The promoter problem in Indian banks

February 16, 2014 Leave a comment

The promoter problem in Indian banks

| Feb 14 10:55 | Comment | Share

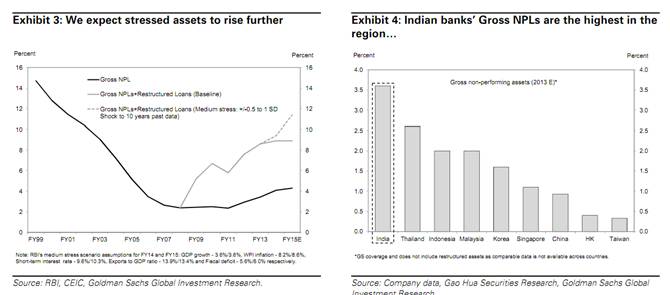

Or — watch the rate of stressed asset growth in the industry:

That’s from Goldman, they of the Modi-fied viewpoint. You can check out United Bank of India for more…

On a systemic point it’s worth noting the impact such hamstrung banks can have on GDP growth and the circular nature of the problem. India’s already capital starved and although sensitivity of GDP to bank credit growth is lower than that in China, it’s still a potentially serious drag. The estimate is that a 1 per cent fall in credit growth could shave off 20bps from overall GDP growth.

From Goldman again:

The lower sensitivity in India’s case may be attributable to the low absolute level of credit in the economy. India’s bank credit/GDP ratio is only 55% compared to China’s at 240% (including shadow banking). Low levels of financial deepening mean that the impact of incremental credit growth is not as strong as in countries with more developed banking systems. That said, the impact is still positive and significant. Therefore, we expect a slowdown in credit growth to weaken GDP growth.

Overall, our analysis suggests that the ability of the banking system to lend is currently stretched. Indeed, the current loan growth of 14.8% that we have seen in FY14 may have been inflated by ‘evergreening’ of loans. Our Financials Research team expects that the ability of banks to lend may be weaker in FY15 due to the overhang of stressed assets, strained profitability, and provisioning required for higher NPLs. They estimate loan growth of 12%-14% in FY15, with downside risk in the case of adverse political outcome. If credit growth slips a notch, our sensitivity analysis suggests that it could reduce GDP growth by 20-40bp. In our view, this increases downside risks to our GDP growth forecast of 5.5% for FY15.

Significantly, this also works the other way around, which explains the RBI’s haste to up the number of bank licenses, clean up stressed assets and improve financial inclusion — best to get a process which will take several years started as soon as possible, in short.

As the FT wrote before, a great deleveraging is probably needed and the only way to do that is to drag dodgy tycoons where they don’t want to go. Banks seem unwilling to push them. As a seemingly irritated Rajan said of of those known over here as promoters, they have “no divine right to stay in charge, regardless of how badly they mismanage an enterprise, [or] to use the banking system to recapitalise their failed ventures”. Good luck to him.

A final, optimistic, chunk from Goldman:

Our analysis suggests that there could be significant positive spillover effects if clogged investment projects come on stream. If projects start generating revenues, it will increase cash flow, could improve profitability, and help improve corporate balance sheets. This can then enable them to not only service outstanding debt, but make them more creditworthy. Banks’ balance sheets can also improve as restructured loans become performing loans, the risk weights on these loans reduce thereby improving capital ratios, and provisioning ratios start looking better. As balance sheets heal, they can encourage the start of a fresh lending cycle, and therefore growth. Given the trajectory of stressed assets, we do not see a fresh cycle starting in FY15 as balance sheets need time to heal.