Frontier market havens come under threat as frailties appear

February 28, 2014 Leave a comment

February 24, 2014 3:46 pm

Frontier market havens come under threat as frailties appear

By James Kynge

Frontier markets are poised at the extremities of market capitalism, a position that often equates to life on the edge for investors. But this year, this exotic asset class of outliers has performed more like a haven from the turmoil of more established emerging markets.

The MSCI Frontier Markets stock index has risen by 3 per cent this year, reaching a post-2008 high on February 19. In the first six weeks of the year, frontier stock markets absorbed inflows of $407m, while $21bn exited the mainstream emerging markets. Frontier US dollar debt markets have also been relatively robust, with JPMorgan’s NEXGEM Index up 4 per cent on the year.

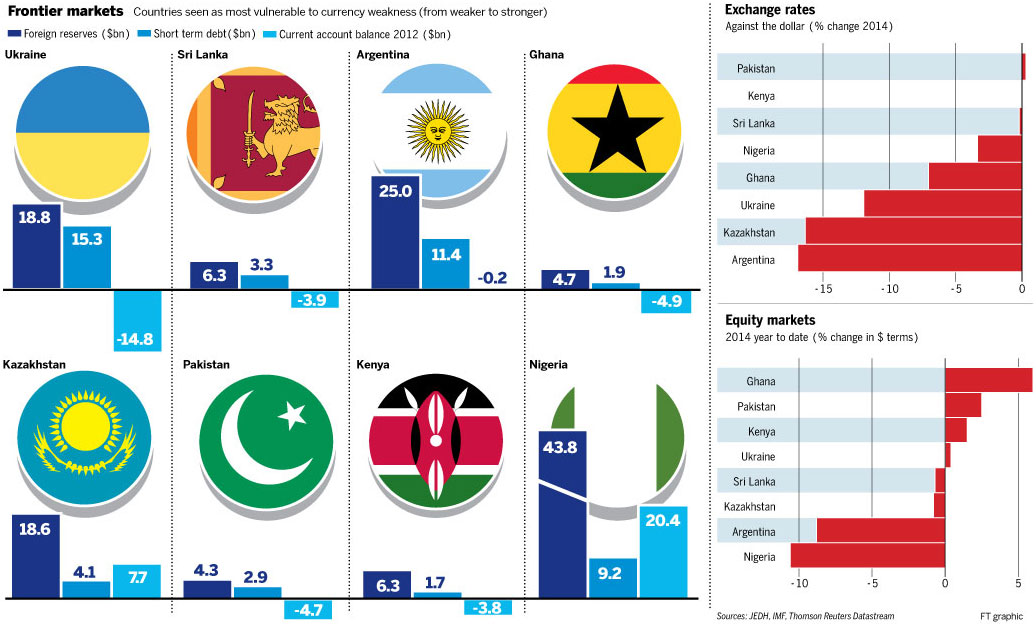

However, the relative calm of the frontier asset class is coming under threat from convulsions among member countries, particularly Nigeria and Ukraine. Economists are identifying frailties that are common to several frontier economies to suggest potential turbulence ahead.

“Until recently, frontier market currencies had come through the numerous bouts of emerging market turmoil over the past year relatively unscathed,” says Jason Tuvey at Capital Economics in London. But, he adds, frontier economy central banks have in recent weeks eased their grip, resulting in slumps for the Argentine peso, Kazakhstan tenge, Ukrainian hryvnia and the Ghanaian cedi.

“Looking ahead, we think further exchange rate weakness is likely to be concentrated in those countries that have already seen the steepest falls: Argentina, Ukraine and Ghana,” Mr Tuvey says. “But a weakening of oil prices and falling foreign exchange reserves could force the Nigerian authorities to devalue the naira.”

According to Mr Tuvey’s analysis, countries particularly at risk of currency contagion are those that have meagre foreign exchange reserves relative to the sum of their current account deficits and short term debts. These include Ukraine, Sri Lanka, Argentina, Kazakhstan, Ghana, Lithuania, Pakistan and Jamaica.

Such a frailty sets up a potential scenario – already evident in Ukraine and Argentina as well as in Venezuela and some other mainstream emerging markets – in which ebbing public confidence in the central bank’s ability to defend the national currency leads to capital flight. This, in turn, brings about the very depreciation that people feared.

Nigeria, which suffered a sharp decline in the naira’s value against the dollar last week, is a somewhat different case. It has a current account surplus that is larger than a year’s worth of maturing external debt, giving it plenty of ballast to avoid potential debt defaults.

The problem for Nigeria, which last week suspended Lamido Sanusi, its internationally respected central bank governor, has been a huge and persistent capital flight linked to what Mr Sanusi alleged was multibillion-dollar oil fraud. Defending the naira against this flight has sapped the central bank’s reserves, weakening the outlook for the currency.

“The market is without a doubt seeing the increased likelihood of a devaluation in the naira,” says Kevin Daly, portfolio manager at Aberdeen Asset Management in London. Mr Daly also sees a possibility that foreign investors will start to sell off positions in Nigerian bonds, pushing yields out by several percentage points.

Another African nation experiencing increased turbulence is Ghana, where rampant inflation coupled with meagre foreign exchange coverage for external liabilities is undermining confidence in the cedi and pushing bond yields higher. Mr Daly thinks the yield on Ghanaian sovereign US dollar bonds could soar from current levels.

However, such volatility always presents opportunities for investors. Ukrainian bonds rallied on Monday as the country’s new leadership issued an arrest warrant for toppled president Viktor Yanukovich, who has not been seen since Friday evening. The announcement came as Yuriy Kolobov, finance minister, said the country would need about $35bn of foreign assistance for 2014-15 and called for donors.

Mr Daly says the turbulence in frontier markets is unlikely to disrupt an estimated issuance of $13bn in frontier market gross debt this year, from $10.7bn last year. However, the turbulence may mean that countries such as Ghana, Zambia and Pakistan will have to pay above the current spreads to lure sufficient buyers.

For Malek Bou Diab of Bellevue Asset Management, which invests in frontier market equities, the current environment throws up a multitude of opportunities. “Even if in the short term you may face a crisis, in the longer term the impetus for reform is there in some countries,” he says. “Nigeria falls into that category.”

Mr Bou Diab says the political opposition in Nigeria had publicised corruption in the government to such an extent that the government would have no option but to clean up its act. Similar opportunities seem likely to flow from governance reforms under way in Kenya, Egypt and Rwanda, he says.