Emerging markets: Locus of extremity; Developing economies struggle to cope with a new world

February 3, 2014 Leave a comment

Emerging markets: Locus of extremity; Developing economies struggle to cope with a new world

Feb 1st 2014 | HONG KONG | From the print edition

THE central bank of Turkey boasts an impressive art collection, including a canvas by Erol Akyavas entitled “Locus of Extremity”. That was pretty much where the central bank found itself at midnight on January 28th. Turkey’s currency, the lira, had fallen by 13% against the dollar in the previous six weeks, one of the worst casualties of a broader sell-off in emerging-market assets. Prices were rising (by 7.4% in the year to December) and yet the political pressure to suppress interest rates remained firm. At its unscheduled, nocturnal meeting, the central bank dramatically simplified and tightened monetary policy, raising what will henceforth be its key rate from 4.5% to 10%.

The Turks were not alone. Earlier that day India’s central bank also surprised people by raising rates (albeit by a less extreme 0.25 percentage points) for the third time in five months. South Africa’s monetary authorities followed suit the next afternoon, lifting rates by 0.5 points. The trio deemed their tightening necessary to keep a lid on troublesome inflation and to give a lift to their battered currencies. But it gave their exchange rates only a fleeting lift; late on January 29th they were wobbly again.

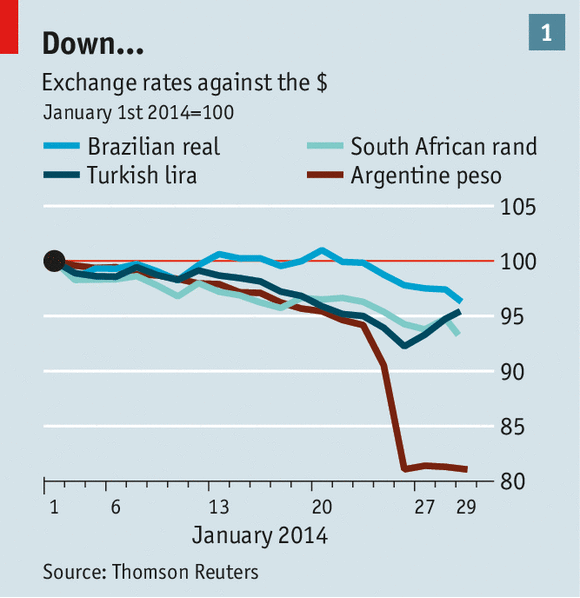

These three economies, alongside Brazil and Indonesia, belong to the “fragile five”. Their currencies suffered dramatic declines last year, after Ben Bernanke, the chairman of America’s Federal Reserve, was tactless enough to say that it would not keep printing money to buy bonds at the same pace for ever. The beleaguered five enjoyed some respite in September, when the Fed decided to maintain its “quantitative easing” for a few months more. But in the past two weeks foreign investors have once again found reasons to sell (see chart 1).

They did not have to look too hard. In recent months Argentina has squandered a big chunk of its foreign-exchange reserves in a doomed defence of the peso, which eventually fell by about 20%, despite the government’s fitful efforts to curtail capital outflows. On January 23rd a widely watched index of manufacturing in China fell by more than expected, raising the prospect of slowing growth amid excessive credit. In Turkey, the sons of three cabinet ministers were arrested in December in a corruption scandal. Meanwhile, in both icy Kiev and balmy Bangkok, protesters are on the streets.

These local difficulties, not all of them little, are unfolding against the backdrop of a gradual rise in global interest rates, as America’s economy strengthens and the Fed moderates its bond purchases. Yields on ten-year Treasuries are still low: about 2.8%. But that is more than one percentage point higher than nine months ago. At Mr Bernanke’s last meeting as chairman, on January 29th, the Fed decided to cut its monthly purchases by another $10 billion, having done the same in December.

The Fed’s bond-buying was not popular in emerging economies. Brazil’s finance minister, Guido Mantega, once accused the rich world of unleashing a currency war: the Fed’s easy money cheapened the dollar, reducing the demand for emerging-market goods. But now that quantitative easing is slowly ceasing, the developing world faces the opposite problem: the Fed’s cutbacks will cheapen American bonds, reducing the demand for emerging-market assets. Alexandre Tombini, governor of Brazil’s central bank, has likened rising rates in the rich world to a “vacuum cleaner” that will suck foreign money out of emerging economies.

How dependent on that money are emerging economies? The amount of emerging-market bonds and equities that foreigners have accumulated is impressive (see chart). But the income and wealth of the emerging economies have also grown over that period. The 30 most prominent such economies account for almost 40% of global GDP, notes the Institute for International Finance, which represents global banks. Yet their weight in benchmark portfolios of global stocks is only about 13%.

As a group, the emerging economies are actually net exporters of capital to the rest of the world. Even as they have attracted large private capital inflows, their central banks have engineered an even greater capital outflow by accumulating big foreign-exchange reserves. They smoked foreign capital but they did not inhale, as Martin Wolf of the Financial Times once put it.

That is true of the group as a whole. But it is not the case for every member, some of whom breathed deep. Turkey, South Africa, India, Brazil and, latterly, Indonesia have all run troublesome current-account deficits, which have left them vulnerable to capital outflows. Moreover, the current-account is “only the bit of the balance of payments that you can see above the surface,” notes Kit Juckes of Société Générale. Countries can experience large and potentially destabilising capital flows in both directions, even as their current account remains roughly in balance, if inflows differ greatly from outflows in their liquidity, maturity or currency.

