China’s State-Owned Sector Gets a New Boost

February 27, 2014 Leave a comment

China’s State-Owned Sector Gets a New Boost

BOB DAVIS

Updated Feb. 23, 2014 6:20 p.m. ET

When China’s leaders wanted to give a boost to the domestic semiconductor industry last year, a big state-owned electronics company scooped up smaller privately owned chip-design and chip-making firms.

Beijing followed the same script to get control of the sprawling, polluting rare-earths industry: A big state-owned company purchased nine firms in December that mine the minerals used in such strategic industries as defense and telecommunications.

Expect China’s leaders to insist on a big state role in sectors they deem strategic when the officials lay out their economic plans for the coming year at a session of the country’s largely toothless legislature.

On the one hand, China has pledged to dismantle some state-owned monopolies so they operate by market principles and pay more dividends to fund social spending. But on the other, China specialists say the state may actually end up with more influence over the economy in coming years, at least in areas considered central to China’s core interests.

“Beijing has been unable to control strategic sectors in which locally owned SOEs [state-owned enterprises] or private firms predominate because of local government backing, so Beijing has promoted consolidation campaigns,” where large state-owned firms acquire other companies, says Scott Kennedy, a China expert at Indiana University.

Potent forces push against the breakup of monopolies. China continues to encourage jumbo-size state-owned companies to compete internationally, as it has in the past decade, especially in the oil and mining industries. State-owned firms have become powerful enough politically to resist efforts to close them. The Communist Party also has been looking to tighten—not ease—control over state-owned firms so they carry out its priorities.

In 2009, for instance, when Beijing ordered a surge in lending to combat the global financial crisis. China’s largest bank, Industrial & Commercial Bank of China Ltd.601398.SH -1.74% , lagged behind its competitors in ramping up lending because it worried about creating bad debt—a problem that now haunts the Chinese financial sector. ICBC’s chairman, Jiang Jianqing, was the only head of the top four state-owned banks to not get a promotion last year, which banking officials say was meant as a signal to put the party’s priorities ahead of profits.

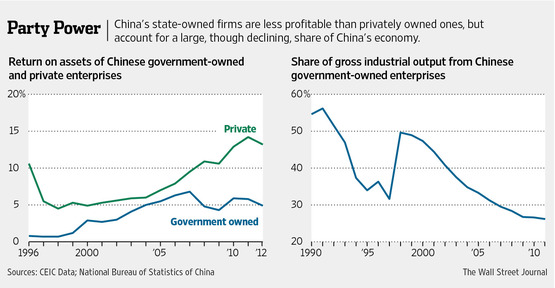

The Peterson Institute for International Economics estimates state-controlled firms account for about 25% of China’s industrial output, though other analysts say state-owned enterprises control an even larger share of the economy. The top 100 or so state-owned firms dominate critical industries, including banking, telecommunications, steel, transportation and electricity. But there are about 100,000 others, owned by provinces and cities, that compete with private companies in a wide range of industries including real estate and hotels.

China’s effort to whittle down the number of SOEs halted during the global financial crisis that began in 2008 and hasn’t resumed, according to a research paper by the Paulson Institute, a China-focused think tank in Chicago. Local governments formed companies to borrow money and build real-estate developments and infrastructure as part of Beijing’s stimulus plan.

“Local governments don’t want to lose the benefits from their control of local SOEs,” said Xuan Xiaowei, an SOE specialist at the Development Research Center, a prominent Chinese think tank. “The control gives them power [and] local income.”

But competitors inside and outside of China complain that state firms have special advantages, including subsidies and easy access to bank loans. One of China’s largest,China Nonferrous Mining

Corp. 1258.HK -0.48% , acknowledged as much in its 2012 prospectus, noting “we enjoy governmental support and preferential treatment in credit borrowing from [Chinese] banks and [in] tax payment.”

The U.S. has been using annual economic negotiations with China to try to persuade Beijing to reduce the SOEs’ advantages. There have been some signs of movement in that direction.

Last week, two big state-owned firms agreed to sell minority stakes in areas traditionally off-limits to private investment, including domestic oil-refining marketing and distribution. Chinese banking regulators also have begun to approve small privately owned banks.

But China’s view of what constitutes commercial operations may be different from what international competitors are seeking. Chinese officials point to Singapore’s big sovereign-wealth fund, Temasek Holdings Pte. Ltd., as a model. Temasek buys stakes in companies, including controlling interests, and its fund managers look to improve corporate profitability and efficiency.

China’s Communist Party plays a far more intimate role in state-owned firms. The party puts in place the top managers at the biggest firms and installs a party secretary, whose job is to make sure party directives are followed. Companies hold “study sessions” to figure out how to carry out party priorities. The heads of local SOEs are often appointed by local party officials.

Having party-appointed Temasek-style asset managers closely oversee the companies, rather than Beijing regulators who sometimes see themselves as company allies, could give the state a stronger hand in corporate affairs.