Unlocking New Sources of Value Creation

September 29, 2013 Leave a comment

Unlocking New Sources of Value Creation

by Gerry Hansell, Jeff Kotzen, Eric Olsen, Frank Plaschke, and Hady Farag

SEPTEMBER 17, 2013

Unlocking New Sources of Value Creation is the fifteenth annual report in the Value Creators series published by The Boston Consulting Group. Each year, we offer commentary on trends in the global economy and world capital markets, share BCG’s latest research and thinking on value creation, describe our experiences working with clients to materially improve their value-creation performance, and publish detailed empirical rankings of the performance of the world’s top value creators. This year’s report offers four different perspectives on successful value creation. We begin by analyzing the recent disconnect between uneven global economic growth and buoyant global equity markets. Next, we describe how senior executives can use value patterns, a concept we introduced in last year’s report, to identify the most appropriate “unlocks” to create new value. We follow with a detailed case study of how one BCG client, the branded apparel company VF, has used a focus on total shareholder return to transform the company’s business, accelerate its growth to the point that today it is the world’s largest apparel company, and deliver shareholder value at the top end of its peer group. Finally, we conclude with our annual rankings of the top ten value creators worldwide and in 25 industries for the five-year period from 2008 through 2012.

The Great Disconnect

The Great Disconnect

Think of it as “the great disconnect.” Global economic growth continues to be slow and highly uneven. And yet, over the past 18 months, global equity markets have seen their most consistent expansion since the financial crisis of 2008. In 2012, the total shareholder return (TSR) of the MSCI All Country World Investable Market Index was approximately 16.5 percent. For the first half of 2013, it was 9.8 percent.

What are the implications of this disconnect between economic performance and market performance for how companies should approach value creation in the years to come? That is the focus of this year’s Value Creators report.

Uneven Economic Growth

To be sure, some of the recent market gains reflect real improvements in global economic growth. Earlier this year, we pointed out that the relatively strong performance of traditional economic engines—such as automobiles and parts, household goods and home construction, construction and materials, and general industrials—in 2012 werehopeful signs (https://www.bcgperspectives.com/content/articles/value_creation_strategy_signs_of_sustainable_value_creation/) that global economic recovery was becoming more sustainable. Rapid growth has continued in some emerging markets. And there has been slow but increasingly steady growth in the U.S. and Japan, with the two countries achieving annualized first-quarter growth of 2.5 percent and 2.8 percent, respectively, in 2013. This growth is finally having a material impact on unemployment. In the U.S., for example, the unemployment rate dropped from 10 percent in October 2009 to 7.6 percent in May 2013.

But the improvement in global economic performance has been highly uneven. At the same time that the U.S. and Japan have been doing somewhat better, Europe has been mired in recession. In annualized terms, the Eurozone economy contracted by about 0.8 percent in the first quarter of 2013. And although emerging markets are on track to grow about 5 percent in 2013, that is the slowest expansion in a decade, except for that of the post-financial-crisis economy of 2009.

The Impact of Central Bank Policies

Far more important to recent market gains have been the monetary policies adopted by the world’s central banks in an effort to boost economic growth. Central banks have kept interest rates low in order to encourage borrowing and investment, and low interest rates have driven down yields on financial assets such as bonds. With interest rates on risk-free government bonds approaching zero, equities have become a relatively more attractive asset class, driving stock prices higher. We estimate that improvements in valuation multiples alone accounted for roughly 13 to 14 percentage points of the average TSR of 16.5 percent in 2012.

