Have EM outflows only just begun?

February 2, 2014 Leave a comment

Have EM outflows only just begun?

| Jan 31 10:01 | 9 comments | Share

SocGen’s cross-asset research team believes that when it comes to EM outflows they may have only just begun:

As the team notes on Friday, this is especially so given the Fed doesn’t appear to care about the EM sell-off:

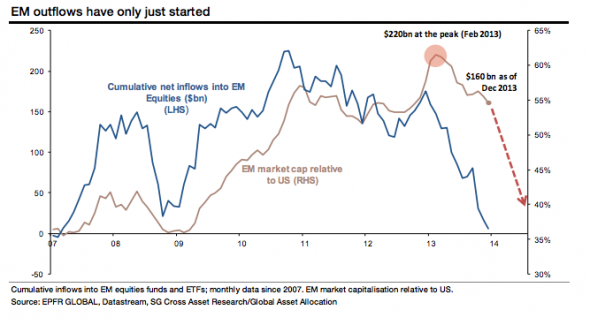

Since cumulative inflows into EM equity funds reached a peak of $220bn in February last year, $60bn of funds have fled elsewhere. Given the exceptionally strong link between EM equity performance and flows, we think it plausible that funds are currently withdrawing double that from EM equity (see chart below). EM bond funds face a similar fate. For reasons discussed in our latest Multi Asset Snapshot (EM assets still at risk – don’t catch the falling knife), we see no early end to EM asset de-rating. Furthermore, the Fed remains assertive on execution of tapering despite recent turmoil within the EM world, which spells more turbulence ahead.

And if it keeps going, balance of payments issues could emerge as a result:

A close look at Global EM funds indicates that all EM markets are suffering outflows Mutual fund and ETF investors in EMs both favour global EM funds. Regional or country specialisation is less common (less than 47% of global EM assets). The implication is that all EM markets face outflows currently, with little discrimination between the countries that are most exposed and those which are more defensive. We think Balance of Payment issues may emerge as an important factor going forward.

Though, what is EM’s loss seems to be Europe’s gain at the moment:

Europe reaps the benefits While current EM volatility is impacting developed markets as well, some of the flows are being redirected toward Europe, notably into Italy, Spain and the UK.

The notable difference with taper tantrum V.2, of course, is that US yields are compressing:

Which might suggest that what the market got really wrong during taper tantrum V.1, was that a reduction in QE would cause a US bond apocalypse. This was a major misreading of the underlying fundamentals and tantamount to some in the market giving away top-quality yield to those who knew better.

Taper at its heart is disinflationary for the US economy, and any yield sell-off makes the relative real returns associated with US bonds more appealing.

That taper V.2 incentivises capital back into the US, at the cost of riskier EM yields, consequently makes a lot of sense.

Though, this will become a problem for the US if the disinflationary pressure gets too big.