Because the results of China’s local government debt audit just can’t come fast enough

October 3, 2013 Leave a comment

Because the results of China’s local government debt audit just can’t come fast enough

| Oct 02 11:15 | 2 comments | Share

SIV/ LGFV/ LGIV/ *shrug*

Whatever you choose to call the vehicles China’s local governments used to fund infrastructure when Beijing restricted financing (we are going with LGFVs here) they are very near the centre of Chinese debt fears. Which means it’d be nice to know how big they really are. From Stephen Green at Standard Chartered (our emphasis): The National Audit Office (NAO) is now carrying out a survey of local government debt. Thousands of officials have been running around the country trying to generate accurate estimates of liabilities at the four levels of local government, down to the township level. At least 10,000 separate legal entities carry this debt burden (some large cities have hundreds of such vehicles), and many have an interest in disguising their liabilities. In addition, a portion of the debt is in the form of inter-company loans and IOUs. The auditors have an extremely challenging task.Expectations that the auditors will report a large number were first raised by comments from Zhao Quantou, a research academic at a MoF-sponsored think tank, who publicly wondered in early September if the total might be around CNY 18-20tn. Xia Bin, a senior economist formerly with the Development and Research Centre of the State Council, said publicly that the number might be “astonishing”. Last week, Economic Information, a newspaper, reported a senior NAO official postulating that the number could be CNY 22tn.

The audit results are likely to be out in October, just before the Party’s Third Plenum meeting in November. The timing is interesting. At the least, getting the bad news out in the open at the start of his term is clearly in the interest of new Finance Minister Lou Jiwei. And releasing a larger debt figure could help the MoF garner high-level support for a big fiscal reform package, and approval for sterner measures to get LGIVs under control.

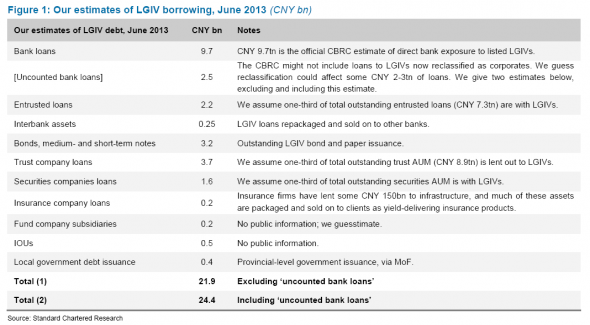

Data on LGFVs is hard-ish to come by — as Green says, there are at least 10,800 LGFVs, but the market only has financial statements for the 800-900 that have publicly issued debt, and these are the ones with better financials. And even in this privileged few, most are barely cash-flow positive, and any assets they hold (usually land) are illiquid — more on that below.

A relative lack of data doesn’t stop some useful estimates being made. StanChart have total debt at some CNY24bn:

Nomura’s Zhiwei Zhang and team have a reasonably similar estimate (in what looks a thorough report aiming to provide some much needed clarity on the LGFVs and their wider import, more of which is in the usual place):

We estimate total LGFV debt at the end of 2012 was RMB19.0trn (37% of GDP), which included RMB14.3trn of interest-bearing debt. In the period 2010-12, LGFV debt rose by 39%, which implies total government debt of RMB31.7trn, or 61% of GDP at end-2012.

So, we have an estimate of size. But what about risk? Nomura suggest that without local government support to LGFVs, over half of LGFV debt would have been at risk of default in 2012. They also estimate that in the case of a liquidity crisis, 70 per cent would be in real trouble with a government hug.

As mentioned, even the healthier LGFVs are barely cash-flow-positive, and any assets they hold (usually land) are illiquid. From Nomura again on the worsening climate:

Liquidity conditions are tight and worsening. Demand for funding continues to grow, yet profitability and operating cash flows fell sharply in 2012. 35% of LGFVs experienced net operating cash outflows and hence have to rely on new borrowing to finance existing investment activities.

Solvency for many LGFVs depends on asset injections from local governments and debt restructuring. Many assets injected are illiquid and hence would be of little help in a liquidity crisis.

LGFV debt is sensitive to an interest rate shock. Our stress tests find that if interest rates rise by 100bp, an additional 10.4% of LGFV debt would become non-sustainable.

Systemic risks are rising quickly. With government revenues under pressure, interest rates rising and local government land revenues facing uncertainty due to an unsustainable property boom, the number of LGFV credit rating downgrades has risen recently. Moreover, the continued practice of using land and property as collateral is questionable. These factors will likely exacerbate LGFV debt conditions in 2014.

Macro conditions will deteriorate if the current pace of LGFV debt build-up continues. LGFV debt will rise to 54% of GDP in 2018 if the current pace of growth is maintained, taking total government debt to over 80% of GDP. The efficacy of this debt-driven investment strategy will dwindle as funds raised are increasingly used to service existing debt over new investment.

As widely touted reform, alongside the audit, is on the cards. Recent policy announcements about “major change in the regulatory policies on land” in Jiangsu — the rapid growth of LGFV debt is to a large extent due to the significant asset injection from local governments to LGFVs in the form of land — suggest the drive is serious.

But do please remember the whack-a-mole of nature of finance… everywhere. It’s that problem which means Green sees solving the moral hazard problem as the ultimate end game. Essentially a default or two for the good of the system is needed:

The bottom line: interest rate reform will not work unless moral hazard is reduced. If lenders believe they will always be repaid, interest rates will not work. New institutions are channelling credit to LGIVs on the basis of local government guarantees that are extremely weak in reality. The more stressed the borrowers, the more likely they are to engage in irresponsible borrowing.

No city mayor wants to be the first to announce that his LGIV is unable to repay its obligations. Unfortunately, without an LGIV having a serious problem repaying its loans, the moral hazard problem will remain, and lending to LGIVs without due attention to risk will continue. To end the moral hazard problem, we believe an LGIV default in the bond market is needed.

The assumption, for now, is that something more systemic isn’t on the cards.