Debt explosion real story of Fed QE dance; Western finance cannot be fixed without tackling credit addiction

September 20, 2013 Leave a comment

September 19, 2013 5:14 pm

West’s debt explosion is real story behind Fed QE dance

By Gillian Tett

Western finance cannot be fixed without tackling credit addiction

The danger with addictions is they tend to become increasingly complusive. That might be one moral of this week’s events. A few days ago, expectations were sky-high that the Federal Reserve was about to reduce its current $85bn monthly bond purchases. But then the Fed blinked, partly because it is worried that markets have already over-reacted to the mere thought of a policy shift. Faced with a choice of curbing the addiction or providing more hits of the QE drug, in other words, it chose the latter.In many ways this is understandable; the real economic data is still soft. But as investors try to fathom what the Fed will (not) do next, it is worth pondering a timely speech made recently by former UK regulator Lord Turner. As he told Swedish economists last week, and repeated to central bankers and economists in London this week, the real story behind the recent dramatic financial sagas – be that the market dance around QE or the crisis at Lehman Brothers five years ago – is that western economies have become hooked on ever-expanding levels of debt.

Until this situation changes it is delusional to think that anyone has really “fixed” western finance with post-Lehman reforms, or created truly healthy growth, Lord Turner insists. Put another way – although he did not say so bluntly – one way to interpret this week’s dance around QE is that policy makers are continuing to prop up a financial system that is (at best) peculiar and (at worst) unstable.

Such criticisms, of course, are not new: maverick far-right and far-left economists have been making them for years. But what makes Lord Turner’s contribution notable is that until recently he was sitting at the centre of the global financial system – and post-Lehman reform process – he now thinks is so flawed. And from that perspective he points out some curious contradictions. Take what banks do. A standard economics text book, Lord Turner writes, claims that banks exist to “raise deposits from savers and then make loans to borrowers” . . . and “primarily lend to firms/entrepreneurs to fund investment projects”. Thus “demand for money is a crucial issue” in terms of growth.

But this depiction is a fiction, he says. The reason? He calculates that today in the UK a mere 15 per cent of total financial flows actually go into “investment projects”; the rest support existing corporate assets, real estate or unsecured personal finance to “facilitate lifecycle consumption smoothing”.

Some non-investment finance is socially useful, Lord Turner admits; but much is not. In real estate, for example, most credit just “funds the purchase of already existing houses” rather than investment in new homes (ie construction). And what is really striking about the non-investment piece of this financial picture is that it has exploded; as a result, as the Bank of England’s Andy Haldane also pointed out in a debate in London last week, the size of private credit, relative to GDP, has doubled to 200 per cent in the past 50 years.

This makes a mockery of existing textbooks and official policy assumptions. But the explosion in credit has another peculiar implication, both Mr Haldane and Lord Turner note: since total credit keeps rising inexorably, even as growth remains flat, the “productivity” of money is falling, even as the propensity of the over-leveraged system to have booms and busts, amid investor sentiment swings, has risen.

So is there any solution? Lord Turner offers a few ideas. He wants a radical overhaul of the intellectual models that economists use (including, presumably, those in central banks.) He also wants policy makers to deliberately reduce credit. Thus the Basel III framework for banks should have tough counter-cyclical capital requirements, he argues, and regulators should reintroduce “into the policy toolkit quantitative reserve requirements, which more directly constrain banking multipliers and thus credit growth than do increases in capital requirements”.

Now, of course, that is not happening; on the contrary, British banks are under political pressure to provide more mortgages, as house prices hit new peaks, and the Fed is so determined to kickstart the US housing market it keeps gobbling up those mortgage bonds. Of course, the official policy line is that this is just a temporary affair: once there is strong, sustainable growth, this will stop.

But don’t bet on that soon; or not in a world where asset prices and animal spirits are now so dependent on cheap money, and so central in driving growth. Either way, as investors celebrate this week’s QE decision, they would do well to remember that 15 per cent estimate for productive investment. And it would be fascinating if somebody tried to work out what the ratio for the US economy is today. Particularly if that calculation was to emerge from the Fed.

