Betting on a U.S.-Debt Doomsday: Budget Showdown Has Traders Crowding Into Derivatives That Pay Off if the Federal Government Defaults

October 5, 2013 Leave a comment

October 4, 2013, 7:10 p.m. ET

Betting on a U.S.-Debt Doomsday

Budget Showdown Has Traders Crowding Into Derivatives That Pay Off if the Federal Government Defaults

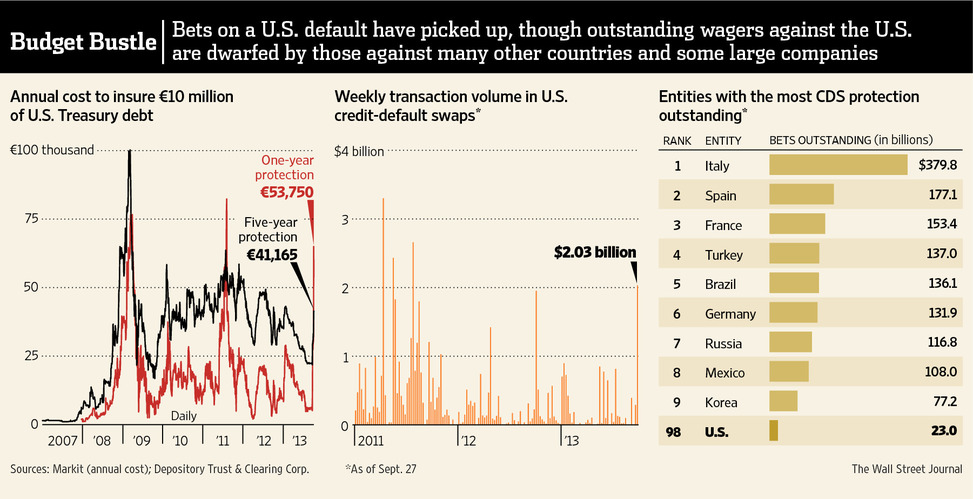

Washington’s budget showdown has sent traders and analysts crowding into a cobwebbed corner of the financial world, the market for derivatives that pay off if the federal government defaults on its debt. The cost of insuring against a U.S. default via credit-default swaps has risen sharply over the past two weeks. Volume has ticked up as well, though trading remains sparse and the number of bets against the U.S. pales in comparison to other large nations and companies.Traders on Friday were asking about €41,165 ($56,060) annually to cover €10 million of U.S. Treasurys for five years, according to data provider Markit, and €53,750 to cover the same amount of debt for one year. Two weeks ago, five-year protection cost €21,831 annually and one-year protection cost just €5,126.

The price run-up underscores some traders’ effort to protect themselves against so-called tail risk, an event that is perceived as highly unlikely but stands to be very costly if it comes to pass. Some traders are seeking to profit from the protection becoming more valuable as the logjam drags on.

“No one really believes [a U.S. default] will happen,” said Gennaro Pucci, chief investment officer at $250 million London-based hedge fund PVE Capital LLP, who isn’t buying or selling U.S. credit-default swaps.

Enlarge Image

European Pressphoto Agency

Volkswagen ranks 47th among global companies and sovereign-debtissuers, with $34.3 billion of credit-default swaps outstanding at Sept. 27

The last time one-year insurance was more expensive than five-year coverage was in mid-2011, when questions surfaced about whether the U.S. government was at risk of running out of cash.

U.S. CDS are bought and sold in euros, primarily in London, because buying protection in dollars would expose traders to the risk the dollar will fall in value—an event many view as likely in the event of a default. Accordingly, sovereign CDS on European countries are traded in dollars rather than euros.

The net sum due buyers of CDS in the event of a U.S. default rose to $3.4 billion last month from $3.2 billion at the end of August, according to Depository Trust & Clearing Corp. The gross sum of wagers against the U.S. increased $2 billion in the latest week ended Sept. 27, the most since July 2011.

Even so, bets against the U.S. barely rate a mention in the $25 trillion market for wagers against companies and sovereign-debt issuers.

The outstanding volume of U.S. credit-default swaps rank 98th at $23 billion—behind numerous European nations led by Italy, many of the globe’s largest banks and a handful of large nonfinancial companies such as Volkswagen AG VOW.XE +0.49%and Computer Sciences Corp.

Foreign banks such as Barclays BARC.LN -0.60% PLC, BNP Paribas SA, Deutsche Bank AG and Nomura Holdings Inc. 8604.TO -2.00% are the primary banks quoting prices in U.S. CDS, traders said.

Many orders are from small funds seeking to hedge their Treasury portfolios. Larger institutions often don’t buy U.S. CDS, traders said, because their portfolios of Treasury seurities are so large that they would need so much protection, weighing down the returns.

In a default, CDS holders would receive make-whole payments from CDS sellers. The recovery is determined by the lowest-priced bond of the issuer underlying the CDS.

For the U.S., that is currently a Treasury bond due in August 2042 that trades at 82 cents on the dollar, yielding U.S. CDS holders a hypothetical 18-cent payout.

The U.S. government would have three business days to make up a missed payment before any payouts would be triggered.

Some investors, however, caution that a U.S. default would send stock and bond markets reeling, potentially making it hard to collect.

PVE Capital’s Mr. Pucci said he was taking the opportunity to buy risky assets when markets tumble during the Washington standoff.

If the Treasury does fail to make timely payments, Mr. Pucci said, the market reaction could be so swift and unruly that “the last thing you would worry about is how you invest your money.”