China’s Central Bank Leads Effort to Regulate Internet Finance; Move Comes as Technology Firms Muscle In on Businesses Dominated by Traditional Banks

February 14, 2014 Leave a comment

China’s Central Bank Leads Effort to Regulate Internet Finance

Move Comes as Technology Firms Muscle In on Businesses Dominated by Traditional Banks

LINGLING WEI and PAUL MOZUR

Updated Feb. 11, 2014 7:06 a.m. ET

BEIJING—China’s technology giants are marching onto the turf of the country’s state-controlled banks, soaking up tens of billions of dollars’ worth of investor money.

Now, regulators are taking notice.

China’s central bank is leading a government effort to stem potential risk from a new generation of popular online investment products, according to people with direct knowledge of the matter. Officials are looking to develop regulations aimed squarely at products offered by an affiliate of e-commerce giant Alibaba Group Holding Ltd. as well as by rivals Tencent Holdings Ltd. 0700.HK 0.00% and Baidu Inc. BIDU +1.25%

The products offer higher yields than bank deposits and are easy to access with smartphones and other gadgets. But some Chinese officials worry that investors often don’t know where their money is being placed and are vulnerable to theft of personal information. The worries come amid broader concerns about potential disruptions in China’s vast but opaque shadow-banking system, an array of lenders such as so-called trust firms, leasing companies and insurers.

Officials stressed that they hope the Internet companies could still play a role in making China’s creaky financial system more competitive, improving the flow of lending to small businesses and encouraging greater competition from stodgy state-run banks. “The goal is not to crack down on the sector, but to foster its healthy development,” said an official at the People’s Bank of China, 601988.SH 0.00% China’s central bank.

How tightly the government regulates tech firms’ financial offerings could indicate how willing Beijing is to relax its decadeslong hold on China’s banking system.

“If Internet finance products cause [financial] problems, no doubt the banking regulator and the PBOC will step in,” said He Fan, a senior economist at the Chinese Academy of Social Sciences. “If the products are successful, the banking regulator and the PBOC will step in the name of fair play. They will be pushed by the commercial banks.”

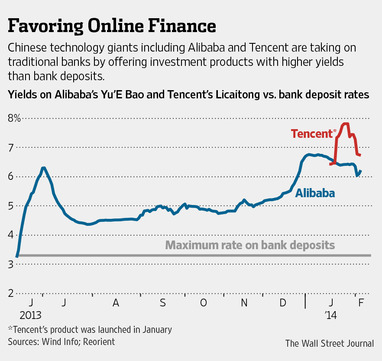

The amounts held in Internet products are small, compared with China’s 46 trillion yuan ($7.59 trillion) in bank deposits, but growing rapidly. Alipay, Alibaba’s online payment affiliate, launched Yu’E Bao, or “leftover treasure,” a product similar to a money-market fund, last summer. As of mid-January, it had more than 49 million customers with more than $40 billion in investments, according to Alipay.

According to MorningstarInc., MORN 0.00% the investment-research firm, the $30.6 billion that Yu’E Bao held at the end of December made it the world’s fourth-largest money-market fund.

Currently, Yu’E Bao offers rates of about 6%, compared with the maximum of 3.3% banks can offer on deposits under Chinese regulations. Alipay says the money is invested in debt, currencies, deposits and other liquid assets. Tencent and Baidu now offer their own Yu’E Bao-like investments.

This week, Alipay moved to offer online its first wealth-management product, a popular type of investment similar to a bank deposit but with a higher yield. On Friday, it is set to begin selling a one-year, principal-guaranteed product with an advertised annualized return of 7%. Alipay said the product would invest in bank deposits, the property sector, equities and other instruments.

Wealth-management products typically are a staple of banks, which offer them to consumers as a way to obtain higher yields than are available on deposits. Lenders compete for investors’ cash via the level of returns they offer.

Alipay processes payments for Alibaba’s Taobao and Tmall online shopping services, so it is already familiar to China’s legions of online shoppers.

The PBOC—working with China’s banking, securities and insurance regulators—is trying to put in place this year measures that would protect consumer information from being stolen or misused, ensure adequate risk disclosure over the Internet-based investment products, and prohibit illegal fundraising activities, said people knowledgeable about talks among the regulators.

They also said Chinese officials are responding to recent collapses among a separate group of small Internet-based lending firms. Those firms, known as peer-to-peer lenders, link individuals looking for better returns on their funds with borrowers starved for cash.

Big Chinese banks, including Industrial & Commercial Bank of China Ltd.601398.SH -0.29% and Bank of China Ltd., are pushing back against online lenders by offering money-market funds or slightly raising rates on cash deposits. ICBC and Bank of China declined to comment. Deposit rates in China are set by the government, with limited competition allowed, and banks often pay interest rates near or below the rate of inflation—whetting the appetite of depositors for higher yields.

Fostering Internet finance could help change the politics on one of the central bank’s major priorities: liberalizing interest rates. For decades, China’s largest banks have opposed liberalizing deposit rates because that would increase their costs. But the pressure from Internet financing could turn the banks into proponents of liberalization, say advisers to China’s central bank, because that would give the banks a way to compete for funds.

The PBOC has been trying to move China to a system under which interest rates are set more by the market, figuring that would force financial institutions to make lending decisions based on potential payoff, rather than on government guidance. That could direct more lending to smaller, newer firms, rather than to the banks’ largest customers, namely big, state-owned companies.

So far, the tech firms have been targeting a demographic group underserved by the large, state-run banks: small businesses and the average consumer. In the past two years, Alibaba has been extending loans to the hundreds of thousands of merchants on its e-commerce websites, evaluating their creditworthiness based on the company’s records of the performance of those merchants.

The company said it had a loan book of about $2 billion as of the end of last year. Less than 2% of those loans were nonperforming as of July, it said.

“Creative disruptions to the traditional banking sector will gain, not fade, in the coming year,” predicted Steve Wang, head of China research at Reorient Financial Markets Ltd., a Hong Kong-based investment bank.