CEOs to Reveal Their ‘Cheap Number’; SEC Wants to Compare CEO Pay with Average Worker’s

September 22, 2013 Leave a comment

September 21, 2013, 8:30 p.m. ET

CEOs to Reveal Their ‘Cheap Number’

SEC Wants to Compare CEO Pay with Average Worker’s

AL LEWIS

Perhaps you’ve seen those commercials for the Sleep Number mattress. What’s your Sleep Number? Learn it and you’ll have pleasant dreams. There is another number that’s giving the chief executives of America’s largest companies nightmares. It expresses the ratio of their pay to that of their employees. I call it the Cheap Number. In 1977, renowned management thinker Peter Drucker wrote a piece for The Wall Street Journal complaining that this number had grown as high as 50 at many companies. “A ratio of 25-to-1…is well within the ratio most people in this country…consider proper and indeed desirable,” he wrote. Today the number is 354, according to a study touted by the AFL-CIO. Other studies show it well over 1,000 at some companies. A recent analysis by Bloomberg compared a former J.C. Penney CEO to a former J.C. Penney cashier and pegged the number there at 1,795. Knowing this number raises a salient question: If you own a business, what would you rather have for your money? An army of more than 1,000 workers, or one delusional jerk in a suit? The world is filled with enterprises paying fortunes to chief executives, but relatively little to almost everyone else.Last week, the Securities and Exchange Commission finally proposed a rule that would require large, publicly traded companies to report the ratio of their CEO’s pay to the median pay of their workers.

The Dodd-Frank financial-reform act of 2010 mandates that the SEC adopt this rule, but the regulator has been overrun by corporate lobbyists trying to block it.

The SEC said it has received 22,860 letters and a petition with 84,700 signatures. Thousands of pages of blah, blah, blah, and waa, waa, waa, arguing why America’s biggest companies can’t calculate their Cheap Numbers.

Complying would be “highly costly and burdensome, with tremendous uncertainty as to accuracy,” wrote lawyers from Davis Polk, a Washington firm representing America’s six largest banks.

Also piling on were groups like the HR Policy Association, which represents the human-resource officers of more than 300 large companies; the Retail Industry Leaders Association, which represents more than 200 retailers; and the American Benefits Council, a lobbying group that represents Fortune 500 companies.

“There is a widespread misconception that this information is readily available at the touch of a button,” wrote a group of trade associations.

It’s not? Sarah Anderson of the Institute for Policy Studies, which has lobbied for the rule, finds this puzzling. Coming up with numbers is what companies do best. “If they don’t know what they’re paying their own employees, their investors should be worried,” she said.

The more likely explanation is that CEOs don’t want their Cheap Numbers reported because they could be used against them in debates over tax policies and legislative reforms.

Even some of their own shareholders might want them to take their Cheap Numbers down a notch. “This further opens the window on CEO pay and will help shareholders to keep management accountable,” the California Public Employees’ Retirement System wrote in a news release applauding the proposal.

“They have reasons to be this paranoid,” Ms. Anderson said. “They probably spent more money lobbying against this thing than it would cost them to just come up with the number.”

Updated September 20, 2013, 7:23 p.m. ET

It’s Hard to Slice and Dice CEO Paychecks

The SEC is proposing new CEO pay disclosure, but it’s not as simple as it may seem.

Federal regulators want companies to reveal how much more their chief executives make than a typical employee, but the disclosures may not help investors determine whether a CEO’s pay is out of step with his peers.

Analysts say the so-called pay ratios will vary based on differences in how companies deploy their workforces and how they’ll crunch the numbers.

Ratios at companies with predominantly U.S. employees will likely be lower than at companies with lower-paid employees abroad. Companies that outsource work will post different ratios than rivals that use their own employees to perform the same tasks. Part-time and temporary employees could further skew the ratio, since the Securities and Exchange Commission said they must be included.

“I just don’t see how there’s going to be a company-to-company comparison that’s going to be all that meaningful,” said Mark Borges, a principal at executive-compensation consultant Compensia Inc. Mr. Borges thinks the ratio will be most useful in assessing pay equity at a single company over time, as it grows or shrinks.

The SEC on Wednesday proposed that companies compute the pay of their median worker and compare that figure to the pay of the CEO. The median is the point where half the workers make more and half make less. The proposal would flesh out a provision of the 2010 Dodd-Frank financial-reform law. The SEC said it would accept comments on its proposal for 60 days. The rule will likely take effect in 2015 or 2016, depending on when the SEC takes final action.

