013, 6:25 p.m. ET

How to Play the September Effect

It’s well known that September has been the worst month, on average, for stocks. But no one has come up with a plausible explanation for why that is.

MARK HULBERT

Stock-market aficionados know that the average September over the past 100 years has been terrible for stocks. But this record, in and of itself, isn’t a good reason to sell all your stocks and leave the money in cash this month. That is because there appears to be no convincing explanation for why equities have performed poorly in September. So there is a good chance September’s dismal historical record is just a random fluke that won’t persist.There is a broader investment lesson, too: Rarely do the myriad patterns that get Wall Street’s attention justify deviating from a simple strategy of buying and holding index funds.

The reason you should bet only on patterns whose existence makes theoretical sense goes back to Statistics 101: Correlation isn’t causation.

A good illustration comes from David Leinweber, founding director of the Center for Innovative Financial Technology at the University of California, Berkeley. Several years ago, while searching through economic data collected by the United Nations, he found that the indicator most highly correlated to the S&P 500 was butter production in Bangladesh.

No one would ever think of basing investment decisions on Bangladeshi butter output, of course. But without a good reason for why September has been bad for stocks, the same conclusion applies to the September phenomenon. As Mr. Leinweber said in an email: “There are too many meaningless correlations out there.”

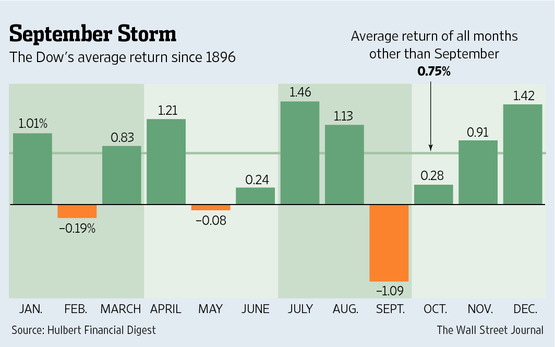

Meaningless though the September pattern appears to be, the month has been far and away the worst performer of the calendar. Since the Dow Jones Industrial Average was developed in 1896, it has lost an average of 1.09% in September—versus gaining an average of 0.75% in each of the other 11 months.

Of course, September is just one of a host of seasonal patterns that investors have observed over the years. Examples include the tendency of the stock market to perform well in late December and early January, and in the winter months between Halloween and May 1. Most of these patterns aren’t backed by sound theoretical explanations.

Many have searched for such a rationale in the case of September. One superficially plausible explanation is that it is caused by the large number of mutual funds whose fiscal years end in the fall—especially since 1990, because of a new tax law that took effect then.

Near the end of their fiscal year, mutual funds often will sell positions they hold at a loss in order to reduce the size of their capital-gains distributions.

There are at least two serious objections to this hypothesis. The first is that, since the 1990 tax-law change, September actually has lagged behind the other months by less than it did in previous decades. The second is that just 11% of U.S. stock-fund assets are invested in funds with fiscal years that end in September, according to Lipper.

By contrast, no less than 35% of assets are invested in funds with fiscal years ending in December, and yet it has been the second-best performer of the year, on average.

Another popular explanation for September’s poor record: a wave of selling by investors returning from their vacations. Ben Jacobsen, a finance professor at Massey University in New Zealand and an expert on the stock market’s seasonal patterns, isn’t convinced. In an email, he said that the evidence is mixed at best on whether investors are net sellers after taking vacations.

In fact, one study found that their tendency is to do the bulk of their selling before their vacations, not after.

Should investors continue searching for why September has a bad record? Lawrence Tint, the former U.S. CEO of Barclays Global Investors and currently chairman of Quantal International, a risk-management firm, says it is a waste of time. That isn’t just because he doubts that such an explanation will ever be found. It also is for a more basic reason, Mr. Tint argues.

“If a convincing explanation for the September effect were ever found, savvy investors would immediately begin jumping the gun by selling in August, others in turn would try to beat them, and the historical pattern would quickly disappear,” he says.

“Unless you or I are able to discover something nobody else knows about, by the time we know why a pattern exists it’s too late to profit from it,” he adds.

For most individuals, Mr. Tint’s advice means sticking with a broadly diversified stock-index fund. The low-cost choice among U.S. funds is the Vanguard Total MarketVTI +0.08% exchange-traded fund, which charges annual expenses of just 0.05%, or $5 per $10,000 invested.

If you don’t think you can stick with such a fund through a market decline, you should reduce your equity holdings now to whatever level you would be comfortable holding.

An inexpensive option for diversifying outside of the U.S. is the iShares Core MSCI Total International Stock IXUS +0.38% ETF, with an expense ratio of 0.16%. It reflects the returns of all publicly available stocks outside the U.S.

—Mark Hulbert is editor of the Hulbert Financial Digest, which is owned by MarketWatch/Dow Jones. Email: mark.hulbert@dowjones.com