From Micro-Caps to Mid-Caps, a Comprehensive Approach to Smaller Companies

February 15, 2014 Leave a comment

From Micro-Caps to Mid-Caps, a Comprehensive Approach to Smaller Companies

by Royce FundsFebruary 12, 2014, 4:40 pm

As the small-cap asset class has grown in size, those companies just beyond the periphery of small-cap have become somewhat orphaned.

By moving up to the smid-cap space and looking down to the micro-cap space, we not only give ourselves access to an underappreciated—and inefficient—zone of the equity market, we also potentially enable some of our long-held, favored investment ideas to continue to benefit our clients as they grow beyond the smaller-company universe.

Starting at the Bottom, Looking Past the Top

When selecting stocks for our portfolios, we have always taken a comprehensive approach. For example, we never hesitate to look down the market capitalization scale to find conservatively capitalized companies that we think are well managed and attractively valued. More recently, we have also been looking up.

When looking down, we use the same criteria we do elsewhere in the small-cap space, seeking companies with underlying financial strength in the form of strong balance sheets and high returns on invested capital. We began referring to this traditionally more volatile sub-segment of small-cap as micro-cap back in the early ’90s and currently define them as those stocks with market caps up to $750 million.

Expanding Our Opportunity Set

Being accustomed to looking further afield than many other investors, we think that smid-cap stocks represent a logical extension of our analytical expertise in the small-cap universe.

Just as we do not hesitate to look down the market cap scale at micro-cap stocks, we see both monitoring and investing in smid-cap companies as a critical expansion of our core area of competence. It allows for ongoing use of our domain knowledge as companies we know well move up (and down) in market cap, crossing the border of small and mid.

The most common definition of smid-cap is any company eligible for inclusion in the Russell 2500 Index, which includes all of the stocks in the Russell 2000 Index (one of the best-known-small-cap indexes) plus the 500 smallest stocks in the Russell Midcap Index. Thus the smid-cap universe encompasses all small-cap stocks plus the smallest mid-cap issues.

We think that the smid-cap universe combines many of the attractive performance attributes of the small-cap segment. Smid-caps have many of the liquidity and business stability characteristics more traditionally associated with larger enterprises; these attributes also tend to be present in small-caps outside the micro-cap zone, which we would define as those with market caps between $750 million and $2.5 billion.

Interestingly, as small-cap has become an established asset class, those companies just beyond the periphery of small-cap have become somewhat orphaned, and therein lies the opportunity. By moving up to the smid-cap space, we not only give ourselves access to an underappreciated zone of the equity market, we also potentially enable some of our best investment ideas to continue to benefit our clients as they “graduate” to mid-cap status.

Our more than four decades of asset management experience have taught us that the small-cap asset class is a larger and broader universe than a single index can encompass.

Compelling Performance

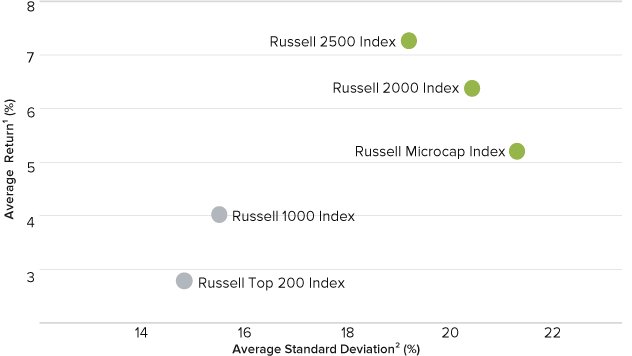

Examining performance characteristics provides a clear case for the opportunity presented by smid-cap stocks. To illustrate this, we compared the Russell 2500 to the Russell 2000, and the Russell Microcap Index. To represent the large-cap universe, we used the Russell 1000 and the Russell Top 200 Index.

We were interested not only in return characteristics but also risk characteristics, and by using five-year annualized rolling data, we evaluated a robust data set. To allow complete participation for each index, we selected a start date of June 30, 2000, the inception of the Russell Microcap Index, the newest of the Russell Indexes we evaluated.