In its proposal, the SEC said companies could use differing methods to identify their median employee, including looking at a sample, rather than all employees. Analysts said that provision, aimed at reducing the record-keeping burden on large, global companies, would make company-to-company comparisons more difficult.

The freedom in selecting the median-paid employee drew praise from one large global company that met with SEC commissioners and staffers as they drafted the rule. Health-care company Johnson & Johnson credited the agency’s “practical approach” and consideration of compliance costs. J&J said the rules “appear designed to provide significant flexibility” to companies trying “to comply with an otherwise onerous disclosure requirement.”

At the same time, Arthur Kohn, a partner who specializes in executive compensation at Cleary Gottlieb Steen & Hamilton LLP, said the flexibility “undermines the ability to compare [ratios] on an apples-to-apples basis.”

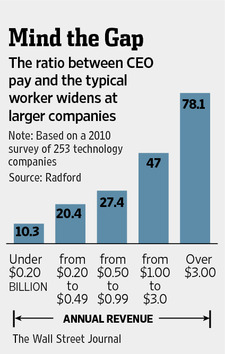

Radford, a consulting unit of Aon PLC, offered a glimpse of the complexity after Dodd-Frank passed in 2010, when it analyzed salary data for employees at 253 technology companies. The sample was drawn from more than 1,500 companies that annually tell Radford how much they are paying employees, from the executive suite to the factory floor.

Its conclusion: Bigger, more global companies would likely report significantly higher pay ratios than smaller, domestic-focused firms.

At companies with less than $200 million in annual revenue, the CEO made roughly 10 times the typical employee; at companies with more than $3 billion in annual revenue, the CEO made 78 times the typical employee. At companies with only U.S. employees, the CEO made 20 times the typical employee; at companies with global operations, the CEO made 42 times the typical employee.

“The biggest lesson we took away is that it’s going to be difficult to draw company-to-company comparisons,” said Ted Buyniski, a senior vice president for Radford.

Many companies in the analysis were in the same corners of the tech industry, often rivals of one another, but had different results. For example, Mr. Buyniski said, the ratio for the CEO of a semiconductor maker with factories in the U.S. will likely be lower than a rival with factories in East Asia.

“When you’re talking about global companies, you may be in a situation where you have two similarly paid CEOs who have dramatically different pay ratios,” he said.

The same dynamic would be evident in other industries. Yum Brands Inc., owner of Taco Bell, franchises most of its U.S. restaurants, but employs tens of thousands of workers at company-owned restaurants in China. Chipotle Mexican Grill Inc. owns its restaurants, almost all of which are in the U.S.

The SEC acknowledges that differing corporate strategies and structures may affect the ratios. In its proposal, the agency said comparing the ratio from one company to another may not be “achievable” or “justifiable,” and could lead to “potentially misleading conclusions and to unintended consequences.”

Supporters of the rule hope that highlighting the pay disparity will prompt companies to cut CEO pay, raise the pay of lower-level workers, or both. In a letter to the SEC, Sen. Robert Menendez, a New Jersey Democrat who wrote the pay provision, said investors deserve to know “whether public companies’ pay practices are fair to their average employees, especially compared to their highly compensated CEOs.”

Supporters say they don’t expect investors to compare the pay ratios of companies in different industries. Brandon Rees, acting head of the AFL-CIO’s Office of Investment, said the numbers will be more useful in comparing peers; even then, he said, comparisons might be skewed by whether a company uses its own workers or farms tasks out to subcontractors.

But Mr. Rees said the rule would prompt more disclosure about those workplace practices. “This rule will encourage the companies to better describe those differences and help investors better understand those companies,” he said.

September 21, 2013

A Better Way to Compare C.E.O. Pay

HOW much pay is too much pay? It’s a question shareholders have been asking for years.

Now the Securities and Exchange Commission has dipped its toe into the executive pay pool with a rule issued last week that would require companies to publish a comparison of their chief executives’ pay to the median compensation of most other company employees.

Unless you were born yesterday, you already know there’s a vast gulf between C.E.O. pay and that of the public company rank and file. So the rule, if it goes into effect (it is now undergoing a 60-day comment period), won’t be that revelatory. Sure, there will be noteworthy numbers. But the new rule will do little to help shareholders understand whether the executive pay awarded by their companies is appropriate and if not, how off the charts it is. A far more meaningful comparison for regulators is the peer groups public companies choose to use as benchmarks when setting their pay packages.

