China’s Credit Levels Echo U.S. Crisis; Quick Jump in Country’s Debt is Reminiscent of Previous Meltdowns

September 9, 2013 Leave a comment

September 8, 2013, 6:53 p.m. ET

China’s Credit Levels Echo U.S. Crisis

Quick Jump in Country’s Debt is Reminiscent of Previous Meltdowns

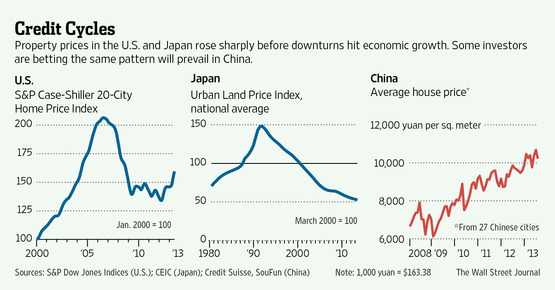

Investors have made billions betting against economies in which debt is rising and home prices are soaring. They have had particular success targeting the banks that fund these booms. Right now, their target is China. Some compare China to the U.S. in 2007. Others cite Japan before the 1989 real-estate bust. China bulls acknowledge the risks but say the government has the money and expertise to defuse the problems. Until recently, the bears were winning the tug-of-war, pushing down the prices of Chinese banks until they were the cheapest of any major economy based on price-to-book value, a measure for how investors rate the quality of a bank’s assets. But recently, the Chinese economy and markets have perked up. Chinese banks, reflected in the Hang Seng H Financial Index, have rallied 17% since July 3, even as they warned of rising bad debts and said they would likely have to raise capital.

With the U.S. housing bust fresh in their minds, critics see parallels. “The similarities to the U.S. are wanton use of the credit system to substitute for better sources of economic growth with a background of rising income inequality,” says George Magnus, a senior independent economic adviser to Swiss bank UBS AG, UBSN.VX -1.11% who has written extensively on financial crises. “These are all telltale signs of a country at a relatively advanced stage of financial instability.”

One key difference: “In the Western case, the official response was denial or complete ignorance,” says Mr. Magnus. In China, where the central government controls the economy and policy makers witnessed the U.S. bust, Beijing “will be able to respond in ways we [in the West] weren’t capable of. But it doesn’t mean it won’t be painless,” he says.

China’s corporate and household credit has risen quickly, from around 120% of gross domestic product in 2008 to more than 170% today, according to Bank for International Settlements data, which does not include debts owed by financial companies.

The U.S. in its credit boom rose from 143% in 2001 to 177% in 2008. Japan had a similar run up in the decade before 1989. Economists say quick jumps in debt—rather than absolute levels—are the determinants of future crises.

“I don’t know any country that’s seen such a large increase in debt and not gone on to have some form of crisis,” says Mark Williams, chief Asia economist for Capital Economics, an independent research house. He doesn’t think it is imminent in China, and the “crisis” could be years of slow growth, rather than a financial meltdown.

One key area of concern is China’s banks. As in the U.S., much of their loan growth in recent years has been off-balance-sheet. In China’s case, it has been wealth-management products and other devices that allowed banks to keep lending even despite regulators’ efforts to slow things down.

Much of this shadow-banking growth is being monitored by regulators. “The shadow-banking thing has been both known and blessed for a time,” says Jaspal Bindra, Asia chief executive for U.K.-based, emerging-markets-focused bank Standard Chartered. “Then I think they decided that people have taken it to a point where it’s been abused.”

In May, officials from the chief bank overseer, the China Banking Regulatory Commission, told Mr. Bindra that a substantial portion of the credit being generated in the economy this year was coming from the shadow-banking system, often arranged by banks but hidden from their balance sheets. The fear is that should the loans made through these wealth management products sour, regulators and investors will expect banks to take them back on their balance sheets, eroding their capital.

“They were very aware and very public. It wasn’t a whisper in my ear or a secret or something. They were probably telling everybody who visited them to make their point that they know what is happening,” he said.

The next month, in June, a credit crunch hit China’s banking system, reviving fears that the kind of credit market paralysis that hit the U.S. in 2008 and 2009 could wreak havoc on the financial system. The squeeze was engineered by the central bank to rein in what it saw as out-of-control credit growth driven by the country’s shadow-banking system. While the credit squeeze caused turmoil, it eased once the central bank let the cash flow again. It was also a sign regulators are aware of the problems in the system.

Another difference: America’s bubble originated in home mortgages. China’s house-buying frenzy has been financed mostly with cash. The big debt growth has been to developers, companies and local governments, some of whom have implicit backing from the state.

“The housing market isn’t going to be the big crash story,” says Diana Choyleva, head of macroeconomic research for Lombard Street Research.

Giving China some breathing room compared with other emerging markets, such as India or Brazil, is that it is a net saver as a nation. It has run current-account surpluses for years, meaning its own savings are enough to fund its rise in debt. So if its debts sour, it can afford to bail itself out.

“The difference I think is that the overleveraging, if at all in China, is all one pocket of the state,” says Mr. Bindra of Standard Chartered. All of China’s biggest banks are controlled by the central government.

That invites comparisons with Japan. The most obvious parallels are rising debt and real-estate prices coupled with a banking sector that is perceived as too cozy with its borrowers. When bad debts started rising, the Japanese government allowed banks to put off dealing with the problem, leaving them undercapitalized and unable to lend.

In Japan, “no systemic financial crisis occurred, but financial stress was hidden,” writes Haibin Zhu, J.P. Morgan’s chief China economist. Banks refinanced loans even though there was little prospect the beleaguered corporate borrowers would pay them off in the end. This led to “zombie companies and zombie banks” and little new investment in the economy.

He worries that without reforming the banking and corporate sector, China could put off a restructuring of debts needed to cleanse the economy. “The consequences could be more severe for China,” he says. “China is not as wealthy as Japan was and so would not be able to sustain as much stress.”

Japan’s economy has stagnated, but with little social upheaval or mass unemployment thanks to a strong social safety net. China might not be as well prepared.