Wanted: Jobs for the New ‘Lost’ Generation; Five years after the 2008 crisis, younger adults still struggle to find work

September 14, 2013 Leave a comment

Updated September 13, 2013, 11:15 p.m. ET

Wanted: Jobs for the New ‘Lost’ Generation

Five years after the 2008 crisis, younger adults still struggle to find work

BEN CASSELMAN and MARCUS WALKER

Like so many young Americans, Derek Wetherell is stuck. At 23 years old, he has a job, but not a career, and little prospect for advancement. He has tens of thousands of dollars in student debt, but no college degree. He says he is more likely to move back in with his parents than to buy a home, and he doesn’t know what he will do if his car—a 2001 Chrysler Sebring with well over 100,000 miles—breaks down.“I’m kind of spinning my wheels,” Mr. Wetherell says. “We can wishfully think that eventually it’s going to get better, but we don’t really know, and that doesn’t really help us now.”

Mr. Wetherell is a member of a lost generation, a group that is only now beginning to gain attention of many economists and employment experts. From Oakland to Orlando—and across the ocean in Birmingham and Barcelona—young people have come of age amid the most prolonged period of economic distress since the Great Depression.

Most, like Mr. Wetherell, have little memory of the financial crisis itself, which struck while they were still in high school. But they are all too familiar with its aftermath: the crippling recession, which made it all but impossible for many young people to get a first foothold in the job market, and the achingly slow recovery that has left the prosperity of their parents’ generation out of reach—perhaps permanently.

“This has been for quite a while now a hostile environment for young people,” said Paul Taylor, executive vice president of the Pew Research Center, which has studied the impact of the recession on young people. “This is all they’ve really known.”

The financial crisis that struck five years ago this month opened up a sinkhole in the U.S. economy that swallowed Americans of all ages and backgrounds. Retirees lost life savings. Families lost homes. Millions of Americans lost their jobs.

Five years later, that hole is being filled in, however slowly. The unemployment rate is down to 7.3% amid slow, steady job growth. The stock market has rallied to new highs. Home prices are rebounding. Total output has surpassed its prerecession peak.