These peer groups, which are supposed to include similar companies, often don’t. In many cases, companies choose peers that are far larger or more complex and whose executives are paid more to manage that size and complexity. Therefore, the inclusion of these companies in a peer group can skew an executive’s pay higher. Investors have a name for such companies: aspirational peers.

Peer groups certainly are ubiquitous — in 2012, some 86 percent of companies in the Standard & Poor’s 1,500-stock index said they used them, according to Equilar, the executive compensation analytics company in Redwood City, Calif. But they can be pretty blunt instruments for comparing executive pay.

Aware of the potential for questionable choices of companies within these peer groups, institutional investors are examining them more closely. Equilar has been assisting these investors with a system that generates a separate peer group for a company. Shareholders can use Equilar’s peer groups — and the pay they provide to their executives — to vet the groups chosen by their companies.

Aeisha Mastagni, investment officer at the California State Teachers’ Retirement System, says her organization uses Equilar’s peer groups as a gut check before voting on executive pay at companies. When wide disparities emerge between a company’s peer group and the Equilar alternative, Calstrs officials have brought up the matter with company officials.

“The peer group aspect is one piece of the puzzle that we look at when we cast votes on company pay practices,” Ms. Mastagni said in an interview last week. “Far too many companies use the peer groups as a starting point when they really need to be that reasonableness check.”

Peer groups chosen by companies don’t always differ significantly from those Equilar’s system produces. But many do.

ONE is Hain Celestial Group, a food company based on Long Island whose founder and chief executive, Irwin David Simon, received $6.5 million in pay last year.

In its proxy statement, Hain discloses two different peer groups that it uses to benchmark pay. One consists of many food and beverage companies, including Chipotle Mexican Grill, Mead Johnson and United Natural Foods. Most have higher revenue than Hain’s and half have larger market capitalizations. And yet Hain’s chief executive received far more than the $3.9 million median pay for the C.E.O.’s at those larger peers.

The other peer group used by Hain consists of companies whose founders, like Mr. Simon, still run the show. This peer group is made up of 14 companies, including Costco and Starbucks. The revenues of most of those companies were significantly higher than Hain’s — Costco, for example, has $99 billion in revenue compared to $1.4 billion for Hain. Nevertheless, these peers paid their executives less — a median of $4.8 million versus Hain’s $6.5 million.

Equilar’s suggested peer group for Hain, adds two companies to Hain’s list, with median revenues that were much more in line: Post Holdings and SunOpta. This group paid their C.E.O.’s a median $2.6 million last year, far less than what Mr. Simon at Hain received.

Mary Anthes, a spokeswoman for Hain, said that its peer group was selected by its board’s compensation committee and that for the last two years Hain’s sales, earnings and stock price had been markedly higher, justifying the pay.

Kelly Services, the staffing company, provides another example. Its disclosed peer group has just two companies — ManpowerGroup and Robert Half International. Carl T. Camden, Kelly’s chief executive, received $3.3 million in pay last year. This sounds reasonable enough, given that the median pay received by the top executives at Kelly’s peers was $8.7 million.

But when you look at revenues, the peer group comparison makes less sense. Manpower’s revenue was more than three times the $5.5 billion Kelly generated last year, and the market capitalization of both peers was far in excess of Kelly’s $585 million.

As an alternative, Equilar chose a larger group — 14 companies, most of them in the employee staffing field — with median revenue of $1.24 billion and market capitalization of $775 million. In this case, Equilar’s more representative group was not so out of whack with Mr. Camden’s actual pay. The median pay dispensed to the top executives at these companies was $2.8 million, slightly below what Mr. Camden received.

Kelly Services did not respond to an e-mail seeking comment.

Equilar came up with the idea of creating alternative peer groups because its officials believed that in an age of big data, it could improve on the standard, more limited approach taken to come up with peer groups. Rather than just look at industry groups and revenues, Equilar builds relationship maps.

Equilar uses an algorithm to tap into peer group data found in S.E.C. filings and employ social media to generate what it contends are credible alternatives to company peer groups.

For example, Equilar consults all filings for mentions of peers and then matches them up. Say, for example, company A is identified as a peer by company B but A does not include B as one of its peers. Equilar feeds this information into its system. It also includes what it calls second-

degree peers — when company A lists B as a peer and B lists company C as one, Equilar will consider adding company C.

Equilar maps these ties and identifies the strongest connections among them. The result is what it calls market peers for each company.

Investors have to weigh many elements when assessing the fairness of executive pay. Peer groups are just one of those, of course. But as the Equilar examples show, some peers are more equal than others.