J.P. Morgan’s Subprime Troubles Ran Deep

October 28, 2013 Leave a comment

J.P. Morgan’s Mortgage Troubles Ran Deep

Deals With Subprime Lenders at Heart of $5.1 Billion Settlement

AL YOON

Oct. 27, 2013 6:24 p.m. ET

A 1,625-square-foot bungalow at 51 Perthshire Lane in Palm Coast, Fla., is among the thousands of homes at the heart of J.P. Morgan Chase JPM +0.55% & Co.’s $5.1 billion settlement with a federal housing regulator on Friday. In 2006, J.P. Morgan bought one of two mortgage loans on the home made by subprime lender New Century Financial Corp. J.P. Morgan then bundled the loan with 4,208 others from New Century into a mortgage-backed security it sold to investors including housing-finance giantFreddie Mac. FMCC +11.89%By the end of 2007, the borrower had stopped paying back the loan, setting off yearslong delinquency and foreclosure proceedings that halted income to the investors, according to BlackBox Logic LLC, a mortgage-data company.

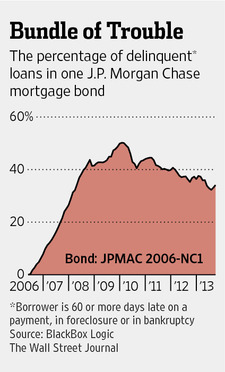

The Palm Coast loan wasn’t the only troubled one in the New Century deal: Within a year, 15% of the borrowers were delinquent—more than 60 days late on a payment, in some stage of foreclosure or in bankruptcy—according to BlackBox. By 2010, that number exceeded 50%.

“That’s much worse than anyone’s expectations when the deal was put together,” said Cory Lambert, an analyst at BlackBox and former mortgage-bond trader. “It’s all pretty bad.”

J.P. Morgan sidestepped many of the subprime-mortgage problems that bedeviled rivals during the financial crisis, and avoided much of the postcrisis scrutiny that dragged down others on Wall Street. But now its own behavior during the housing boom is coming under close examination as investigators work through a backlog of cases.

The bank dealt with some of the biggest subprime lenders of the time, including Countrywide Financial Corp., Fremont Investment & Loan and WMC Mortgage Corp., a former unit of General Electric, according to the Federal Housing Finance Agency complaint.

J.P. Morgan’s relationship with New Century, a subprime lender that went bankrupt in 2007 and later faced a Securities and Exchange Commission investigation and shareholder suits, shows that the New York bank was part of the frenzied push to package mortgages for investors at the end of the housing boom.

The New Century deal, J.P. Morgan Mortgage Acquisition Trust 2006-NC1, was one of 103 cited in the lawsuit against J.P. Morgan brought by the FHFA, which oversees Freddie Mac and home-loan giant Fannie Mae. FNMA +13.40%

The $5.1 billion settlement is part of a larger tentative deal with the Justice Department and other agencies that would have J.P. Morgan pay a total of $13 billion. That deal is expected to be completed this week.

“While these settlements seem huge, given the nature of the offenses, they are trivially small,” said William Frey, chief executive of Greenwich Financial Services LLC, a broker-dealer that has participated in investor lawsuits against banks that packaged mortgages. J.P. Morgan declined to comment on the settlement or any loans in the bonds it bought.

The FHFA has gotten aggressive in recouping losses from mortgages and securities sold to Fannie and Freddie. In 2011 it sued 18 lenders, and J.P. Morgan was only the fourth to settle.

To be sure, the New Century deal was among J.P. Morgan’s worst performers, and other mortgage-backed securities it issued at the time have held up better. An improving economy and housing market have lifted many mortgage bonds sold in 2006 and 2007.

But that is of little consolation to Freddie Mac, which bought more than a third of the $910 million New Century bond deal in 2006 and still is sitting on losses.

The group of loans backing Freddie’s chunk of the deal had more high-risk loans than the rest of the pool. Nearly 44% of Freddie’s piece had loan-to-value ratios between 80% and 100%, compared with 31% for the rest, according to the deal prospectus.

What’s more, nearly half the loans backing the New Century deal were from California and Florida, two states hit hard by the housing bust. Of the 4,209 loans in the bond, more than half have some experienced distress, according to BlackBox data.

Three debt-rating firms gave the top slice of the deal AAA ratings. But as the housing market soured, a series of downgrades starting in 2007 took them all into “junk” territory by July 2011. As of last month, nearly a quarter of the principal of the underlying loans in the deal had been wiped out, with a third of the remaining balance delinquent or in some stage of foreclosure, according to BlackBox.

New Century made two loans for the Perthshire Lane home for $207,350, representing 100% of the home’s value. That left the borrower with little cushion if home prices fell or the borrower’s income dropped. According to foreclosure documents and other records, Evelin Diaz owns the home. Ms. Diaz couldn’t be reached.

The Palm Coast loan recently was modified, with cuts to the principal and the interest rate, reducing the borrower’s payment significantly, said Mr. Lambert. Mortgage investors dealing with delinquent loans often must choose whether to allow loan modifications to the principal or interest, or face foreclosure, which would cost them even more.

Investors such as Freddie Mac weren’t the only ones hurt. The New Century deal also became part of complex mortgage investments known as collateralized debt obligations, which repackage risky parts of bonds into still other securities.

One such investment, Silver Elms CDO II, included a riskier slice of the J.P. Morgan-New Century bond deal, according to a lawsuit filed against the bank this year in New York State Supreme Court. The suit claims statements made by J.P. Morgan, testifying to New Century’s underwriting standards, were false and misleading. Calls to Robbins Geller Rudman & Dowd LLP, lawyers for Silver Elms and other investors suing J.P. Morgan, weren’t returned.

The funds allege that one couple whose mortgage was in J.P. Morgan’s NC1 pool had income in 2005 of only $826 a month to support monthly debts of $6,478, including payments on a $588,000 mortgage granted by New Century that year. That couple declared bankruptcy in 2006, according to the lawsuit.

“The truth was that New Century had completely abandoned its stated underwriting guidelines,” the investors said in a court document.

Four months after the New Century deal, J.P. Morgan packaged another $905 million of New Century loans into J.P. Morgan Mortgage Acquisition Trust 2006-NC2.

That deal has performed even worse: A quarter of the principal has vanished and 36% of the remaining balance is in default. One of the buyers was Fannie Mae.