China Inc’s balance sheet is flashing danger signals

September 22, 2013 Leave a comment

China Inc’s balance sheet is flashing danger signals

Friday, 20 September, 2013, 12:00am

Tom Holland

Mainland’s recent lending boom has pushed corporate leverage into a potentially perilous state in terms of ratio of operating cash flow to debt

If you want to know whether a recession is coming, don’t look at the top-down macroeconomic numbers like gross domestic product. Instead, focus on the bottom-up analysis of consumer, corporate and government balance sheets. They make a far more reliable warning system. In emerging Asia, where consumer debt is generally modest and government finances relatively sound, it is corporate balance sheets that we should be looking at.Specifically, says Gillem Tulloch, managing director of Hong Kong-based independent research outfit Forensic Asia, we should pay attention to corporate leverage and solvency.

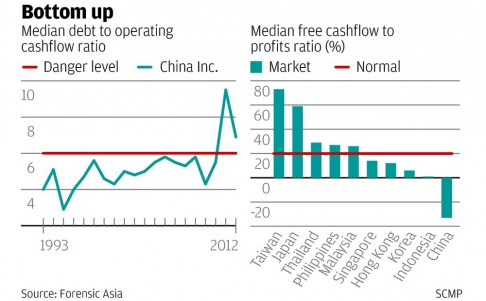

Tulloch’s preferred measure is the ratio of operating cash flow to debt. Operating cash flow he describes as “true profit”: the money a company earns from its business before splashing out on capital expenditure.

The ratio of operating cash flow to debt is important because it tells us how many years it would take a company to repay its debts if it slashed its capital expenditures to zero.

A typical healthy period is around three or four years, says Tulloch. The danger level is six years. Any number higher than that is a signal that a company’s balance sheet has become perilously bloated and that its solvency is threatened.

At that point, says Tulloch, companies stop investing in order to generate enough free cash flow – operating cash flow minus capital expenditure – to pay down their debts.

Unfortunately, if the bulk of a country’s corporate sector is overleveraged and cuts capital expenditure at the same time, growth will grind to a halt and the economy slip into recession.

There are plenty of examples from the past. For instance, in 1996 the median debt to operating cash flow ratio among listed Thai companies shot up to eight years.

That left corporate Thailand bleeding cash, with free cash outflows equal to more than 100 per cent of profits.

In the deleveraging that followed, Thailand’s economy contracted by a brutal 15 per cent in real terms.

[1]Now it looks as if China might be about to undergo a similar experience.

According to Tulloch’s analysis of China’s 1,500 biggest listed companies by sales, the lending boom of the last few years has pushed corporate leverage well into the danger zone, with the median level of debt now equal to almost seven years of operating cash flow (see the first chart).

With Chinese companies still investing, China Inc’s free cash flow has turned deeply negative (see the second chart), a situation Tulloch says is “very rare” and only seen in Asia in the run-up to the 1997 crisis.

Although it looks from his data as if corporate solvency actually improved last year, Tulloch warns against false optimism. The apparent strengthening, he says, was the result of Beijing’s latest round of credit stimulus.

Unfortunately, it’s unsustainable. “Banks can’t continue to lend at the current rate,” he says.

Meanwhile, leverage is rising and overcapacity mounting, especially in the state-owned heavy industrial sector. At the same time the state of China’s accounts receivable is deteriorating, as payment times have almost doubled from 30 to nearly 60 days.

With command of the banking system and control of China’s capital account, Beijing can postpone the reckoning for a year or two, but only at the cost of exacerbating the depth of the eventual slump.

“Recession is inevitable,” Tulloch warns. “China has to have an economic contraction to cleanse the system.”

There is silver lining to the thundercloud. As corporate capital expenditure collapses, China’s economy will automatically rebalance away from investment and towards consumer demand.

But as Thailand found in 1997, while it lasts the balance sheet deleveraging will be deeply unpleasant.