Global banking: Inglorious isolation; To avoid another crisis, the Fed further fragments global finance

February 26, 2014 Leave a comment

Global banking: Inglorious isolation; To avoid another crisis, the Fed further fragments global finance

Feb 22nd 2014 | Washington, DC | From the print edition

THE economics of international banking are straightforward enough: raise funds in countries where they are cheap, lend where they are dear. Done right, this is both lucrative for bankers and good for the world, by channelling savings to their most productive use.

Those economics have begun to come apart over the past five years, battered first by the excesses of profit-seeking bankers and now by regulators. On February 18th the Federal Reserve Board voted to “ring-fence” foreign banks’ American operations, forcing them to meet the same standards for capital and liquidity as American banks, rather than allowing them to rely on their parents’ buffers.

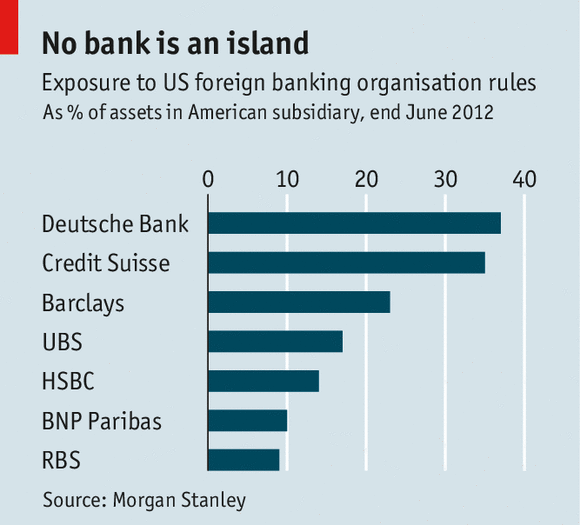

The Fed considers the step essential to insulate America from the cross-border financial contagion that has regularly erupted since 2008. Previously it allowed foreign-owned banks to lean on their parents for support, provided the parents were properly overseen by their own regulators. But over the past 20 years, foreign banks in America have become “more concentrated, more interconnected, and increasingly reliant” on footloose wholesale funding, and now rank among America’s largest securities dealers, notes Dan Tarullo, the Fed governor who oversaw the drafting of the new rules (see chart).

The financial crisis exposed the failings of that set-up. When funding markets froze, foreign-owned banks were among the hardest hit: they accounted for more than half of the emergency loans the Fed made from its discount window in late 2008. Meanwhile, the chaotic consequences of a cross-border failure became all too apparent. When a bank in Iceland failed, the government protected only local depositors; British and Dutch customers had to be bailed out by their governments.

America’s Dodd-Frank Act, passed in 2010, required foreign-owned bank holding companies to meet the same capital standards as their American-owned peers. Barclays and Deutsche Bank responded by moving big American operations out of their holding companies and into more lightly regulated structures.

The Fed’s new rule puts an end to such ruses. Large foreign-owned banks will have to group all American subsidiaries under an intermediate holding company which must then meet the same capital, liquidity and leverage standards as similarly sized American banks. Like American banks, they will have to submit annual capital plans to the Fed demonstrating their ability to meet minimum capital standards even during times of upheaval. In a concession, the rule covers only banks with more than $50 billion in American assets, up from $10 billion in the original proposal. Banks will have until July 2016, instead of July 2015, to comply.

The Fed’s actions will further balkanise global finance. Cross-border lending has plummeted from $5.8 trillion in 2007 to just $323 billion in the first half of 2013, according to McKinsey, a consultant. Most of this reflects economic and business forces, but regulatory actions also play a part. European regulators, for example, have pressed foreign banks to convert branches to separately capitalised subsidiaries and prohibited banks’ local units from repatriating capital to their parents.

By trapping capital and liquidity at the local level, America’s new rule hampers a global bank from deploying money to its most productive destination, in effect undermining the benefits of being global. Luigi De Ghenghi, a partner with Davis Polk, a law firm, notes that stress tests will require many of these banks to exceed capital and liquidity minimums, which makes it “more difficult to repatriate any excess capital from US to non-US operations, or even just to upstream dividends to the foreign parent.” The risk, says one banker, is that “you overcapitalise yourself into complete stagnation”.

The Fed reckons 15-20 foreign banks will have to create holding companies under the new rule. Of the biggest, says Huw Van Steenis of Morgan Stanley, the ownership structures of BNP Paribas and HSBC are already largely in compliance, and Credit Suisse’s soon will be. Deutsche Bank, Barclays and Royal Bank of Scotland have the most work to do. Deutsche may shrink its American balance sheet by $100 billion but would still need to retain $1 billion-$2 billion of additional capital. By shrinking, the three have already each lost a percentage point of market share in bond-trading to their American rivals.

The Fed admits it has thrown sand in the gears of global finance, but argues that the trade-off is worth it. Far worse, says Mr Tarullo, would be another crisis that would cause global capital flows to collapse, leading to “ad-hoc ring-fencing”.

For their part, foreign regulators worry about damage not just to capital markets but to regulatory co-operation. When a draft of the rule was published, Germany condemned the Fed’s “go-it alone” approach, France registered “serious discomfort” and Switzerland bemoaned the “lack of confidence” America had in its peers. Michel Barnier, a European Commissioner, darkly warned of retaliation and said this week: “We will not be able to accept discriminatory measures.”

The Fed has been working with its counterparts on a common approach to restructuring a troubled global bank, something which could have made ring-fencing unnecessary. By blazing its own path before that work was complete, the Fed may encourage others to do the same.