A Big, Bad World for America Inc.

February 15, 2014 Leave a comment

A Big, Bad World for America Inc.

JUSTIN LAHART

Feb. 12, 2014 4:44 p.m. ET

Trouble in emerging markets is unlikely to hurt the U.S. But America’s companies may not be as lucky.

It has been a rough year so far for developing economies. Several, including Turkey, Argentina and South Africa, have seen sharp slides in their currencies. The Federal Reserve’s reining in of its bond-buying program is causing fits elsewhere, and worries about capital flight have contributed to some central banks’ recent decisions to raise interest rates. Signs that China’s growth is softening, along with worries about the stability of the country’s “shadow banking” system, have added to the mix.

Although emerging-market woes have played a part in the drop in the U.S. stock market this year, worries they could cause serious financial-market problems in the U.S. have been subdued. Unlike the Mexican peso, Asian financial and Russian debt crises of the 1990s, banks’ emerging-market exposures seem well managed. And investors have shied away from the types of heavily leveraged, multiple-country bets that led to the Fed-supervised bailout of Long-Term Capital Management in 1998. In her inaugural testimony as Fed chairwoman Tuesday, Janet Yellen said that the central bank isn’t viewing the recent volatility in global financial markets as a threat to the U.S.

But while the risk of financial-market contagion from emerging markets has lessened, their role in the global economy has grown. Countries outside of the Organization for Economic Cooperation and Development nations that the World Bank classifies as high-income generated 61% of global gross domestic product, on a U.S. dollar basis, in 2012. That was up from 53% in 2000.

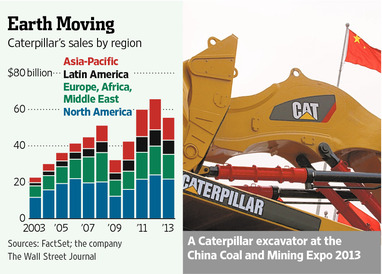

Precise numbers aren’t available, but as emerging economies have grown, they also have become more vital to many large, public companies’ businesses. General Electric,GE -0.16% for example, made 34% of its sales outside of the U.S. and Europe in 2012 versus 17% in 2003. Caterpillar CAT +1.27% generated 36% of its total sales last year in Latin America and the Asian-Pacific region, compared with 21% in 2003. Countries outside of the U.S. and Europe accounted for 40% of Johnson & Johnson‘s JNJ -0.59% sales in 2013, up from 17% in 2003.

A broad set of data from the Commerce Department on U.S. multinationals’ majority-owned foreign affiliates paints a similar picture. In 2011, countries outside of the high-income OECD members accounted for 34% of sales at U.S. multinationals’ majority-owned foreign affiliates. That compared with 25% in 2000.

Emerging markets’ role in companies’ expansion plans has been even more pronounced. In 2011, non-OECD countries accounted for 42% of capital spending at multinationals’ foreign affiliates, versus 30% in 2000. In other words, not only do emerging markets now represent a greater share of sales, they are where companies have put bigger stacks of their chips.

Given the pace of emerging markets’ growth over the past decade, and the promise of what they may become, it isn’t hard to see why U.S. companies have done this. But there is a risk that in chasing growth they, and their shareholders, have lost sight of just how volatile emerging-market economies can be. This year may serve as a reminder.