In Latest IPOs, Profits Aren’t the Point; Two-Thirds of U.S.-Listed Tech Debuts in 2013 Lost Money

October 11, 2013 Leave a comment

In Latest IPOs, Profits Aren’t the Point

Two-Thirds of U.S.-Listed Tech Debuts in 2013 Lost Money

TELIS DEMOS

Oct. 10, 2013 7:07 p.m. ET

No profits? No problem. Investors are showing increasing hunger for initial public offerings of unprofitable technology companies and the potential for big gains that they bring. Sixty-eight percent of U.S.-listed technology debuts this year, or 19 out of 28 deals, have been companies that lost money in the prior fiscal year or past 12 months, according to Jay Ritter , professor of finance at the University of Florida. That is the highest percentage since 2007, and 2001 before that.The excitement over companies’ potential rather than their present results is the latest sign in the stock markets of a rising tolerance for risk. The U.S. IPO market, often seen as a gauge of risk appetite because the stocks don’t have a track record, is on pace to produce the most deals since 2007, according to Dealogic.

Twitter Inc. is expected to join the parade of unprofitable companies selling shares, with a public offering expected this year. While hardly a startup—”tweeting” began in 2006—Twitter didn’t turn a profit last year, even as its microblogging service rose to more than 215 million monthly active users and has challenged traditional media for audience. Its IPO documents show a $79 million loss for 2012, on revenue of $317 million.

A Twitter spokesman declined to comment.

The piqued interest in earlier-stage technology IPOs in particular has raised concerns that IPO investors are turning a blind eye to the possibility that business plans don’t pan out.

“IPOs can have a place in someone’s portfolio if you’re willing to be a trader,” said Robert Pavlik , chief market strategist at Banyan Partners, an investment manager that advises on $4 billion in assets. “But if you want to be a long-term investor, don’t treat the stock market as another kind of Las Vegas.”

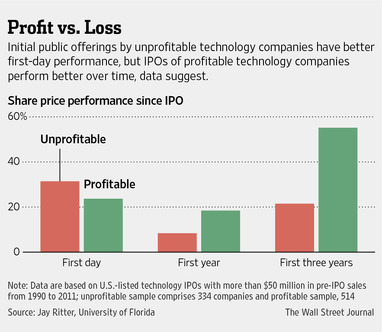

Data suggest that sticking to companies that already are producing income can be a better bet. Unprofitable U.S.-listed technology companies that went public from 1990 to 2011 returned an average of 21.5% in their first three years, while profitable companies returned an average of 55.2% in that period, according to research by Mr. Ritter on companies with more than $50 million in revenues.

The returns are based on performance after a stock’s first day of trading. His data also show that both groups outperformed the broader market in those periods.

In the dot-com boom years of 1999 and 2000, when many investors lost money after snapping up highflying shares, 86% of tech IPOs were of companies that lost money.

At the same time, when it comes to public offerings, some investors aren’t focused on averages. They are looking for home runs. Profitability even can be seen as a negative because it sometimes suggests maturity.

Some investors “want a lottery ticket on a company disrupting a very, very large market,” said Paul Deninger, senior managing director in the technology group at investment bank Evercore Group LLC. “For that, they’re willing to sacrifice profit for growth.”

That sentiment prevailed in the dot-com era. But one feature sets the latest batch of unprofitable companies apart: hefty revenues. More than 85% of the tech companies going public in the U.S. this year had annual revenues over $50 million, versus an average of 22% of tech IPOs in 1999 and 2000 on an inflation-adjusted basis, according to Mr. Ritter.

Pets.com Inc., for example, went public with sales of just $5.8 million in the three quarters before its 2000 IPO. Pets.com’s shares priced at $11 and were trading at less than $1 when the company closed later that year.

In contrast, Splunk Inc., a data-analysis software company, lost $11 million in the fiscal year before its IPO in April 2012, but had total revenues of $121 million. Its shares are up 248% since its debut.

Still, some maintain it is just too difficult, and too risky, to value a company that doesn’t have earnings.

“You should be more wary of these IPOs. They say the scariest words in the market are ‘this time is different,'” said Lance Roberts, chief strategist for STA Wealth Management, an investment adviser based in Houston, Texas. He suggests investors wait to see how a stock performs and how the fundamentals look before buying an unproven concept.

Facebook Inc. FB +4.87% already was generating $3.7 billion in annual revenues and $1 billion in net income when it went public in May 2012. In the months after the IPO, Facebook shares dropped as much as 50% from their offering price, partly because investors worried that the company wouldn’t be able to adequately boost advertising revenue amid a user shift to mobile devices.

Yet Facebook shares have risen 85% since mid-July, when the company reported better-than-expected mobile-advertising revenue.

Twitter produced positive cash flow from its operations of $10 million in the first six months of 2013, a measure of money being generated by the business that doesn’t include accounting adjustments. Its net loss for the period was $69 million.

Twitter may be about four years behind Facebook in terms of generating revenue and profit from users, according to analysts who have reviewed its IPO filing.

This means it might be more apt to compare Twitter to Facebook four years before its IPO. In 2008, Facebook had net losses of $56 million on revenues of $272 million.