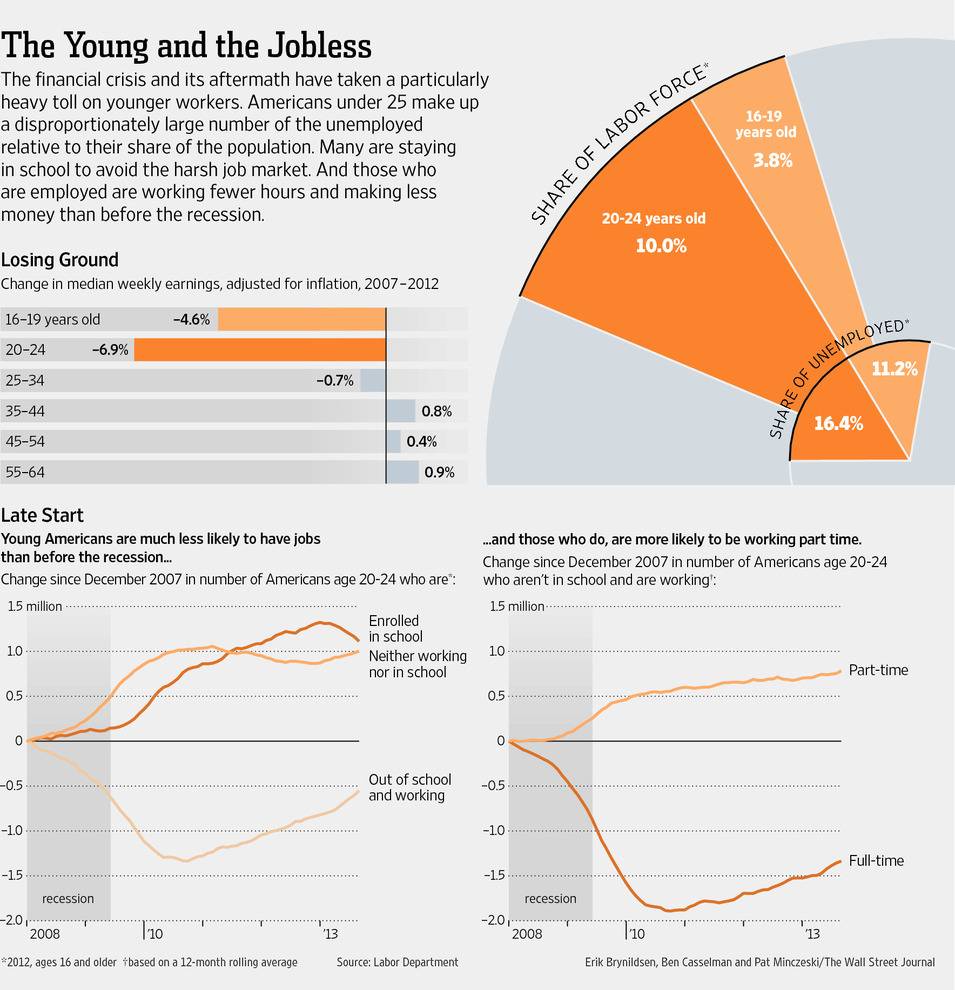

But the recovery has left many young people behind. The official unemployment rate for Americans under age 25 was 15.6% in August, down from a peak of nearly 20% in 2010 but still more than 2½ times the rate for those 25 and older—a gap that has widened during the recovery. Moreover, the unemployment rate ignores the hundreds of thousands of young people who have taken shelter from the weak job market by going to college, enrolling in training programs or otherwise sitting on the sidelines. Add them back in, and the unemployment rate for Americans under 25 would be over 20%.

Even those lucky enough to be employed are often struggling. Little more than half are working full time—compared with about 80% of the population at large—and 12% earn minimum wage or less. The median weekly wage for young workers has fallen more than 5% since 2007, after adjusting for inflation; for those 25 and older, wages have stayed roughly flat.

This generation’s struggles have few historical precedents, at least in the U.S. The recession of the early 1980s was comparable but was followed by a rapid recovery. The economic legacy of the Great Depression was erased to a large degree by World War II and the boom that followed. No similar rebound looks likely this time around.

What evidence does exist suggests today’s young people will suffer long-term consequences. One recent study by Yale University economist Lisa Kahn found that after the 1980s recession, new college graduates lost 6% to 7% in initial wages for every one percentage point increase in the unemployment rate. The effects shrank over time, but even 15 years after graduation, those who finished college in bad economic times earned less than similar people who graduated in better times. Some never caught up at all.

Mr. Wetherell, the son of an electrician, grew up in Imperial, Mo., a small town south of St. Louis where job opportunities were limited even when the economy was strong, which it wasn’t when he graduated from high school in 2008. He enrolled at the University of Missouri-St. Louis, juggled a full course load and a full-time job at a local grocery store and tracked his near-constant commitments on a dry-erase board in his room.

Eventually the schedule wore him down. He withdrew from school in 2011, though he says he still plans to complete his degree. He owes $27,000 in student debt—roughly his annual pretax earnings—with three semesters still to go.

Mr. Wetherell is better off than many of his peers. He works at Schnucks, a locally owned supermarket chain where he is a union member, receives health benefits and is paid $12.65 an hour. That is enough to cover $400 monthly rent and $200 in student loan payments. But it leaves little left over for an emergency fund, let alone retirement savings. “It’s kind of unsettling not being able to put anything away,” says Mr. Wetherell, a political science major.

Even more unsettling: Mr. Wetherell has noticed that more and more of his co-workers have college degrees, some from well-regarded colleges like Washington University. What he had intended as a job to help pay his way through college has now turned into a destination for college graduates. “I think a lot about whether I’m ahead or behind,” he says. “I really hope I’m not ahead.”

Americans aren’t the only ones asking such questions. The financial crisis that began in the U.S. quickly rippled across the Atlantic, bursting similar credit and property bubbles in countries such as the U.K., Ireland and Spain, and crippling a European banking sector that had dense links with the U.S. financial system.

Much of Europe’s economy was plunged into its worst postwar slump and has struggled even more than the U.S. to regain its precrisis levels of growth and jobs. In Europe, the banking crisis also triggered a second-wave crisis—massive capital flight from Southern European countries that relied on foreign borrowing—that came close to unraveling the euro.

The still-lingering malaise has hit young Europeans even harder than young Americans. The global financial crisis and its aftermath have exacerbated older problems of sclerotic labor markets in countries such as France, Italy and Spain, where young workers already faced a struggle to find solid jobs even before the crash. Over 23% of the European Union’s workforce under age 25 is unemployed, and youth jobless rates in the worst-hit European countries approaches 60%.

In the U.K., whose financial fortunes mirrored the U.S.’s closely, so many young people have been pushed to society’s shadows that they have their own name—NEETs—for “not in education, employment or training.” Their existence has helped to fray the social fabric not only in London, but places like Athens and Stockholm. Those cities have seen riots led by young people who have become alienated from political and economic institutions that no longer seem to offer hope of prosperity.

The U.S. has thus far escaped such turmoil. Polls show young Americans remain generally optimistic about their long-term future, even as they remain pessimistic about their immediate prospects.

But there are signs that the weak economy is leading to deep societal changes. An entire generation is putting off the rituals of early adulthood: moving away, getting married, buying a home and having children. The marriage rate among young people, long in decline, fell even faster during the recession, and the birthrate for women in their early 20s fell to an all-time low in 2012. According to a recent Pew Research study, 56% of 18- to 24-year-olds lived with their parents in 2012, up from 51% in 2007—an increase that looks particularly dramatic because the share had changed little in the previous four decades.