1 Average of monthly rolling average annual five-year total return

2 Average of monthly rolling average annual five-year standard deviation

As one would expect, micro-, small-, and smid-cap stocks offered higher returns with higher volatility than their large-cap counterparts. Notably, the Russell 2500 provided the highest average of the average five-year annualized returns of all five indexes at 7.26% and did so with lower average volatility than the small- and micro-cap indexes.

Throughout the evaluation period, the aggregate performance of micro-cap companies lagged that of small- and smid-cap companies while also showing higher volatility. The Russell Microcap captures the smallest investable companies in the U.S. equity market, zeroing in on what we believe is that market’s most inefficient segment.

This makes micro-cap ideally suited to disciplined, active managers prepared to perform deep analysis on more obscure companies. Our approach to micro-caps centers on companies that have strong balance sheetsand high returns on invested capital, traits that we believe can help to compensate for the additional volatility that often comes from investing in the smallest of the small.

We look far and wide in the micro-cap universe, considering many stocks that are not in the index, including non-U.S. stocks. By using our time-tested approach, we are hoping to identify stocks with long-term return potential in part by emphasizing those with the ability to survive unexpected downturns.

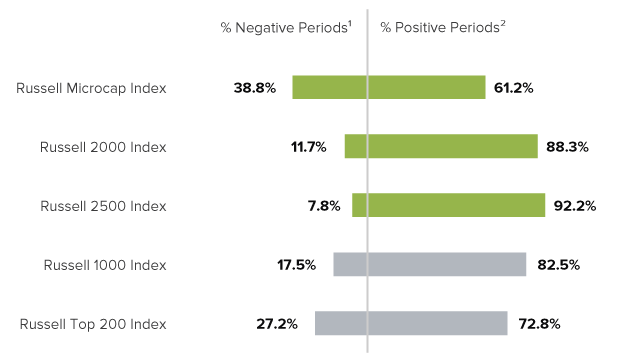

Further analysis also supported both an extension into smid-cap and a risk-focused approach to micro-caps by looking at the percentage of positive and negative five-year rolling periods for each index. A similar pattern again emerged as the smid-cap index outshone all of its peers with more than 92% of all five-year periods being positive, compared to 83% of five-year periods being positive for large-caps and only 61% of five-year periods positive for micro-caps.

1 Percent of positive monthly rolling average annual five-year returns

2 Percent of negative monthly rolling average annual five-year returns

Drilling down further in order to understand the magnitude of returns, we separated all positive and all negative five-year rolling periods and computed their averages. As displayed in the chart below, the average of all positive average annual five-year rolling returns for the Russell 2500 was an impressive 8.1%, compared to 5.3% for the Russell 1000.

The chart also shows the return-enhancing potential of the Russell Microcap Index. When positive, the Russell Microcap boasted an average of average annualized five-year returns of 10.46%.

As one might expect, during five-year periods with negative returns, the worst results came from the Russell Microcap, at -3.1%, followed somewhat curiously by the Russell 2500 at -2.3%.

1 Average of all positive monthly rolling average annaul five-year returns

2 Average of all negative monthly rolling average annual five-year returns

Conclusion

Our more than four decades of asset management experience have taught us that the small-cap asset class is a larger and broader universe than a single index can encompass.

The acceptance of small-cap stocks as a permanent part of an investor’s portfolio, combined with the traditionally dominant allocation to large-cap stocks, has created a meaningful investment opportunity in those stocks that fall both below and above conventional small-cap boundaries.

If we are to use market exposure as our guideline in determining proper allocation to an asset class, we think one may want to measure the proportion of the Russell 3000 Index that is comprised of smid-cap stocks—interestingly, its long-term average weight has been approximately 18%.1

Smid-caps demonstrated strong historical performance, lower volatility, and greater liquidity than many small-caps while also frequently boasting greater financial resources and business stability.

The underfollowed, often misunderstood micro-cap asset class, although more volatile, also offers unique opportunities, especially for patient managers with a focus on managing volatility.