India and Indonesia have tried to limit their exposure. India has narrowed its current-account deficit dramatically, helped by a ban on gold imports. Indonesia cut fuel subsidies in June and taxed luxuries that are largely imported. And both countries let their currencies fall—a symptom of overstretch that (by encouraging exports and deterring imports) is also a partial remedy.

Having endured big falls since May, the currencies of both India and Indonesia have stood up well to the recent turmoil. The currencies of South Africa and Turkey have not. Their rate hikes this week will help to restore the higher real yields their assets must pay to attract foreign investors.

But according to Mr Juckes, this absolute yield differential is not all that matters. Once rich-country pension funds are earning more than a derisory amount on staid investments at home, they will be far more reluctant to venture into anything “exciting” abroad, even if the spread between domestic and foreign rates remains the same in absolute terms. “Part of me wants to look at interest-rate ratios not interest-rate differentials,” he says. In other words, if American ten-year yields go up from 2% to 3%, it is not enough for emerging-market yields to go up by one percentage point. They have to go up by half.

As real long-term interest rates rise above zero in America, global investment managers are going through an enormous “one-off adjustment”, Mr Juckes reckons. They are anticipating a “more normal world”, in which pension funds can meet their obligations by holding safe but rewarding assets in countries they know well. It was a world America began to leave behind in late 2007, when the crisis broke and the dramatic rate cuts started. At that time, curiously enough, the central bank of Turkey’s “Locus of Extremity” was on loan to America’s Federal Reserve.

The coin has two faces

Other currencies’ losses may be the dollar’s gain

Feb 1st 2014 | From the print edition

SINCE the debt crisis of 2008, the foreign-exchange market has been the dog that didn’t bark. The euro has not broken up; the dollar has not imploded in the face of quantitative easing; the yuan has not become the world’s reserve currency of choice. Although the dollar received a lift when markets were collapsing in late 2008 and early 2009, its trade-weighted index is within 2% of where it was when Lehman Brothers crumbled (see chart).

Currency traders have had little to get their teeth into. Often they focus on yield differentials, buying the currency with the highest interest rates, but yields have been low and barely differentiated between countries. Sometimes they look at economic-growth forecasts, but growth has been uniformly sluggish. And sometimes they look at current-account deficits, but the American deficit has shrunk, the Japanese surplus has disappeared completely and the euro area’s biggest imbalances are internal, not external.

Policy has also dampened fluctuations. The euro bears were frustrated because the European Central Bank (ECB), under Mario Draghi, proved to be more flexible than its critics suggested while the German government proved willing to do just enough to keep the euro zone intact. Those who predicted the imminent demise of the dollar thanks to the Federal Reserve’s experimentation forgot that other central banks were also cutting rates to zero and expanding their balance-sheets. Those who bought yen or Swiss francs in search of a safe haven were frustrated by central-bank intervention to limit their rise.

If there was a long-term trend, it was that the currencies of developed economies were falling and those of emerging markets were rising. Economists viewed this as the “right” thing to happen, even though it caused grumbles from some politicians about “currency wars”.

But that trend reversed itself last year, and at the start of 2014 currency markets are on the move again. Attention has focused on the sudden drops in the currencies of various emerging markets, thanks both to slowing growth and poor economic management in the countries concerned, and to the Fed’s decision to begin reducing (“tapering”) its bond purchases. The corollary of cheaper liras, pesos, rand andreais, of course, is a more expensive dollar. There is a sense that American investors are bringing their money home, after a long period when they sought higher returns abroad. Figures from EPFR Global, a data provider, show that investors started switching from emerging-market equity funds into rich-world ones in 2013.

As yet, the dollar is still well below the highs it reached earlier this century against the euro (in 2001) or the yen (in 2002). But Citibank, which monitors foreign-exchange flows, says long-term investors have shifted from being dollar-sellers into dollar-buyers, so its rise may yet continue. The Japanese authorities seem happy to let the yen weaken, and the euro zone is sliding dangerously close to deflation, which may yet prompt further monetary easing by the ECB later this year.

Meanwhile, some of the market’s favoured currencies have lost their appeal. Both the Australian and Canadian dollar had moments in the past five years when they traded above parity against the greenback, but each has dropped significantly in recent months. Weak commodity prices may be largely to blame, but it could be another case of American investors rediscovering the joys of home.

The dollar’s last extended period of strength was in the late 1990s, when optimism about the growth-enhancing potential of the internet was at its height. A similarly optimistic mood exists today, linked to the potential for shale oil and gas to reduce America’s energy costs and thus boost its manufacturing sector.

A strong dollar can have negative consequences. In the late 1990s several emerging economies struggled to maintain their pegs to the greenback, leading to financial crises in both 1997 and 1998. It will also, other things being equal, make life more difficult for big American companies, making their exports less competitive and reducing the value of overseas earnings when translated back into dollars for quarterly results. Countries that import a lot of commodities will, for their part, pay more for them, since they are all priced in dollars.

But it is not all bad news. If the dollar is starting a bull run, the American government should have no problem finding buyers for its bonds. When the Fed mused about tapering last May, yields rose sharply; so far in 2014, ten-year yields have fallen by a third of a percentage point.