September 19, 2013, 7:50 p.m. ET

Fed’s Guidance Questioned As Market Misreads Signals

JON HILSENRATH

The markets received a shot of adrenalin when the Federal Reserve opted not to cut back on its bond-buying program. Robert Tipp, chief market strategist for Prudential fixed income, has advice on how investors should respond. Photo: AP

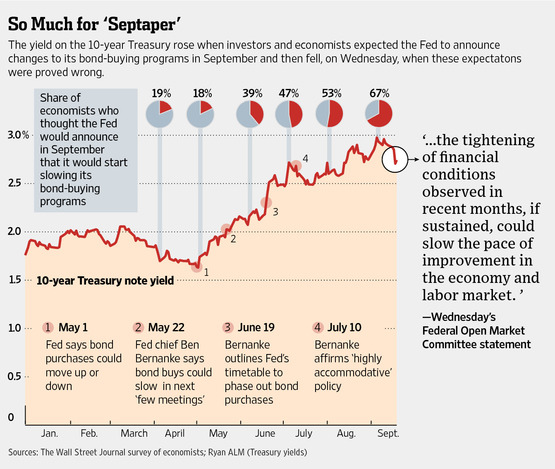

Federal Reserve officials created new uncertainty about how much farther they will push their easy-money policies—and new questions about how effective they are at communicating their thinking—with the decision to stand pat on the pace of their bond purchases for now.

The Fed on Wednesday went beyond merely deciding to keep buying the $85 billion a month of mortgage-backed securities and U.S. Treasurys that it had been telegraphing for months it might start winding down. In the news conference after a two-day policy meeting, Fed Chairman Ben Bernanke also seemed to walk away from some of the guidance he had given in June on how the bond-buying program would play out over the next year, making it even less clear when the program will end.

Mr. Bernanke said Wednesday that he thought the decision not to begin pulling back on bond purchases was right given a weaker economy than the Fed expected a few months ago and one facing new threats from a fiscal showdown in Washington. He also said the Fed might still proceed with a pullback in the months ahead if the economy cooperates.

In his defense, Mr. Bernanke said that he has never said the Fed would start the pullback in September and that the decision always depended on the economy’s vigor. “I don’t recall stating that we would do any particular thing in this meeting,” Mr. Bernanke said at the news conference.

Yet some investors and analysts said the Fed’s action was the latest in a series of communications missteps, demonstrated by the fact that numerous surveys showed investors broadly expected the central bank to move in September.

Fed officials place heavy weight on communicating clearly to investors how they’re likely to behave. They believe that guiding the public about the Fed’s future actions influences spending and investing decisions in the present, making monetary policies more effective in helping the economy. Part of the Fed’s strategy, for instance, is to assure the public that it will keep short-term interest rates low for several years and that its bond-buying program will be in place as long as the economy needs added support—signals aimed at holding down long-term interest rates to boost growth.

But the events of the past months and Wednesday’s market reaction show the potential pitfalls when Fed communications on monetary policy—the so-called forward guidance—are conditional, complicated, nuanced or misread by much of the investing public.

Market expectations of a bond-buying pullback had caused U.S. interest rates on mortgages and bonds to rise since May, when Mr. Bernanke began talking about the timetable for the Fed to begin cutting its bond purchases. The rate increases crimped the U.S. housing rebound, while the expectations triggered stock and currency selloffs in emerging markets that caused turmoil for developing economies. Then, on Wednesday, Mr. Bernanke cited higher U.S. interest rates as a threat to the recovery and among the reasons for holding off on a reduction in bond purchases

“The whole key to forward guidance is you have to have the market rely upon what you’re telling them,” said Scott Minerd, chief investment officer at Guggenheim Partners, an investment firm with more than $180 billion in assets under management. “What the Fed did…decreased their credibility in terms of being able to use forward guidance.”

In Wednesday’s news conference, Mr. Bernanke said: “We can’t let market expectations dictate our policy actions. Our policy actions have to be determined by our best assessment of what’s needed for the economy.”

The Fed’s mixed signals Wednesday were the latest in the five-months-running drama surrounding the fate of the bond-buying program. In May Mr. Bernanke said the Fed could in its “next few meetings” start winding down the bond-buying program. The Fed has held three policy meetings since then.

