Investors have lost billions on Australian toll roads and tunnels but that isn’t stopping others from following in their path

October 2, 2013 Leave a comment

Oct 1, 2013

Australian Toll Roads, Tunnels Offer Divergent Paths for Investors

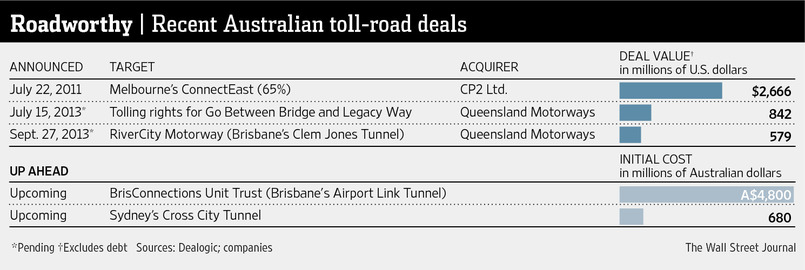

SYDNEY—While some investors have found that Australian toll roads amount to expensive wrong turns, others are choosing to follow them. Investors have collectively lost billions of dollars on the toll roads and tunnels in recent years because of too much debt and overestimates on traffic volume. Now, sharply lower prices for those assets and more-realistic traffic assessments are adding up to opportunities for others.Consider last week’s sale of the lease on Clem Jones Tunnel, a key artery in Queensland’s state capital, Brisbane. It was put up for sale this year after its leaseholder failed to meet debt obligations. The tunnel attracted four bidders, with some consortium members from as far away as Europe.

Queensland Motorways Group, owned by Australian investment manager QIC Ltd., said last week it had acquired the lease on the tunnel from the Brisbane City Council through 2051. The price: US$579 million—less than half the amount of debt the previous leaseholder accrued on the project and a fraction of the original construction cost of 3 billion Australian dollars (US$2.81 billion).

“Toll roads can be really safe assets, because road traffic volumes never go backwards. If you take conservative growth numbers, they can be highly appropriate for Australian and global pension funds,” said Tom Snow, a partner in Access Capital Advisers, which bid on Clem Jones Tunnel as part of a consortium with Dutch pension fund manager APG and Macquarie Infrastructure and Real Assets.

The Cross City Tunnel in Sydney is on the block after a debt default last month, while the leaseholder on Brisbane’s A$4.8 billion Airport Link, is in receivership.

Still, traffic volumes are slowly rising, improving the prospects for profitability. In fact, despite the failures, some investors are finding that the toll roads and tunnels offer low-risk, high-yield opportunities.

Access Capital, which specializes in infrastructure, believes assets such as toll roads can deliver returns in excess of 11% using a low level of debt, Mr. Snow said. “On some assets, debt is highly valuable but in this case, it didn’t add much, which is why we went for an all-equity-funded bid [for the Clem Jones Tunnel],” he said.

Queensland Motorways financed its acquisition of the marked-down Clem Jones with debt of A$247 million—less than one-fifth of the debt that the previous leaseholders had accumulated. Three Australian banks backed Queensland Motorways’ bid, Chief Executive Brendan Bourke said.

Existing debtholders will receive perhaps 45 cents on the dollar from the recent sale of the long-term lease.

Even using some debt, the completed assets likely carry less risk than previously, said Michael Siede, a director at Ironstone Capital, which advised a consortium led by an infrastructure fund managed by UBS Global Asset Management in bidding for the Clem Jones Tunnel.

“Financing existing toll roads is much lower risk than greenfield toll roads and current financing structures are more conservative,” Mr. Siede said. Greenfield toll roads are new and have no operating history.

If interest in Clem Jones Tunnel is any indication, Sydney’s Cross City Tunnel and Brisbane’s Airport Link are likely to attract a line of bidders. Mr. Bourke said Queensland Motorways could be among them.

Airport Link “does fit neatly within our goal to have an integrated road network in Brisbane,” he said.