America Faces the Shock of the Old; Future Economic Growth May Depend on Innovation

September 9, 2013 Leave a comment

September 8, 2013, 5:48 p.m. ET

America Faces the Shock of the Old

Future Economic Growth May Depend on Innovation

U.S. companies just haven’t been pushing boundaries like they used to. Innovation is the secret sauce of growth, enabling an economy to advance at a faster pace than the mere combination of investment and labor allows. A history of innovation encompassing the likes of the light bulb and the Internet is a big reason why the U.S. economy has been so much more robust over the long haul than others. But there is no guarantee that past will be prologue.Robert Gordon, an economist at Northwestern University, thinks innovation won’t be quick enough to save the U.S. economy from lackluster growth stemming from headwinds like an aging society and increasing inequality. He argues that even with the boost provided by personal computers and the Web in the late 1990s through the early part of the last decade, innovation since the 1970s hasn’t been as strong as in earlier decades when products like the internal combustion engine filtered through the economy.

Disagreeing with that assessment, MIT Sloan School of Management economists Erik Brynjolfsson and Andrew McAfee point to factors such as recent advances in artificial intelligence, saying the pace of innovation has in fact been accelerating. They say the productivity figures Mr. Gordon uses to bolster his point don’t capture the full story.

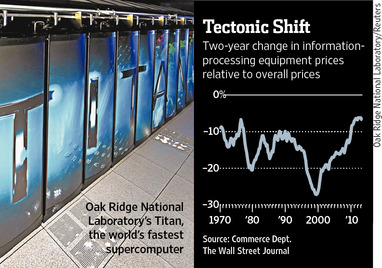

But a look at what is happening with technology prices suggests that, at least for now, Mr. Gordon may be on to something.

A hallmark of technology is that it constantly gets cheaper: Buying a computer equivalent to today’s $1,000 PC in 2005 would have cost much more. But prices for tech equipment and software purchased by U.S. companies haven’t been falling as quickly as in the past, notes J.P. Morgan Chase economist Mike Feroli.

Prices of information-processing equipment in the second quarter were down 6.8% from two years earlier, adjusting for the economy’s overall pace of inflation, according to Commerce Department data. In the 1990s, the average two-year decline was 17.7%. Software prices fell 3.4% over the same period, compared with an average decline of 9.5% in the 1990s.

The government quality-adjusts its price figures, so if a company is buying, say, a more advanced server for the same price it paid for a less powerful one five years ago, that registers as a price decline. So the slower rate of price deflation in recent years suggests that technology isn’t becoming obsolete as fast as it used to. The implication is that the pace of innovation is slowing.

Prices are far from a perfect measure of innovation. For example, GoogleGOOG +0.00% is a big user of R, a programming language for statistical computing. But as an open-source project, R’s price is zero, so it has no place in the statistics. Moreover, prices for technology capital goods don’t reflect the flowering in high-tech tinkering that has emerged in recent years. With hobbyists putting together autonomous blimps in their garages, it is tough to declare American inventiveness dead.

But U.S. companies’ demand for technology has slowed: Spending on it, minus depreciation, in the decade ended 2011 rose at its slowest pace since the 1940s. So the price signal still makes sense: If firms aren’t as willing to buy into innovation, there is less incentive to innovate.

Until that view changes, and more of the secret sauce is mixed up, the U.S. economy may not be able to expand as quickly as it used to. And since this ultimately powers sales and profits, the future for companies, and their investors, will be a little less bright.