After a policy meeting in June, Mr. Bernanke set out some markers on the bond purchases in a bid to give unnerved investors more clarity about the future. He said officials expected to start pulling the program back before year-end and to wind it down fully by mid-2014, when they expected the unemployment rate to be around 7%.

In August, an unusual silence surrounded the Fed’s top officials. Mr. Bernanke skipped his annual comments at the Jackson Hole, Wyo., central-bank conference sponsored by the Federal Reserve Bank of Kansas City. Vice Chairwoman Janet Yellen remained silent, too, trying to avoid the limelight as the White House considered her as a possible nominee to succeed Mr. Bernanke after he leaves the Fed’s top job in January. Meantime several regional Fed bank presidents said in interviews that they might be open to moving at the September meeting to start scaling back the bond purchases.

Investors thought a pullback was to be announced at the September meeting, but the economy hadn’t cooperated, showing signs of decelerating during the summer with new risks looming. Many Fed officials went into the meeting on the fence about acting.

On Wednesday, Mr. Bernanke hedged on his guidance.

On the timetable for a bond-buying wind-down, he offered only lukewarm assurances that it will start this year, saying “if the data confirm our basic outlook…then we could move later this year.” And on the 7% marker in the unemployment rate, he said “there is not any magic number.”

Investors at first liked the message of continued easy money from the Fed Wednesday, but curbed their enthusiasm Thursday. The Dow Jones Industrial Average finished down 40.39 points, or 0.26%, at 15636.55. Yields on 10-year Treasury notes rose 0.056 percentage point to 2.749%, contrary to a big drop in yields on Wednesday.

Some analysts questioned the Fed’s credibility Thursday after its decision to hold off.

“We are worried that when the time comes to taper, and someday tighten, the Fed will not have the courage to follow-through,” Joseph LaVorgna, a Deutsche Bank economist, said in a note to his clients Thursday. “In turn, policy makers will shy away from taking sufficiently aggressive action.”

Wall Street analysts spent Wednesday and Thursday scrambling to map out new estimates of how large the Fed’s already swollen bondholdings will get by the time it is finished with the program. The overall size of its holdings matters to the Fed and Wall Street, because officials believe the impact of the Fed’s program grows as its holdings grow, and so do the risks.

The Fed has been buying bonds since last September—the third iteration of a program also known as quantitative easing, or QE—to hold down interest rates, push up the value of assets like homes and stocks, and encourage more spending, investing and economic growth.

Using the old guidance Mr. Bernanke had set out, investors and analysts could easily plot out that the Fed expected to accumulate securities and other assets totaling more than $4 trillion in all by the time it was done, up from less than $800 billion when it started intervening aggressively in financial markets in 2008 to counteract the financial crisis. With the new, vaguer guidance, the outlook for the Fed’s balance sheet is now a bit less clear.

One rule of thumb used by economists is that every $100 billion the Fed adds to its balance sheet reduces the yield on a 10-year Treasury note by 0.03 percentage point. But there is no perfect measure of the impact of the Fed’s actions, which often resonate in financial markets more loudly than anyone expects.

The Fed could still follow much the same path that it laid out before and begin winding the program down in the months ahead, finishing by mid-2014. As Mr. Bernanke said, “we do have the same basic framework that I described in June.”

Julia Coronado, an economist with BNP Paribas and a former Fed researcher, said Mr. Bernanke’s move Wednesday gave the central bank more wiggle room amid an economic outlook that became more uncertain since the Fed met in June. “This gives them more flexibility,” she said.

Still, Ms. Coronado thinks in the end the Fed will follow a timetable that isn’t much different than what Mr. Bernanke laid out before. She sees the Fed’s total bondholdings hitting $4.3 trillion by the time the program ends.

Though the Fed appeared to be less certain about the outlook for its bond-buying program, officials sent a clear message Wednesday about how they see short-term interest rates moving in the years ahead. Their bottom line: not much at all.

New estimates released by the Fed showed the vast majority of officials don’t expect the Fed to raise its benchmark short-term interest rate before 2015 or later, and by the end most don’t expect it to get any higher than 2%.

“It’s our intent to maintain a highly accommodative policy,” Mr. Bernanke said.