Chinese Capital Markets Frozen As Bad Loans Soar To Highest Since Crisis

February 16, 2014 Leave a comment

Chinese Capital Markets Frozen As Bad Loans Soar To Highest Since Crisis

Tyler Durden on 02/14/2014 14:05 -0500

Chinese capital markets are quietly turmoiling as debt issues are delayed and demand for “Trust” products – the shadow-banking-system’s wealth management ‘investments’ – is tumbling. As Nikkei reports, since January, 9 companies have postponed or canceled issuance plans (around $1 billion) and is most pronounced in privately-owned companies (who lack an implicit government guarantee). This, of course, is exactly what the PBOC wanted (to instill some fear into these high-yield investors – demand – and thus slow the supply of credit to the riskiest over-capacity compenies) but as non-performing loans in China surge to post-crisis highs, fear remains prescient that they will be unable to “contain” the problem once real defaults begin (as opposed to ‘delays of payment’ that we have seen so far).

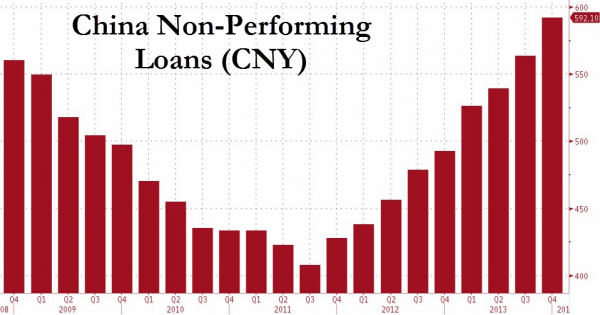

Chinese banks’ bad loans increased for the ninth straight quarter to the highest level since the 2008 financial crisis, highlighting pressures on asset quality and profit growth as the world’s second-largest economy slows.

Non-performing loans rose by 28.5 billion yuan ($4.7 billion) in the last quarter of 2013 to 592.1 billion yuan, the highest since September 2008, the China Banking Regulatory Commission said in a statement on its website yesterday.

Chinese banks are struggling to keep soured loans in check and extend earnings growth as the slowing economy and government efforts to curb shadow financing make it harder for borrowers to repay debt.

“China’s economic growth turned downward with the new leadership switching policy focus to reform and risk management from emphasizing stable expansion,” said Wang Yichuan, a Wuhan-based analyst at Changjiang Securities Co. “Naturally the bad loans will increase along with the change. We expect the deterioration to continue for two more years.”

Chinese banks added 89 trillion yuan of assets, mostly through loans, in the past five years, equivalent to the entire U.S. banking industry’s, CBRC data show. By comparison, U.S. commercial banks held $14.6 trillion of assets at the end of September, according to the Federal Deposit Insurance Corp.

Investors are increasingly concerned that China’s investment through borrowing since 2008 may trigger a financial crisis

Concerns over potential defaults on high-yield financial products are making Chinese companies put some debt issues on hold due to wary investors, as well as posing a potential new risk to the global economy.

Since January, nine companies have postponed or canceled issuance plans for a total of 5.75 billion yuan ($948.24 million) in bonds and commercial paper, equivalent to about 2% of the debt issued over the period.

This is most pronounced among privately operated companies, whose lack of government backing has meant less interest from potential investors than hoped.

Demand has been dulled by worries over defaults on so-called wealth management products, a feature of China’s shadow banking system.

Broader credit risks have driven interest rates up, and the gap between corporate debt and more-creditworthy government bonds is widening. Average yields on AA-rated seven-year corporate bonds reached 8.44% in mid-January.

So even if companies offer bonds, they will be unable to raise money if they cannot pay these higher rates.

“There’s a possibility that the Chinese government will step in to keep the negative impact from spreading,” says Hiromichi Tamura, chief strategist at Nomura Securities, “but if these types of repayment delays continue, they could trigger a global stock market downturn.”

Western Banks And China: “Interesting Times” Are Coming

Tyler Durden on 02/14/2014 19:09 -0500

Submitted by Pater Tenebrarum of Acting-Man blog,

Western Bank Exposure to Mainland China Explodes Higher – Australia Vulnerable

We recently cited the work of Sean Darby, equity strategist at Jefferies, regarding the exposure of Hong Kong banks to the Mainland (see: “How Dangerous is China’s Credit Bubble for the World” for details). Although Hong Kong is technically part of China, it is a foreign country in terms of its economic system and currency, and should therefore be regarded as a foreign creditor. In fact, the incentives that mainly influence the business decisions of Hong Kong’s banks include the US Federal Reserve’s monetary policy as a very important factor, due to the fact that the Hong Kong dollar is pegged to the US dollar via a currency board.

