Opportunities Lurk in Emerging Markets; Investors Need to Do Their Homework to Find the Right Companies Rather Than Make Broad Developing-Country Bets

February 25, 2014 Leave a comment

Opportunities Lurk in Emerging Markets

Investors Need to Do Their Homework to Find the Right Companies Rather Than Make Broad Developing-Country Bets

JENNY GROSS

Feb. 18, 2014 7:25 p.m. ET

Until recently, it seemed the only way to seek refuge from the havoc in emerging markets was to avoid them completely.

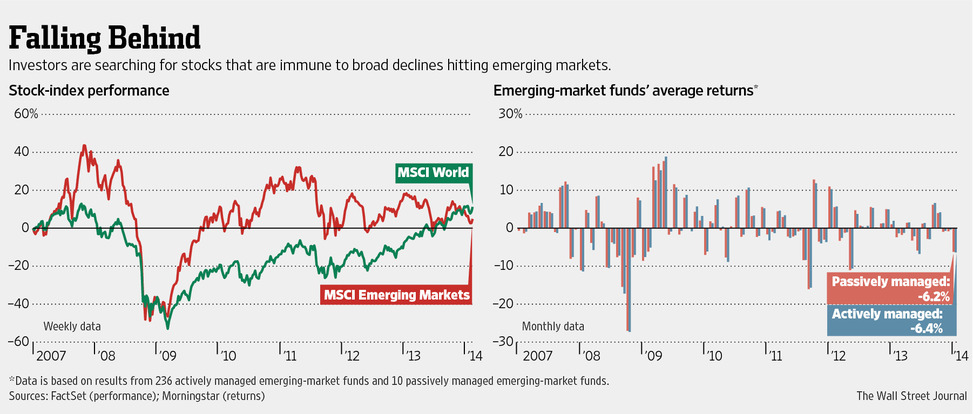

Tidal shifts in U.S. Federal Reserve policy and worries about Chinese economic growth battered emerging-market stocks and bonds nearly across the board last month. The MSCI Emerging Markets Index, priced in dollars, is down 3.8% since the start of the year, and spooked investors have withdrawn billions of dollars from emerging-market funds.

Shares in emerging markets have regained some ground in the past two weeks. But the recent volatility is forcing investors to do their homework to find the right companies rather than just put their money on a broad emerging-market bet, says Richard Titherington, chief investment officer of emerging-market equities for J.P. Morgan Asset Management.

“We think emerging-market equities are relatively cheap,” Mr. Titherington said. “But could they get cheaper? Yes. Therefore, you want to buy companies with strong balance sheets and orient yourself toward companies and sectors that would benefit from currency weakness.”

Last quarter, Mr. Titherington, who oversees $50 billion in assets, shifted about 10% of his fund’s exposure to companies that could benefit from weakness in their local currencies. Those include companies that earn dollars, as well as exporters, such as aircraft- and car-manufacturing companies. At the same time, he decreased exposure to domestic-consumption businesses and financials, sectors that are more vulnerable to currency weakness. He said he has found investments he likes in Turkey but declined to name specific companies.

In past years, money managers scrambled to get into emerging markets. Investing in developing countries is riskier than in developed countries’ markets, but they are attractive because of the potential for fast growth and burgeoning consumer spending. But since the Fed in December said it would further trim its stimulus program, which has flooded global markets with cash, investors have fled the sector en masse. At the same time, growing fears about China’s growth, plus improving prospects for developed economies, contributed to the rush to exit from the sector.

The MSCI Emerging Markets Index has recovered from this year’s low in early February. But 80% of fund managers polled by Bank of America BAC -1.38% Merrill Lynch said they consider emerging markets as the biggest risk for financial stability, according to a survey released Tuesday. The survey, which includes the views of 222 fund managers with combined assets of $591 billion, also found the proportion of funds allocated to emerging-market stocks has fallen to a record low since the survey started in April 2001.

Julian Mayo, co-chief investment officer of Charlemagne Capital, which manages $2.7 billion in emerging-market funds, has increased exposure to TAV Havalimanlari Holding,TAVHL.IS 0.00% the company that operates Istanbul’s biggest airport and other airports. A weaker lira has meant more tourists are likely to head to Turkey and, therefore, more are buying items from duty-free shops in the company’s airports, he said.

He also is investing in exporters based in emerging-market countries, including two Turkish companies: car manufacturer Tofas Turk Otomobil Fabrikasi TOASO.IS -1.79%and appliance manufacturer Arcelik, ARCLK.IS -0.41% which sells products such as refrigerators in developed markets. Tofas is up 3.8% and Arcelik is up 8.5% this month. In the same time frame, Turkey’s main share index rose 3.7%. A weaker currency tends to make a country’s goods more competitive in foreign markets and raises the value of overseas earnings when converted back into the local currency.

Ian Rees, head of multiasset research for Premier Asset Management, said he has recently increased his allocation to funds that handpick undervalued companies and industries in emerging markets, such as Charlemagne Capital’s Magna MG.T -0.60%Emerging Markets Dividend Fund and Lazard’s Developing Markets Fund. He has also diversified his holdings by investing in BlackRock BLK +0.97% Eurasian Frontiers Fund, run by portfolio manager Sam Vecht. Frontier markets tend to be smaller and riskier than emerging markets.

“There has been a lot of indiscriminate selling of late from emerging-market investors,” said Mr. Rees, whose company has $2.5 billion in assets under management. “The liquidity withdrawal creates a really good investment opportunity for active managers.”

Still, the strategy has its risks. For one thing, emerging markets have performed anemically over the past three years. The MSCI Emerging Markets Index, a gauge of stocks in 21 developing markets, fell 5% in 2013, compared with double-digit-percentage rallies in stock markets in the U.S., Japan and Europe. Most managers say it isn’t yet clear that the waves of emerging-market selling earlier this year are finished.

According to figures from Chicago-based research firm Morningstar Inc., MORN +0.57%returns from active and passive funds have been roughly similar. In January, actively managed funds were down 6.4%, while passively managed ones dropped 6.2%.

Patrick Connolly, a certified financial planner for Chase de Vere, independent financial advisers, said the company uses actively managed funds in emerging markets and passively managed ones for large-capitalization U.K. and U.S. companies. He said clients have asked to increase allocations to emerging markets in the past few weeks because they believe the selloff has opened opportunities there.

“Fund managers are looking to see where there are opportunities in this, and the currencies weakening in many countries can create opportunities for those who are exporting overseas to developed markets,” Mr. Connolly said.

He said he recommends J.P. Morgan’s Emerging Markets Equity Fund as well as the Schroder Global Emerging Markets Fund—both of which have people on the ground in countries where they are investing.

Mr. Titherington, the J.P. Morgan investment officer, said investing in developing economies is high-risk, and periods of heightened uncertainty tend to paralyze investors.

“The difficulty you face in emerging markets is the timing,” he said. “When is the bottom?”