Debt Markets Don’t Drink from Stocks’ Half-Full Glass; Stocks Have Jumped on Debt-Deal Hopes, but Funding Markets Are on the Edge of Their Seat

October 14, 2013 Leave a comment

October 11, 2013, 5:14 p.m. ET

Debt Markets Don’t Drink from Stocks’ Half-Full Glass

Stocks Have Jumped on Debt-Deal Hopes, but Funding Markets Are on the Edge of Their Seat

While stock markets have jumped for joy over a possible debt-ceiling deal, short-term funding markets are still on the edge of their seat. Signs of a thaw in Washington’s budget standoff have sent the stock market into paroxysms of joy. But with the clock still ticking on the U.S. hitting its debt ceiling, short-term credit markets remain wary. Until an actual deal is struck, they could get warier still.Since it first emerged that House Republican leaders were hashing out a plan to temporarily extend the country’s borrowing limit, stocks have shot sharply higher. But the yield on the one-month Treasury bill remains elevated. At 0.25% Friday, it was only slightly below the 0.28% it marked Wednesday and well above the 0.03% it carried Sept. 30, the day before the government shutdown began.

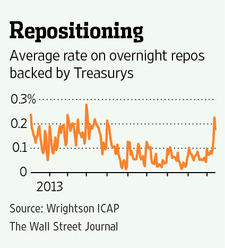

The repurchase, or repo, market, where banks, money-market funds and corporations make short-term loans backed by Treasurys and other government securities, is also showing signs of stress. The average rate on overnight Treasury repos executed by Wrightson ICAP on Friday was 0.17%. Outside of Thursday’s 0.23%, that was the highest since early May.

The Treasury says the debt ceiling will likely get hit around Oct. 17. Budget deals have lately come right down to the wire, points out Stan Collender, a budget expert at public-affairs firm Qorvis. And since everybody in Washington knows the Treasury will have enough cash on hand to keep making payments for a week or two after the ceiling is reached, there is a good chance a deal might not be struck until after next week.

If a deal doesn’t come in time, the consequences would be beyond serious. Short-term Treasurys, among the most liquid instruments in the world because they are so easily converted into cash, would be among the first in line for default.

That would suddenly make them less liquid, prompting lenders to charge significantly higher rates for short-term credit amid a general run for cash. Since short-term funding is crucial for everyone from brokers making markets in securities to companies looking to finance inventory, the economy would be in for a sudden lurch.

It is because the default scenario is so bleak that many investors are so completely convinced a default can’t happen. That is why the debt-ceiling debate has weighed so lightly on the stock market in recent weeks, and shed what weight there was over the past two days on optimism over a deal.

Money-market funds and other participants in the short-term debt markets can’t be so sanguine—especially at a time when overall rates are so low that the payoff for betting against a default is tiny. Instead, every day that goes by without a deal, they have to take more precautionary steps in case a deal doesn’t happen.

Those steps could add up to the point where the stock market notices. It ain’t over yet