Mr. Darby has in the meantime continued to dig into topic of foreign bank exposure to the Mainland, and has recently released his latest findings. Here is a Bloomberg chart that shows how these claims have grown since 2005:

Foreign participation in China’s credit boom: note the involvement of French and Australian banks specifically – click to enlarge.

The numbers are as follows at present (the percentage change is since Q1 2011, indicated by the vertical line on the chart above).

| Country | % change | Total in US$ 3Q13 |

| Germany | +66% | 32bn |

| France | +60% | 41bn |

| UK | +70% | 193bn |

| Total Europe | +70% | 329bn |

| Australia | +230% | 31bn |

| US | +18% | 83bn |

The total exposure of Western banks thus amounts to $709 billion. Australia’s banks were a bit late to the game, but sure did their best to catch up quickly, as the 230% increase in their claims since 2011 shows.

Aussie Bank CDS has yet to reflect this…

In other words, we now have additional evidence of the growing vulnerability of Australia specifically. As we already pointed out in our musings about how “financial contagion” might spread from China in spite of its closed capital account, Australia is a pivotal region. Australia’s economy greatly depends on China’s commodity imports, and its banks have financed an enormous real estate bubble on the back of the commodities boom.

Moreover, Australia’s banking system itself is highly dependent on foreign short term funding sources. Although the chart above doesn’t tell us anything about the maturities of the claims on China, we would not be surprised if many or even most of the loans to China had much longer maturities than the foreign funding Australian banks get from (mainly) Europe. The main point is though that we have yet another source of potential trouble for Australia here – the exposure of Australian banks to China amounts to 9% of Australia’s GDP at this point.

Lured by High Spreads, Interesting Times Await

As Mr. Darby points out, the amounts have grown quite large in absolute terms. Banks have evidently been lured by the higher spreads they can earn on loans to Chinese customers, and in large part this is due to the ZIRP policies pursued by major Western central banks. However, higher spreads usually obviously imply higher risk. Adding Hong Kong’s exposure to the above numbers, we arrive at about $860 billion in total foreign exposure (ex-Japan we might add).

In the course of this year, some $800bn. of debt issued by ‘wealth management products’ is coming due in China, and Mr. Darby notes in this context that the potential knock-on effects on Western banks from an increase in non-performing loans in China are probably not properly appreciated at this juncture.

Especially UK banks with a huge $193 bn. in total exposure, as well as Hong Kong banks (approximately $150 bn. in net claims) and Australia’s ‘big four’ banks seem to be in the line of fire here.

Moreover, we must expect that in the event of a shadow banking crisis in China – a highly probable event given what is known about the practices of the sector and the amount of debt coming due in the near future – will have considerable effects on numerous emerging market economies, especially if China should eventually decide to devalue the yuan (currently the yuan seems quite overvalued actually). In that event, both commodity exporters and exporters of semi-finished and final goods that compete with China would feel the pinch.

This would in turn mean that Western banks would not only have to grapple with a possible rise of NPLs in China itself, but also with an even bigger currency and debt crisis in a number of emerging markets. Since many Western banks remain in weak condition following the 2008 crisis and the euro area debt crisis, they will then be inclined to further reduce their lending in their home countries as well, so as to preserve capital. A vicious cycle could easily be triggered.

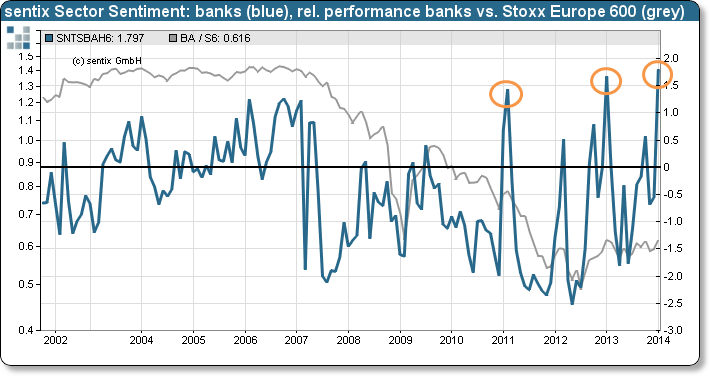

It is quite ironic in this context that German sentiment data provider Sentix recently noted that ‘bullish sentiment on bank stocks has reached a record high‘.

Sentix sentiment indicator on European bank stocks storms to a record bullish consensus in late January – click to enlarge.

Conclusion:

There is a very good chance that the crisis that began in 2008 is actually not over by any stretch – it is merely moving from one place to the next. After all, the developments discussed above are a direct result of the reaction of the world’s monetary authorities to the initial crisis. China’s credit bubble and ZIRP in the US and Europe are all children of the crisis and have evidently sown the seeds for the next crisis. As we always stress, we expect that the next major crisis will eventually lead to a crisis of confidence in said monetary authorities. At some point, faith in central banks is bound to crumble and then we will really experience ‘interesting times’.