Boom Time for Broadcast Stocks

September 22, 2013 Leave a comment

SATURDAY, SEPTEMBER 21, 2013

Boom Time for Broadcast Stocks

By ALEXANDER EULE | MORE ARTICLES BY AUTHOR

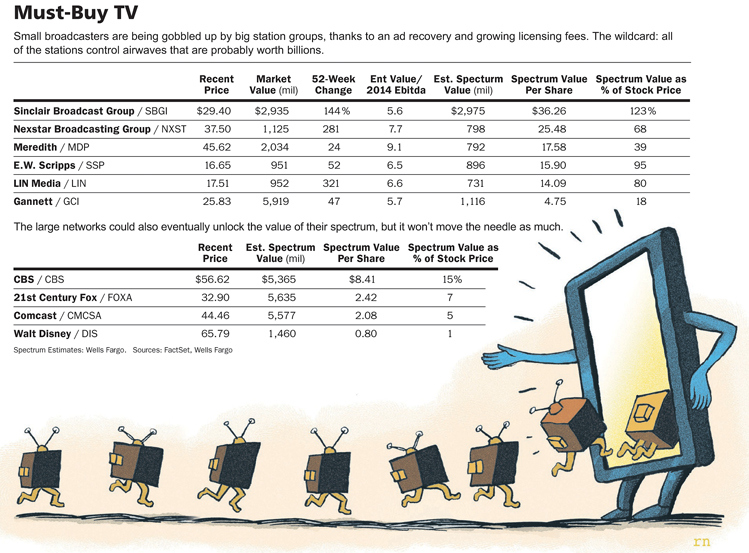

Local broadcasters control valuable spectrum that could be leased to wireless operators. Why Sinclair and Nexstar could be worth as much as twice their current quotes.

Something quaint is happening in TV land. Amid all the talk about new technologies for delivering video, it’s the local broadcasters—the companies that carry local news and sitcom reruns—that are stealing the show. Shares of Nexstar Broadcasting Group (ticker: NXST), an operator of 72 local TV stations, are up 254% in 2013. The surge bests even the torrid pace of Netflix (NFLX), the leading proxy for TV’s hyped future. Sinclair Broadcast Group (SBGI), with 149 stations, is the largest of the pure-play broadcasters; its shares are up 133%.The party is just under way. Nexstar and Sinclair could easily gain 20% in the coming year. And the stocks could double from there, as investors begin to recognize the considerable value tied up in the airwaves. Spectrum is a hot commodity, as consumers pull more and more data to their smartphones. And the broadcasters, thanks to TV’s over-the-air history, happen to control a large swath of airborne real estate. Broadcast bulls contend that Nexstar and Sinclair’s spectrum licenses could be worth as much as the companies’ entire market value today.

Eric Green, director of research at Penn Capital Management in Philadelphia, has been pounding the table for Nexstar and Sinclair for two years. They’re the firm’s largest holdings. “There are multiple ways to win with broadcasters, and valuations are no higher than they were two years ago,” he says.

In the near-term, broadcasters are benefiting from an ad recovery, just as a new revenue stream from licensing content kicks into gear. After years of giving away their channels to cable and satellite companies, the broadcasters have found religion when it comes to getting paid for content. And broadcast content remains a living-room mainstay. Most top-rated shows still originate on the broadcast dial—including popular sitcoms and big-event programming like the Super Bowl and Academy Awards.

Recent battles for these so-called retransmission fees have been public and bruising. CBS(CBS) and Time Warner Cable (TWC) just settled a monthlong fight in which CBS was pulled from Time Warner dials in New York, Los Angeles, and Dallas.

The fights haven’t earned any good will, but the hard line is good business for the station owners. Industry observers believe CBS ultimately wrangled a 150% increase in fees from Time Warner Cable, to nearly $2 per subscriber. Green says “CBS just set the bar” for future retrans agreements, which generally last three years.

Media-research firm SNL Kagan estimates the average broadcaster across the country still gets less than $1 per subscriber from cable and satellite providers. (CBS and the other networks, NBC, Fox and ABC, all own local stations in some of the country’s major markets. But most of the country’s 1,400 commercial stations are owned by smaller station groups or even mom-and-pop shops.)

POLITICAL ADVERTISING IS also growing, thanks to the Supreme Court’s Citizens United ruling in 2010. The decision overturned restrictions on “electioneering communication” and opened the floodgates for campaign and issue ads. Sure enough, political-ad dollars during the 2012 campaign totaled $2.7 billion, according to ad-buying firm Magna Global, a 56% jump from 2008. Magna recently forecast that political-ad spending could top $3.3 billion in 2016. Most of the dollars flow to the local TV stations, given the targeted nature of elections.

Even the midterm election in 2014 could break the 2012 record. “I think it’s going to be off the charts for one reason: Obamacare,” says Ed Atorino, who covers broadcasters for Benchmark Co.