Moreover, many young people are losing hope of matching the prosperity of their parents’ generation. Just 11% of employed young people in a recent Pew survey said they had a career as opposed to “just a job”; fewer than half said they were even on track for one.

John Connelly thought he was right on track in life. The son of a New Jersey auto mechanic, he was the first in his family to go to college when he enrolled at Rutgers in 2009. Four years later, the 22-year-old found himself $21,000 in debt, without a permanent job and sleeping on friends’ couches in New Jersey and Brooklyn.

“I hear a lot of stuff that people in my generation aren’t buying cars or houses, and I’m a step beyond that—I can’t even pay rent on time,” Mr. Connelly says. “I have a hard time planning 10 years in the future when I can hardly plan three months in the future.”

At Rutgers, Mr. Connelly was an honors student and president of the student assembly. But wary of taking on more debt, he ended up withdrawing from school with three credits to go until graduation. After a summer spent living with friends while working a temporary job at a Brooklyn nonprofit, he found a grant that allowed him to re-enroll in school this fall. But he still doesn’t know what he’ll do when he graduates at the end of the semester. “I kind of did everything I was quote-unquote ‘supposed’ to be doing,” he says.

The costs of a “lost generation” go beyond the impact on young people themselves. A 2012 analysis commissioned by the Corporation for National and Community Service, a federal agency, estimated that the 6.7 million American youth who are disconnected from both school and work could ultimately cost taxpayers $1.6 trillion in lost tax receipts, increased reliance on government benefits and other expenses. Look at broader economic and social effects such as lost earnings and increased criminal activity and the impact tops $4.7 trillion, the researchers estimated.

“We end up paying a huge price for all of this because these kids don’t earn, they don’t pay taxes, they stay at home, they don’t get married,” said Andrew Sum, a Northeastern University economist. “It’s not just the kids that lose. It’s all of us as a country that lose.”

The impact of the weak economy varies by education. In the short-term, less-educated workers are less likely to have jobs, and earn less than college graduates when they do. But better-educated workers may face more lasting consequences.

Economic research has shown that the first few years after college play an outsize role in determining workers’ career trajectories: About two-thirds of wage growth, on average, comes in the first 10 years of a person’s career. In weak economic times, graduates are likely to accept lower wages and work for smaller companies with fewer opportunities for advancement. And in many cases, they never move off that second-tier track.

“In a recession, you’re probably going to be starting out at a lower wage at a less attractive firm,” said Till von Wachter, a UCLA economist. “The first few years is about carving your path, and after three or four years you’re not newly minted anymore. You’ve chosen your career.”

Moreover, many college graduates face an added challenge that was far less common in earlier generations: mountains of student debt. Even as mortgage and consumer debt plunged in the wake of the financial crisis, student loan balances nearly tripled from 2004 to 2012, to roughly $1 trillion, according to a recent study by the Federal Reserve Bank of New York. More than 40% of 25-year-olds now hold at least some student debt. The average borrower owes roughly $25,000.

The rising level of student debt, especially during a period of poor job opportunities, is likely to have long-term consequences. A recent study from the left-leaning think tank Demos estimated that $53,000 in student debt—the average debt burden for a household with two college graduates—will reduce lifetime wealth by more than $200,000. Robert Hiltonsmith, the study’s author, said high debt levels are making it harder for graduates to advance in their careers by changing jobs, moving to a different city or accepting internships that can open up career opportunities down the road.

“Beyond just the impact on assets, it does have that direct impact on career choices,” Mr. Hiltonsmith said. “They’re not able to make those decisions that make their salaries rise.”

Emily Koehler, a friend of Mr. Wetherell’s, graduated from the University of Missouri-St. Louis and hoped to go into public policy or the nonprofit sector. But with $26,000 in debt, Ms. Koehler, 23, couldn’t afford to take an unpaid internship to get a leg up, and she’s reluctant to take on even more debt to get the master’s degree she would need to advance in her field.

Instead, Ms. Koehler is doing clerical work for $15 an hour at a local remodeling firm. Her husband, an Egyptian national, has found only temporary work; the couple is trying to save up for when his contract ends in a few weeks. So far, they have $2,000.

Sitting in the couple’s cozy one-bedroom apartment—filled with furniture borrowed from family or bought at Goodwill—Ms. Koehler says she is less worried about the present than the future. She says she can’t imagine when she’ll be able to afford a house or children.

She and her husband talk about moving to another city, but worry about leaving behind the support system they have in her native St. Louis.

Of course, even in good economic times, small apartments, hand-me-down furniture and empty savings accounts are a fact of life for many 20-somethings—or even a badge of honor. But Ms. Koehler fears her bare-bones reality will continue long after the romance has faded.

“You don’t dream big,” she says. “You’re always checking yourself, or you don’t even think about doing other things anymore.”