Europe’s Flawed Growth Strategy; Reliance on Exports Isn’t a Sustainable Approach

October 24, 2013 Leave a comment

Europe’s Flawed Growth Strategy

Reliance on Exports Isn’t a Sustainable Approach

DAVID WESSEL

Updated Oct. 23, 2013 1:40 p.m. ET

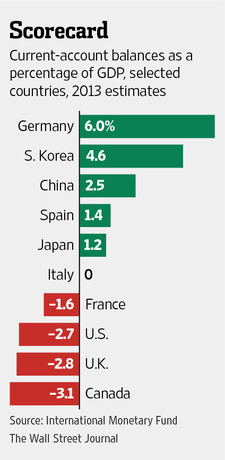

Now that Washington has reopened the government and averted potential default, the global spotlight will shift back to the euro zone. Europe has a way of making the U.S. economy look good. In the U.S., the unemployment rate is a still-high 7.2%. In the 17 countries that share the euro, it’s 12%, ranging from 5.2% in Germany to 26.2% in Spain. Neither the U.S. nor Europe has a compelling strategy to boost the slow pace of economic growth. But Europe in particular has stumbled onto a short-term approach that can’t last: Make the rest of Europe more like frugal Germany, relying heavily on exports rather than on domestic consumer spending and business investment.But not every economy can be a net seller to the rest of the world; someone has to be the buyer. For a long time, it was the borrow-and-spend U.S. consumer. That chapter is closing.

The euro zone was created for several reasons, not all economic. A big one was the fervent desire of European wise men to bind Germany and France together so they’d never again go to war. One economic argument was to meld national economies into a “single market” resembling the U.S., a big economy that makes most of what it consumes and consumes most of what it makes and, thus, is a little less vulnerable to the ups and downs of the rest of the world.

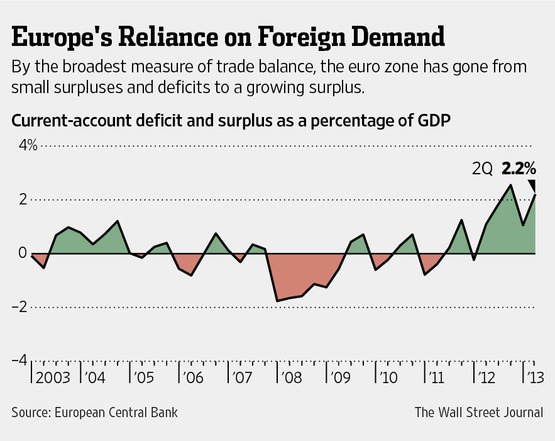

For a time, the euro zone as a whole seemed to be pulling it off. Its trade with the rest of the world was roughly in balance, sometimes a small surplus, sometimes a small deficit. Internally, it was a different story: Germany exported a lot and lent money mainly to Southern Europe, which imported a lot.

Wessel: Yellen’s Challenge: Finding a Safe Exit

Seib: Shutdown’s Biggest Toll: Less Confident Consumers

Obama’s Shrinking Second-Term Plans

The global financial crisis ended that: Spain, Italy, Greece, Portugal and Ireland couldn’t keep borrowing, which meant they couldn’t keep importing. They were told to get more competitive—to increase productivity, or output per hour of work, and reduce wages and prices to make their exports more attractive.

To some extent the weaker economies took the advice. Spain’s central bank says the country eked out quarter-over-quarter growth of 0.1% in the third quarter, marking the end of two years of recession. Domestic demand accounted for minus 0.3 percentage point and exports for a positive 0.4 percentage point. Exports are running 6.6% ahead of last year.

“This approach is full of risk,” says Paul de Grauwe of the London School of Economics. “You want to improve your competitive position by reducing wages. That will improve your competitiveness but it takes a while and by reducing wages, you reduce purchasing power and domestic consumption.”

What’s more, much of the increase in Spain’s exports isn’t to Europe. “External demand from the rest of the world has so far been the main driver of export performance,” the International Monetary Fund notes. It estimates that between 40% and 50% of the upturn in exports from Germany and Spain since late 2008 came from outside the euro zone; for Portugal, all of it was from outside the euro zone.

As a result, the euro zone’s trade surplus with the rest of the world has gone from 0.8% of gross domestic product in 2011 to 1.3% in 2012 to 2.2% in the second quarter of 2013. Much of this is the inevitable consequence of Europe’s lousy economy: When people buy less, their countries import less.

Exporting more outside Europe is certainly better than not exporting at all. But it isn’t sustainable. The slowdown in some big emerging markets, including China, and the tepid pace of growth in the U.S. surely will constrain Europe’s export growth at some point.

If Spain, Portugal, Italy and others are to export more, someone in Europe has to import more. With its usual delicacy, the IMF has lectured Europe on this point: “Stronger domestic demand in surplus economies”—that means you, Germany—”is critical to support stronger demand in the euro area as a whole and help sustain a rebound in exports from deficit economies.”

Germany, suffering a public and private investment drought, can borrow at a 1.8% rate these days on its 10-year government bonds to invest more in infrastructure, energy, whatever, thus increasing demand in Europe. Those investments surely would yield a return better than 1.8%, but, Mr. de Grauwe says, “the German fear of debt in this case is irrational.”

The rising euro, now at its highest level in nearly two years, is a threat, as well. It makes European wares more costly outside the euro zone. But a rising euro doesn’t make Spanish olives, auto parts or hotels more costly to Germans—if only they were buying.

Without a shift in strategy, Europe is dooming itself to a decade or more of stagnation.