Doubts Rise as China Touts Upturn; Beijing’s Reliance on Credit-Fueled Megaprojects, Exports Raises Questions About Rebound’s Length

September 13, 2013 Leave a comment

Updated September 12, 2013, 7:08 p.m. ET

Doubts Rise as China Touts Upturn

Beijing’s Reliance on Credit-Fueled Megaprojects, Exports Raises Questions About Rebound’s Length

BOB DAVIS, TOM ORLIK and LAURIE BURKITT

BEIJING—China’s leaders are trumpeting their commitment to overhauls, but there are signs a recent turnaround in the Chinese economy relies on old policies, raising doubts about how long the rebound can continue. Some economists and business leaders say Beijing is pulling the same levers it has used in the past to produce growth, leaving untouched a reliance on exports abroad and credit-fueled investment in large infrastructure projects at home—the very model China says it wants to scrap. Over the past two months, China’s industrial output, electricity production and exports have posted solid gains, buoying global markets and easing fears the country would join other emerging economies reeling in anticipation that the U.S. Federal Reserve will curb bond-buying.Beijing says the fact that much of the improvement occurred without major stimulus measures marks a big policy change.

“When the economy is slowing, using a short-term stimulus to boost growth is one method, but we think that doesn’t help solve deep-seated problems,” said Chinese Premier Li Keqiang, speaking at the World Economic Forum in Dalian on Wednesday. “So we chose a strategy that is good for today, and has long-term benefits, maintaining stability of macroeconomic policy.”

But some economists and business leaders say they fear the growth spurt might peter out quickly, making longer-term problems more difficult to solve.

“As long as the credit boom is still under way, the day of reckoning still is likely to be delayed,” said Charlene Chu, an analyst at Fitch Ratings.

Emblematic of China’s recent history of overbuilding, when Premier Li told business executives in Dalian that the government would steer clear of stimulus, he spoke from a new conference center that replaced a state-of-the art venue used for the conference two years ago.

Massive spending on prestige projects buoys short-term growth, but does little to support China’s long-term prospects, economists say.

To be sure, some see a real policy change. Zhu Min, a former top Chinese official who is now a deputy managing director at the International Monetary Fund, applauded Mr. Li’s reassurances that stimulus policies won’t be used. “They aren’t going to do massive infrastructure or other things,” he said, “but they will do investment in new areas, for example, [information technology] and energy efficiencies.”

Government officials say they have made some important changes. But it is hard to see many signs in the latest upturn that a shift in the economic model is gaining traction.

In recent months, it appeared China meant business in reining in a persistent credit boom: A liquidity crunch in June reached levels that alarmed global investors, with short-term interest rates nearing 30% as the central bank sought to choke off excess lending. Still, through the year’s first half, lending levels are markedly higher.

Ms. Chu said the roughly 20% increase over the past year has often come through so-called shadow financing institutions, which funnel funds to local government projects and real-estate developments regulators think are too risky for China’s commercial banks.

“Anyone who thinks China is on the verge of working through its credit problems is mistaken,” she said Thursday.

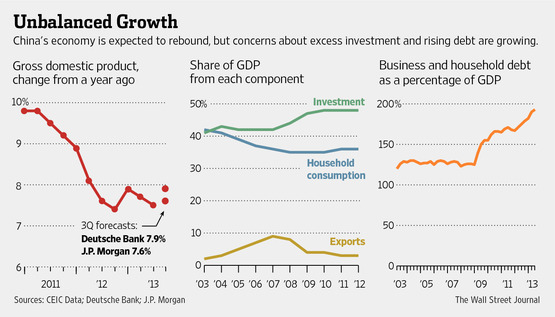

China’s total lending has risen to close to 200% of gross domestic product this year, up from around 125% in 2008.

Ms. Chu said rising debt-to-GDP levels are an indication that much of the lending is used to roll over loans to existing projects rather than financing new ones, which could have a stronger impact on growth.

Smaller companies with higher growth potential routinely complain they can’t get financing because much of the new lending goes to continue to finance megaprojects.

Fast borrowing growth in nations including the U.S., Japan and South Korea resulted in financial disaster or many years of slow growth.

Many economists figure that China has the financial wherewithal to avoid a crash, but a slowdown in lending—unlikely to come until after an important Communist Party conclave in November—could still hinder growth.

Some businesses say they aren’t counting on sustained growth. Edward Y.M. Zhu, chief executive of a Shanghai-based logistics company called Chic Group Global Co., said China relies too frequently on subsidies aimed at boosting infrastructure for short-term gains.

“Those subsidies don’t last long,” he said. “What does are the demands of consumers, so you have to think about the ultimate demand of customers.”

Slightly higher retail-sales growth in August hasn’t boosted businesses’ confidence in a shift toward household spending.

“Overall, our take-away is still slowdown,” said Han Weiwen, a partner at the Shanghai division of consultancy Bain & Co. He said drivers of consumption, such as growth in disposable income, have weakened from previous years.

Growth in urban household income slowed to 6.5% year-over-year in the first half of 2013, down from 9.7% in the same period in 2012.

Nomura said the largest monthly gains in August industrial production came from heavy industries, including steel, iron and coke—sectors marked by overcapacity.

Infrastructure investment is also rising as local governments move to support growth. Through August, spending on highways is up 23.8%, compared with the year-earlier period.

China’s leaders made clear during June and July that they sought “stability” after China’s GDP had slowed for two consecutive quarters.

For the year’s first half, China grew at a 7.6% rate and was in danger of missing the government’s annual target, 7.5% this year, for the first time since 1998, which would be a major embarrassment for China’s new leadership.

The June squeeze on borrowing costs triggered a sharp slowdown in lending. But that reversed again in August as total social financing, China’s broadest gauge of lending, surged to 1.57 trillion yuan ($256.6 billion) from 808 billion yuan in July, suggesting that China again was using credit to boost growth.

Meanwhile, the global economy improved somewhat, giving a boost to China’s exports. Jun Ma, an analyst for Deutsche Bank, estimates growth in the U.S., Japan and Europe overall will be higher next year, which should translate into a 3-4 percentage-point acceleration in Chinese exports.

Still, Chinese exporters are skittish about making the kinds of investments that can further boost growth.

Angela Tu, chairman of Xinpeng International Co, a shoe exporter in Wenzhou, says sales are up about 10% from last year, but the company doesn’t plan to expand. “Right now, our priority is to be stable and cut down expenditures and lay off workers if necessary.”