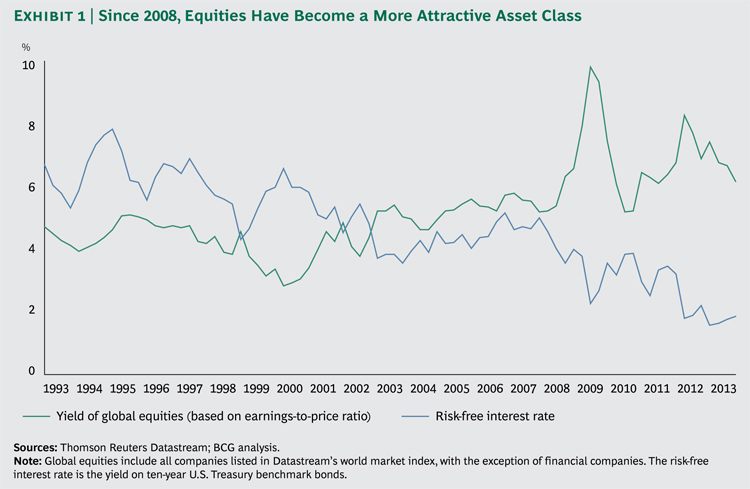

Exhibit 1 puts this phenomenon into historical context. The graph compares the quarter-by-quarter yield of equities (the ratio of earnings to price) with that of the U.S. Treasury’s benchmark ten-year bond from the first quarter of 1993 through the second quarter of 2013. It shows that for much of this period, the yields of these two asset classes remained close to each other. But since the 2008 financial crisis, the spread between the two has grown roughly threefold, making equities a far more attractive asset class, relatively speaking.

Room to Rise?

Exhibit 1 would also seem to suggest that there is considerable room to extend recent equity-market gains. On an absolute basis, earnings-to-price yields on equities remain considerably higher than those that prevailed in the 15 years preceding the 2008 financial crisis, which implies that price-to-earnings (P/E) multiples are below precrisis norms.

What’s more, there are other, longer-term trends that may support the movement of cash into equities. One such trend is the coming retirement of the baby boom generation(https://www.bcgperspectives.com/content/articles/value_creation_strategy_corporate_strategy_portfolio_management_value_creation_in_volatile_economy/). Although this demographic transition will eventually lead to the withdrawal of massive amounts of cash from the equity markets, the impact is likely to be more positive in the next five to ten years. Baby boomers have accumulated a great deal of wealth and as they age they will be looking for places to invest that wealth in order to provide income and preserve capital. These goals will reinforce the market for companies that deliver low risk combined with attractive capital gains or high dividends (or both).

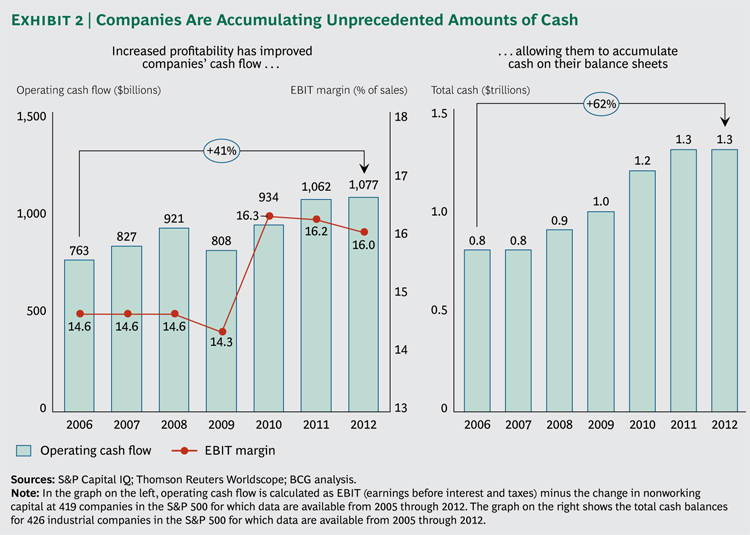

Another potential upside for equity markets (or, at least, a floor under stock prices) is the unprecedented amounts of cash that companies are accumulating on their balance sheets. Exhibit 2 shows that one result of the financial crisis and downturn has been a step function improvement in company profit margins—leading to a growth in operating cash flow. As a result, U.S. companies are sitting on the largest cash pile in history—approximately $1.3 trillion for the 426 industrial companies in the S&P 500 for which there are continuous data for the period from 2000 through 2012, which represents about 6 percent of the entire $22 trillion value of the U.S. equity market.