All the good news has set off a wild wave of consolidation in the broadcast space. Sinclair and Nexstar, along with Gannett (GCI) and Pink Sheets-traded Tribune (TRBAA)—both newspaper/broadcast hybrids—have led a $10 billion buying binge in 2013, according to SNL Kagan. The deals carry significant synergies, mainly because of a mechanism that allows the large acquirers to apply their higher retrans fees to the acquired firms, which always lacked the scale to negotiate favorable rates.

The acquired stations, in other words, become instantly more profitable for the bigger broadcast groups than they are as standalones.

Consolidation has become so profitable that investors bid up acquiring companies as soon as deals are announced, a rarity on Wall Street. In June, Gannett announced it was buying Belo, a smaller station owner, for $1.5 billion. Shares of Gannett soared 34% on the news, adding $1.5 billion in market value.

The most-willing sellers have already been bought up this year, but higher valuations could set off another consolidation wave.

“We’re probably around the fifth inning, probably a little over halfway through the game,” says David Amy, Sinclair’s chief financial officer.

THE FEDERAL COMMUNICATIONS Commission has started to talk about proposals that could put a damper on the consolidation parade. The chatter caused both Nexstar and Sinclair to sell off from their mid-summer highs. Consolidation or not, plenty of opportunity remains thanks to the broadcasters’ growing cash flows.

At a respective 7.5 and 5.5 times 2014 estimated cash flow (earnings before interest, taxes, depreciation, and amortization), Nexstar and Sinclair both trade well below their 2007 levels, despite greater clarity about future revenue. Meanwhile, pure-play cable-channel owners Discovery Communications (DISCA) and AMC Networks (AMCX) trade at 13 and 10 times, respectively.

Despite the big stock moves, Sinclair and Nexstar—with market values of $2.9 billion and $1.1 billion, respectively—remain fairly unknown on Wall Street. Just six analysts cover Sinclair, and six track Nexstar. Compare that with 26 for Discovery and 16 for AMC. A whopping 34 analysts cover NBC-owner Comcast (CMCSA).

Martin Sass, chairman and CEO of M.D. Sass, has been buying shares of Sinclair and Nexstar since July. Without any contribution from spectrum, he puts a near-term price target of $38 on Sinclair and $43 on Nexstar, upside of 30% and 15%, respectively. Sinclair shares carry a dividend yield of 2.1%; Nexstar’s yield is 1.3%. (Both yields could rise substantially, Sass says, if and when the M&A opportunity dries up.)

Wells Fargo’s Marci Ryvicker is one of those few analysts who has stuck with broadcast; she rates Sinclair and Nexstar at Outperform. Her latest research attempts to answer just how much their spectrum is worth.

Ryvicker has studied the FCC’s auctions in 2008, when it raised $19 billion from wireless carriers in return for a block of spectrum. Using the 2008 auction as a baseline, Ryvicker estimates Sinclair’s spectrum alone is worth $3 billion, or $36 a share. Nexstar’s spectrum could be worth $800 million, or $25 a share.

Eric Green at Penn Capital argues that none of the value is in the stocks, given cash-flow multiples that value the existing business at a historical discount. Sinclair closed at a recent $29.40 and Nexstar at $37.50.

“Right now spectrum is valued at zero,” Green concludes.

The big networks could eventually monetize the spectrum from their owned-and-operated stations, but it’s a smaller opportunity for the larger, more-diversified companies. CBS’s spectrum is worth some $5.4 billion, according to Ryvicker, approximately 15% of its market value.

AS WIRELESS CARRIERS grapple with maxed-out networks, there’s a strong policy argument behind repurposing the TV spectrum. “This is grossly underused spectrum,” says Martin Sass. He notes that just 10% to 15% of Americans receive their television over the air.

In 2010, the FCC published a 376-page National Broadband Plan, responding to Congress’ call to expand Internet access across the country.

Repurposing some TV spectrum to improve broadband service isn’t a hypothetical concept. The 2008 auction stemmed from spectrum that the broadcasters once held for analog broadcasts. (They relinquished those assets in exchange for spectrum that was better suited to digital TV.)

Blair Levin, a senior FCC staffer during the Clinton administration, oversaw the national broadband report. He points out that America’s leadership in 4G wireless services is a direct result of the aggressive plan the FCC made in the 1990s to repackage analog-TV spectrum.

The FCC’s latest plan, which stems from Levin’s report, is to hold an incentive auction that would encourage broadcasters to return their spectrum in exchange for large one-time payments. The auction would essentially have the government acting as a broker between broadcasters and wireless operators.

That voluntary auction is scheduled for 2014, but it’s likely to be delayed. And some big players may choose not to participate, anyway. Sinclair, for example, says it would rather lease spectrum directly to wireless carriers, while continuing to operate their TV stations. That go-it-alone approach would require industry agreement around a new standard known as ATSC 3.0. The upgrades, which Sinclair says are gaining momentum, would allow data streams, not just broadcasts, to be sent over TV spectrum. The government, based on current license agreements, would get 5% of this “ancillary revenue.”

However the spectrum shakes out, for the broadcasters the sky may be the limit.