Knowing When It’s Time to Sell Your Favorite Stock: It can be as important as deciding to buy.

February 22, 2014 Leave a comment

Knowing When It’s Time to Sell Your Favorite Stock

It can be as important as deciding to buy.

MARK HULBERT

Updated Feb. 14, 2014 7:19 p.m. ET

Investors spend far more time searching for stocks to buy than thinking about when to sell. That is a potentially costly shortcoming, especially in a bull market that is approaching its fifth birthday, which is how old its predecessor was when it ended in 2007.

You should carefully analyze your stock holdings to decide which, if any, should be sold. One general rule of thumb is to subject your stocks to the same valuation criteria that you used when initially deciding to purchase them. If you bought a stock because its price/earnings ratio is well below the market’s, for example, then you should consider selling it if its P/E is now well above.

Researchers also have identified a handful of lesser-known indicators that you can use to help identify stocks you might want to unload. They derive from the aversion most investors have to selling. That aversion is so strong that when a stock overcomes it and becomes heavily sold, it really means something—and it’s a good bet to underperform in coming months.

The reluctance of investors to part with stocks they once loved enough to buy plays out in many ways. For example, investors typically sell a stock only when they need cash to buy another one about which they have become particularly excited, according toTerrance Odean, a finance professor at the University of California, Berkeley. Furthermore, he says, they often resist selling any stock they are holding at a loss—something that, needless to say, has nothing to do with its potential.

As a result, Mr. Odean says, “for most investors, buying is a forward-looking activity and selling is a backward-looking activity.”

This inertia tends to lead to a protracted selloff of unloved stocks, says Andrea Frazzini, a finance professor at New York University and a principal at AQR Capital Management, a firm that manages several hedge funds and other investment offerings and has nearly $100 billion in assets. The takeaway, he says: Bite the bullet on a stock that has significantly lagged the market over the past 12 months.

Individual investors aren’t the only ones who exhibit a strong aversion to selling; Wall Street analysts do, too. Currently, for example, just 25 stocks within the S&P 1500 index have a consensus analyst recommendation to either sell or underweight, according to FactSet. Two-thirds fall into the “buy” or “overweight” categories.

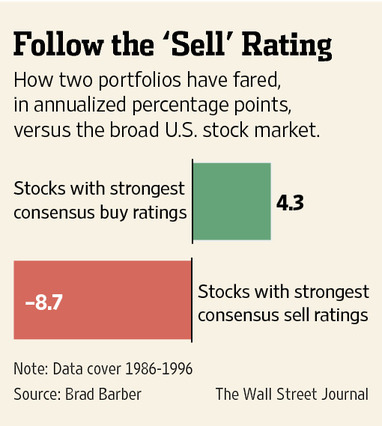

We therefore should pay particular attention when analysts do actually say “sell.” In one academic study conducted in the 1990s, the average consensus sell-rated stock lagged the market by 8.3 percentage points a year—more than twice as much as the margin by which the typical stock with a consensus “buy” rating outperformed the market.

Brad Barber, a finance professor at the University of California, Davis, and one of the co-authors of that study, says that while more recent studies reached broadly similar results, he isn’t aware of any that have updated it. He says that the message of the research is that it makes more sense to follow a consensus sell signal from Wall Street analysts than a consensus buy.

A third indicator you can use when deciding to sell: traders whose very focus is to bet against stocks they think are going to fall in price. This group is known as short sellers, who sell borrowed shares in hopes of repaying with cheaper shares later.

Adam Reed, a finance professor at the University of North Carolina at Chapel Hill, says that stocks tend to significantly trail the market if they have a high degree of short interest, which is calculated by dividing the number of a company’s shares that currently are sold short by the total number of shares outstanding. In fact, he says, “short interest is one of the strongest return predictive signals in the academic literature.”

You don’t have to actually sell a stock short to follow short sellers’ lead, Mr. Frazzini adds. You can instead use the short-interest data to determine which of the stocks you currently own that you might want to sell first.

The following list is drawn from stocks in the S&P 1500 broad-market index that have declined at least 5% over the past year, according to FactSet. (The index itself has gained 20% over that period.) Each also has a below-average consensus rating from Wall Street analysts, and the number of shares currently sold short amounts to at least 10% of shares outstanding.

The stocks are C.H. Robinson Worldwide, CHRW +1.13% a freight-transportation company; chip maker Cirrus Logic CRUS -0.82% ; independent oil company Forest OilFST +0.98% ; investment bank Greenhill & Co. GHL -2.17% ; Intrepid Potash, IPI +3.30%a fertilizer company; retailer J.C. Penney JCP +2.50% ; Quest Diagnostics, DGX +0.77%a medical diagnostic company; Strayer Education, STRA -4.28% a for-profit college;Tower Group International, TWGP -0.72% an insurance company; and Windstream Holdings, WIN +0.13% a rural telecommunications firm.

Even if you get smarter at selling, though, you can’t overcome a bad buying decision. As Mr. Odean points out, there is no evidence the average individual can pick stocks that outperform the market. That is why he recommends investing in a broad-based index fund. One of the very cheapest and most diversified is the Vanguard Total Stock MarketVTI +0.48% ETF, with an expense ratio of 0.05%, or $5 per $10,000 invested.