These enormous cash balances can be a potential problem but also a potential solution. At current low interest rates, this cash is unlikely to be valued fully by investors. What’s more, it represents a tempting target for those looking for ways to get their hands on more cash—whether governments (in the form of higher taxes) or activist investors (in the form of corporate breakups or takeovers). However, if companies start actively deploying this cash—either by investing in new opportunities for profitable growth or by returning it to investors in the form of share buybacks or increased dividends—these cash balances could further boost stock prices and overall TSR. (See “The Components of TSR.”)

The Components of TSR

Total shareholder return is the product of multiple factors. Regular readers of the Value Creators report should be familiar with BCG’s model for quantifying the relative contribution of the various sources of TSR. (See the exhibit below.) The model uses a combination of revenue (that is, sales) growth and change in margins as an indicator of a company’s improvement in fundamental value. It then uses the change in the company’s valuation multiple to determine the impact of investor expectations on TSR. Together, these two factors determine the change in a company’s market capitalization and the capital gain (or loss) to investors. Finally, the model tracks the distribution of free cash flow to investors and debt holders in the form of dividends, share repurchases, or repayments of debt in order to determine the contribution of free-cash-flow payouts to a company’s TSR.

The important thing to remember is that these factors all interact with each other—sometimes in unexpected ways. A company may grow its revenue through an EPS-accretive acquisition and yet not create any TSR, because the new acquisition has the effect of eroding the company’s gross margins. And some forms of cash contribution (for example, dividends) have a more positive impact on a company’s valuation multiple than others (for example, share buybacks). Because of these interactions, we recommend that companies take a holistic approach to value creation strategy.

Of course, all bets are off should interest rates rise. A comment by U.S. Federal Reserve chairman, Ben Bernanke, on May 21, 2013, that the Fed might consider paring back its monthly $85 billion purchases of bonds in the near future was enough to trigger a decline in the S&P 500 of 4 percent over the next three weeks. As of August 2013, global equity markets had regained some of the volatility that had been largely absent during the previous 18 months.

The Need to Step Out from the Pack

No one knows precisely how long the current expansionary equity-market environment will last. As companies devise their value-creation strategies, it is critical to keep four things in mind:

Just as important as a company’s absolute TSR is its relative TSR compared with its peer group. And just as today’s buoyant market is affecting the TSR of nearly all companies, so will any flattening or decline in equity values once the current central-bank policies are unwound. Executives should neither take the recent increases in valuations for granted nor be paralyzed by any forthcoming decline. Instead they should focus their energy on developing a clear investment thesis for how they will allocate capital in the future in order to create value.

Similarly, whatever happens to valuation multiples on average, the real name of the game is how one company’s multiple compares with the multiples of its peers. In order to have a relative valuation advantage, companies need to know what drives the differences among multiples in their peer group. Take the example of debt. Low interest rates may encourage a company to take on more debt. But in some sectors, excess debt has a demonstrated negative impact on relative multiples.

All things being equal, sustainable earnings growth is the key to long-term value creation. But all things are never equal, and investments to drive earnings growth often end up destroying value. Other actions—raising margins, reducing risk, allocating capital differently, restructuring the portfolio—may be more relevant, depending on the company’s opportunity set and starting position. Most companies will need concrete strategies for increasing their top-line revenues at least as fast as their peers over time. But whether a company is in a position to create value primarily through growth depends entirely on its starting position and the relative health of its business.

In an environment of easy capital and buoyant valuations, companies will be tempted to throw money at problems or to “buy growth” (for example, by overpaying for acquisitions). It is a big mistake. They need to be disciplined about capital deployment.