If Brazilians find themselves in a tight spot, they say they are in a saia justa (a tight skirt); Brazil’s president has left herself little room for economic manoeuvre ahead of a difficult re-election campaign

February 10, 2014 Leave a comment

Brazil’s president has left herself little room for economic manoeuvre ahead of a difficult re-election campaign

Feb 8th 2014 | From the print edition

IF BRAZILIANS find themselves in a tight spot, they say they are in a saia justa (a tight skirt). Although she usually prefers trouser suits, that is precisely where Dilma Rousseff finds herself. Later this month she will launch her campaign to win a second term in a presidential election due on October 5th. Normally at this stage of the political cycle, as in the run-up to elections in 2006 and 2010, the government would be ramping up spending. But when Ms Rousseff spoke to the World Economic Forum in Davos last month, with the São Paulo stockmarket and the real dipping along with other emerging economies, she felt impelled to stress her commitment to being strait-laced.

Brazil’s economy has disappointed since she took office in January 2011. Growth has averaged just 1.8% a year; inflation has been around 6%; and the current-account deficit has ballooned, to 3.7% of GDP. Her government has some good excuses. She inherited an overheating economy, the world has grown sluggishly, and cheap money in the United States and Europe prompted an exaggerated appreciation of the real.

But Ms Rousseff has scored some own goals as well. Her predecessor, Luiz Inácio Lula da Silva, left monetary policy to the Central Bank and mostly stuck to clear fiscal targets. By contrast, Ms Rousseff chivvied the bank into slashing interest rates; her officials tried to micromanage investment decisions with subsidies and to cover up the fiscal damage through accounting tricks. Rather than the promised recovery of growth, the result was that Brazilian businessmen and foreign investors lost confidence in the economic team—and just at the wrong time. When America’s Federal Reserve last year announced a possible “tapering” of its bond-buying, the real began to slide. Against the dollar, it is now 17% below its value in May.

A weaker currency is just what Brazil needs if it is to balance its external accounts and its manufacturers are to thrive. But it also risks adding to inflation, the upward creep of which was one factor (along with poor public services) in mass protests that shook Ms Rousseff’s government last year. This has prompted a change of mind. Alexandre Tombini, the Central Bank governor, has been allowed to raise interest rates (from 7.25% to 10.5%). At Davos, Ms Rousseff for the first time said that her aim was to bring inflation down to 4.5%; she previously seemed content merely for it to stay below the ceiling of the target range of 2.5-6.5%. Lula, her political mentor, “surely told Dilma that interest rates won’t lose her the election, but inflation might,” says a senior opposition economist.

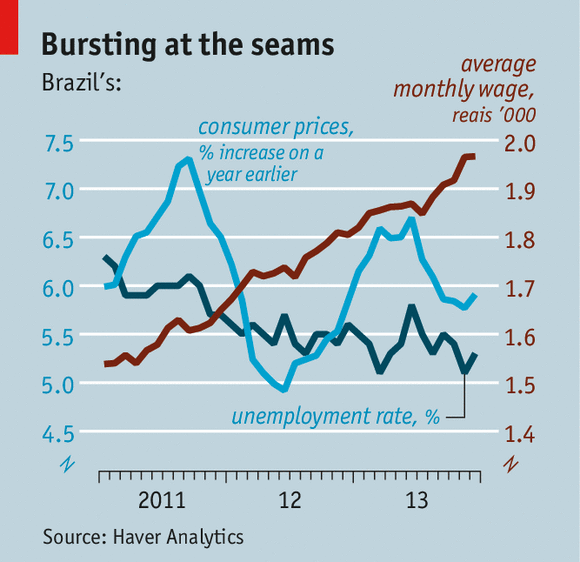

The Workers’ Party, which has ruled Brazil since 2003, expects to fight and win the election on its record of job creation and of lifting 40m Brazilians out of poverty. Unemployment is low and real wages are still rising (see chart). This explains why Ms Rousseff remains the clear favourite for October. A Datafolha poll in late November gave her 47% of the vote, compared with 19% for Aécio Neves and 11% for Eduardo Campos, her main challengers.

Some market analysts include Brazil as one of five “fragile” emerging economies, but the government rightly counters that it does not belong in the same company as Argentina or Turkey. As Mr Tombini points out, Brazil has a strong banking system and the reserves ($376 billion) to smooth a gradual exchange-rate adjustment. While talking of fiscal responsibility, the signs are that the government thinks it can get away with postponing belt-tightening until after the election.

But what if a mixture of outside events and fiscal fudging at home (and even a possible downgrade by credit-rating agencies) prompts a bigger decline in the real? So far the pass-through of devaluation to domestic prices has been low, but the history of price-setting in Brazil suggests that this might suddenly change if the currency weakens further, says Monica Baumgarten de Bolle, an economist at Rio de Janeiro’s Catholic University. “This is what really worries the Central Bank,” she says. It would have to respond with a monetary squeeze, killing growth.

In the same Datafolha poll 66% of respondents said they want the next president to act differently from Ms Rousseff, a generic yearning for change that suggests her support may be less solid than it seems. By allowing inflation to become a campaign issue, she has strayed on to the opposition’s ground. Her past mistakes have led her to a situation in which her promise to spend more on public services is uncomfortably dependent on the humours of international investors. That is the tight skirt she has donned. The next few months will show whether she can wriggle out of it.